Plasma: The World of On-chain Payments

Bitcoin and USDT dominate crypto, yet both are second-class citizens-BTC fragmented across wrappers, USDT competing for general-purpose block space. Plasma rewrites this: stablecoins as native gas, pBTC as unified omnichain Bitcoin, building settlement rails for the assets that actually matter.

This piece was made in collaboration with the Exa Group team.

From “Sound Money” to Stable Money

Definition:

- TARP (Troubled Asset Relief Program) - U.S. program (2008) that bought troubled bank assets to stabilize the financial system.

- Stimulus packages - Government spending or tax measures to boost the economy during downturns.

In September 2008, the world watched a pillar of Wall Street crumble: “Lehman Brothers”, a 158-year-old investment bank, filed for bankruptcy after no buyer could be found.

Overnight, credit markets froze and trillions of dollars in complex mortgage-backed securities became worthless in spite of what ratings suggested. Governments scrambled: the U.S. launched TARP, central banks injected emergency liquidity, and stimulus packages rolled out worldwide.

For millions, the crisis wasn’t just an economic downturn, it was a sign “TradFi” couldn’t be trusted. Banks had taken reckless risks, regulators had looked the other way, and when it all collapsed, taxpayers were left holding the bill.

Three months after, on January 3rd 2009, the first Bitcoin block was mined, embedding a single headline: “Chancellor on brink of second bailout for banks.”

It referred to British Chancellor of the Exchequer, Alistair Darling, preparing yet another massive taxpayer-funded rescue for struggling banks (just months after the first).

The headline was a direct statement toward the very system that had just failed, a reminder, etched into Bitcoin’s first block, of why it existed.

Bitcoin entered the world as a total polar opposite: a fixed supply, no central authority, and a peer-to-peer network immune to bailouts and political manipulation. But, this “sound” money came with a trade-off: $-denominated volatility.

In traditional economics, money serves three functions:

- A medium of exchange,

- A store of value,

- And a unit of account.

Bitcoin excelled at the first two but failed on the third.

As crypto matured, one problem became obvious - people needed a way to hold value on-chain without constantly dealing with price swings.

Business owners wanted to invoice and pay predictably. Traders needed a way to lock in profits without fully cashing out. And everyday users wanted to participate in decentralization without volatility.

The tedious process of: (a) wiring funds to a bank, (b) waiting days for settlement, and (c) paying hefty fees along the way, created a demand for stable on-chain money.

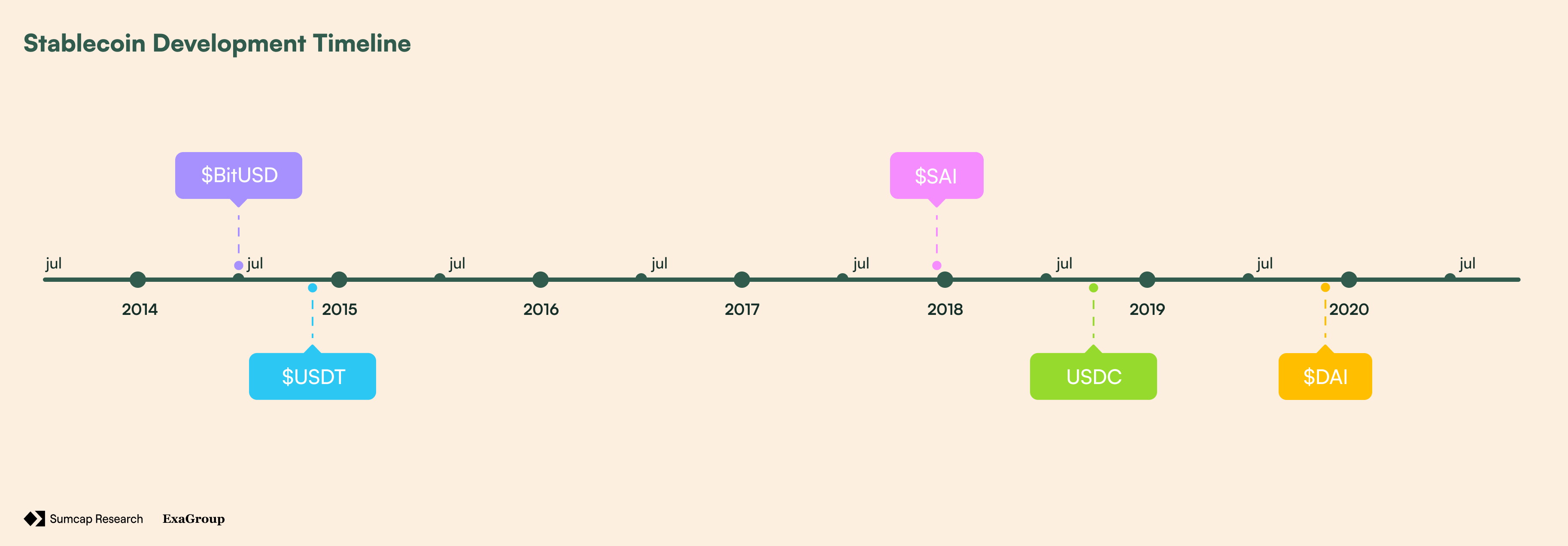

The first to meet this demand was BitShares, with their BitUSD, launched in July 2014. The idea was ahead of its time: users could lock up $BTS (BitShares’ native token) as collateral to create BitUSD, which maintained its peg to the $ through smart contracts and market incentives.

However, the problem was that BitUSD’s peg relied entirely on the value of BTS. When BTS prices fell, collateral ratios could quickly slip below safety levels, triggering mass liquidations.

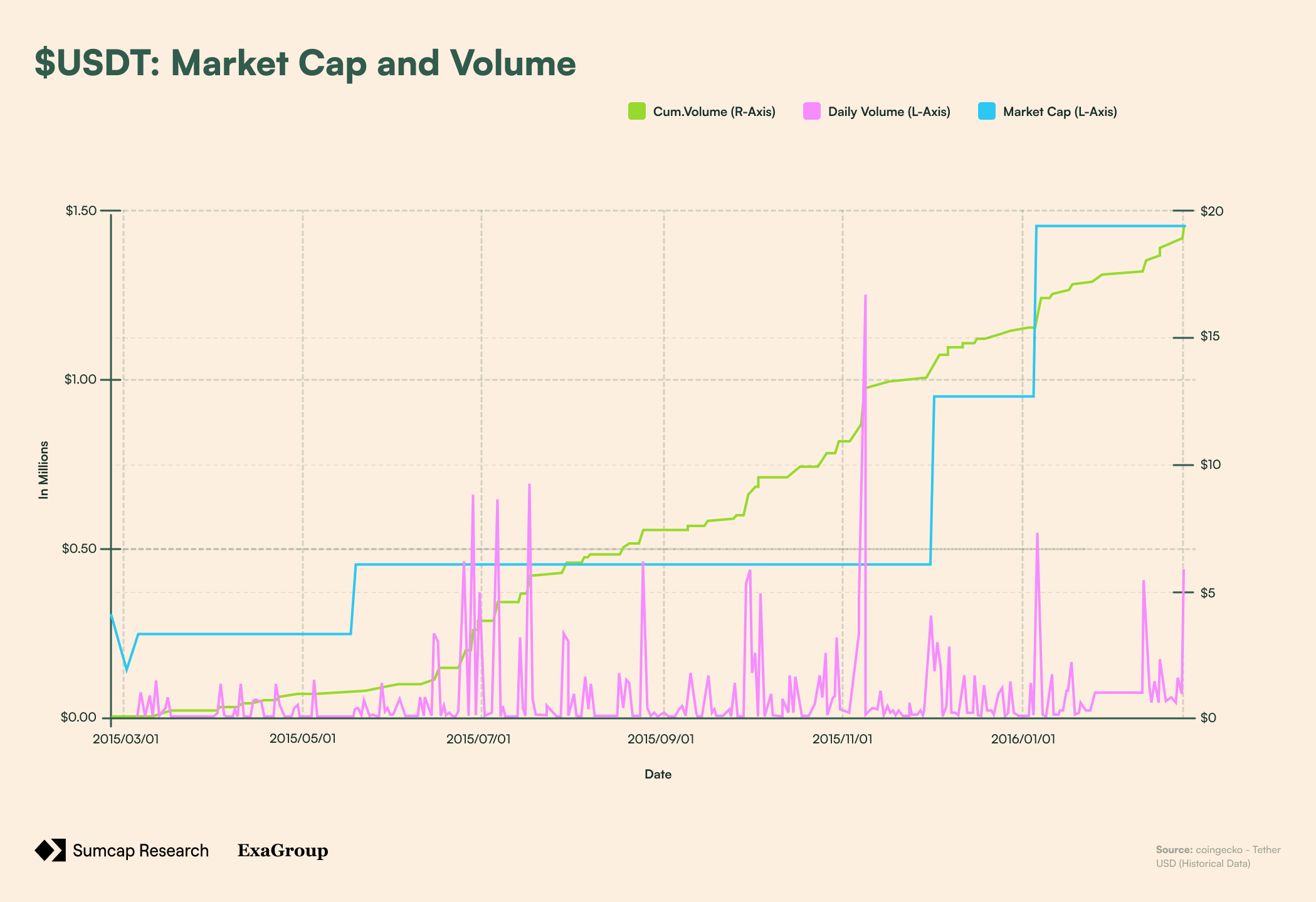

But, just four months later, in November 2014, Tether launched USDT - offering a simpler (fiat-backed) alternative where each token was redeemable 1:1 for U.S. dollars held in custody. USDT didn’t require overcollateralization or complex algorithms, and this simplicity is what allowed it to capture over $19.3M in volume & $1.45M in market cap in just one year.

To put it in perspective, at the time, $ETH was worth only ~$1, while $BTC hovered around $240.

Following USDT’s adoption, teams started searching for new ways to create stability without relying on a centralized issuer. The first major project was SAI (Single-Collateral Dai) by MakerDAO.

Launched on December 18th 2017, MakerDAO’s original system allowed users to lock ETH into Collateralized Debt Positions (CDPs) and mint SAI. While SAI did maintain a soft peg to the U.S. dollar through automated incentives and stability fees, relying only on ETH as collateral left it exposed to violent price swings - much like BitUSD.

To mitigate this risk - after exactly 2 years, on November 18th 2019 - MakerDAO launched Multi-Collateral Dai (DAI). The upgrade expanded the collateral set beyond ETH, improving risk diversification and capital efficiency.

It also introduced a more robust governance model, giving $MKR holders authority over critical parameters such as collateral onboarding, stability fees, and risk controls. With these changes, DAI became the first decentralised stablecoin to achieve broad adoption.

Meanwhile, traditional fiat-backed alternatives continued to grow in parallel. USDC launched on September 26th 2018 and positioned itself as a regulated, fully dollar-backed stablecoin with public attestations of reserves. It found its niche in compliant fintech integrations and became the dominant collateral in DeFi for a while.

Stablecoin Adoption & The Infra Gap

Today, stablecoins are crypto’s most adopted product by both usage and transaction velocity. The scale is difficult to overstate, given that Stablecoin’s Market Cap ($271.657B) is 1.6x bigger than the total DeFi TVL ($166.09B).

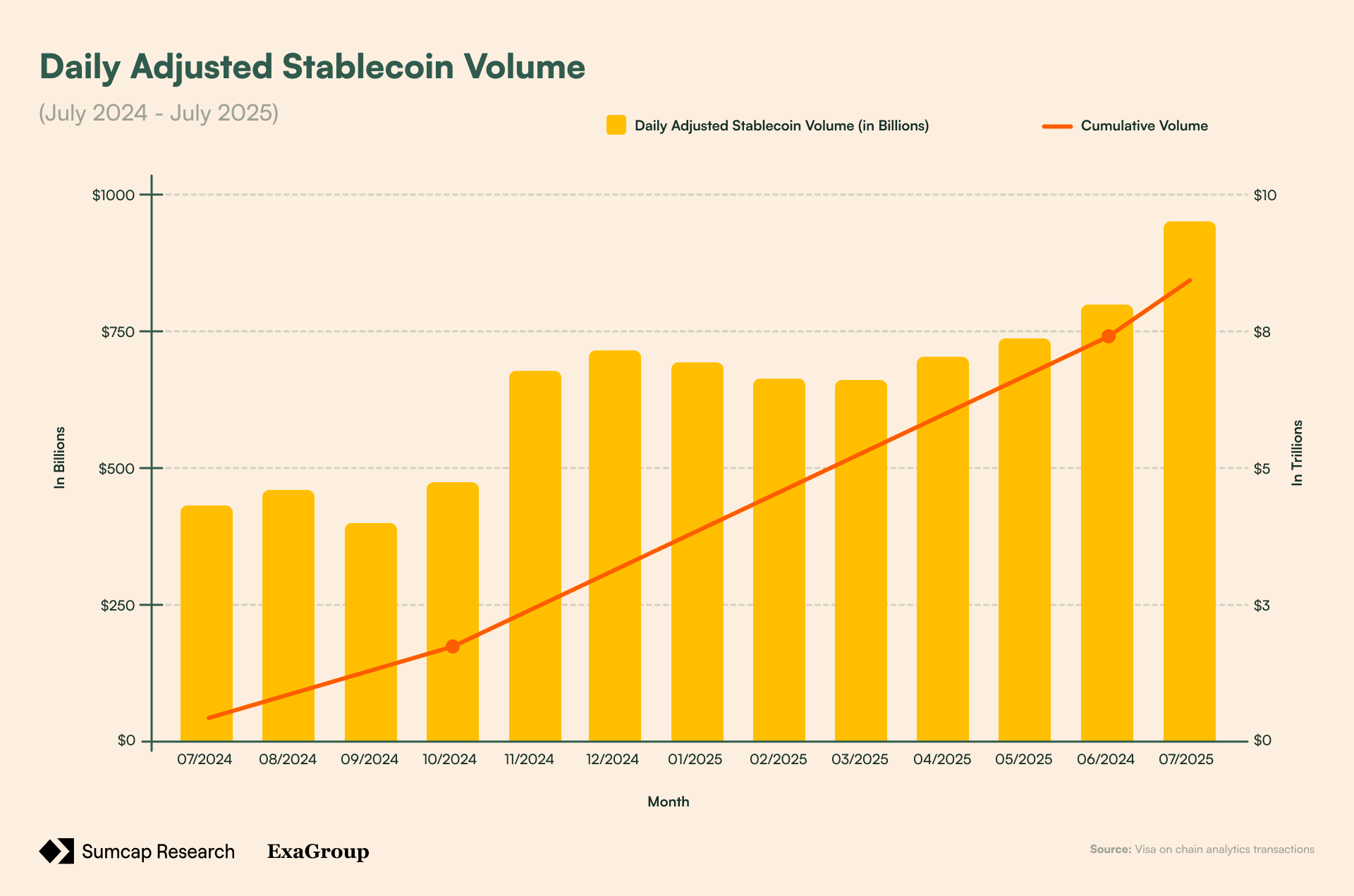

A common comparison used to depict the sheer scale of stablecoin usage is Visa’s Annual Payments Volume (APV). In 2024, Visa processed $13.2T in payments, while stablecoins moved $22T in unadjusted¹ on-chain volume, with an adjusted² figure of $5.67T (which excludes internal exchange transfers and MEV activity).

This adjusted figure has been on a climb for the past 12M, going from $432.3B all the way to $949.07B in daily volume, suggesting an increase in stablecoin demand.

Furthermore, the U.S. Genius Act, signed on July 18th 2025, recognises stables as formal payment instruments, putting them on par with other regulated financial rails like debit card networks, ACH transfers, and wire systems.

Notwithstanding, the core infrastructure for stablecoins hasn’t evolved at the same pace.

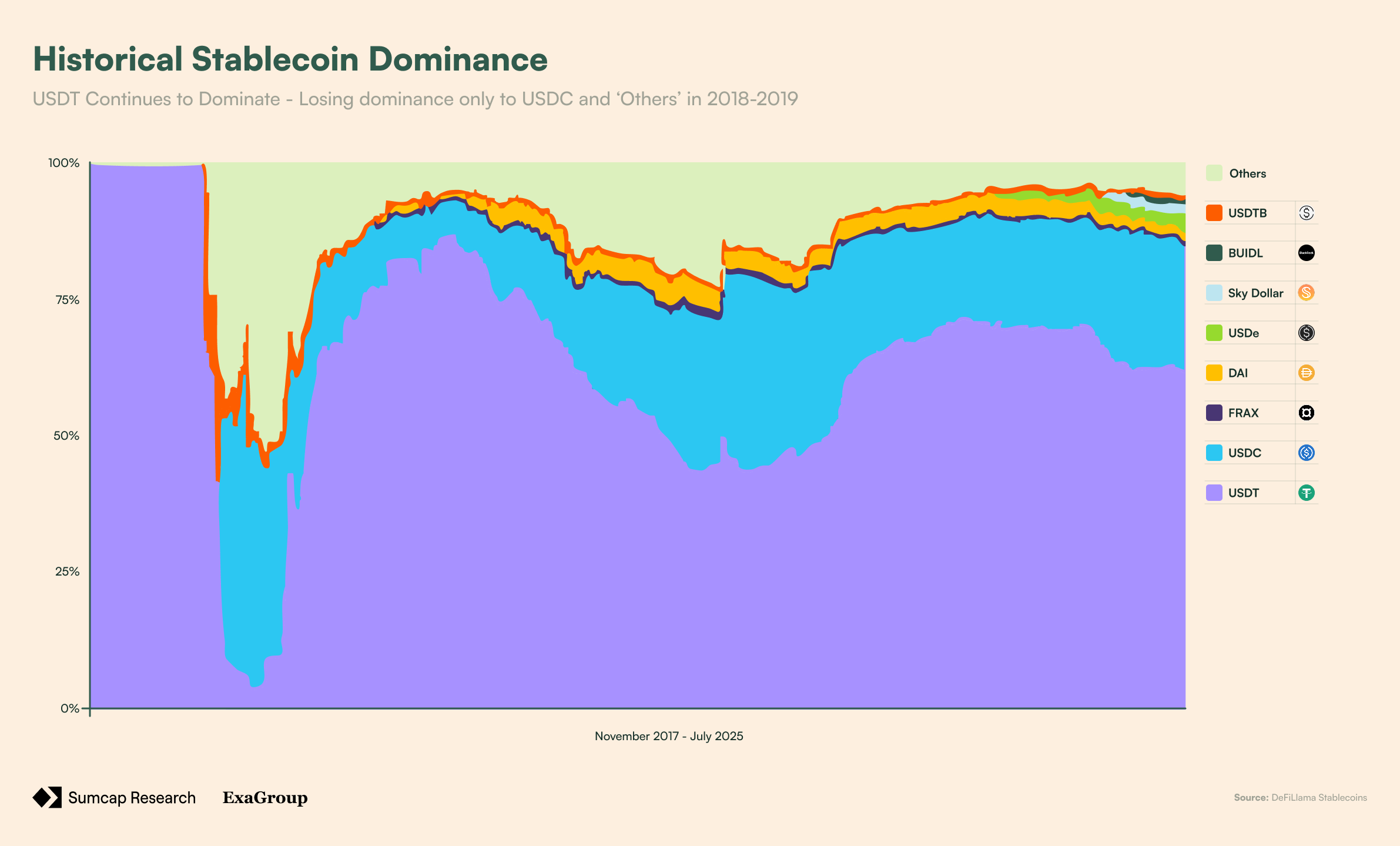

Stablecoins like USDT have become institutionally important, even holding the sector’s dominance with >60%, yet they still live on general-purpose chains that were never designed with them in mind, where:

- Transfers require volatile native gas tokens,

- and none of the underlying infra was purpose-built to meet the scale or compliance expectations of the institutions now entering the space.

This infra gap creates a massive imbalance. Despite moving almost as much annual volume as Visa and being recognized by governments as equal to traditional payment instruments, USDT still operates as a second-class citizen on infra that treats it as just another token.

Ironically, BTC faces a similar paradox. With a market cap larger than silver and a spot as the 7th most valuable asset in the world, BTC should be the most important building block in DeFi. Instead, most of it sits idle.

Existing “wrapped” solutions are little more than glorified custody, and even when BTC does make it into DeFi, it suffers from fragmentation: one wrapped version on Ethereum, another on Polygon, another on Arbitrum, each with its own liquidity pool and friction at every step.

To battle this, Plasma rethinks the foundation itself. Instead of treating stablecoins and Bitcoin as add-ons to a general-purpose chain, it makes them first-class citizens.

In Plasma’s design, stablecoins become the native gas asset, meaning transfers no longer require volatile tokens to move dollars on-chain. For institutions, this eliminates a key barrier to adoption. For users, it creates an experience that finally mirrors the simplicity of existing payment rails.

On the Bitcoin protocol side, Plasma introduces pBTC, secured by a decentralized verifier set rather than a single custodian. Unlike today’s fractured wrapped assets, pBTC is built using LayerZero’s OFT standard, which allows it to exist as one unified token across every connected chain.

By accommodating both stablecoins and Bitcoin at the base layer, Plasma positions itself to become the natural settlement rail for BTC-USDT activity. Together, these two assets represent the most important pillars of crypto - one as its largest store of value, the other as its most widely adopted medium of exchange.

1 - Volume from addresses that are labled as MEV Bots or Intra-Exchange, is considered an interlan transaction, or that have transacted >1k transactions or 10M transfer volume in any 30 day period.

2 - Volume from addresses that are labled as entities related to CEXs, DEXs, or others, or have not transactred >1k transaction or 10M transfer volume in any 30 day period.

The Plasma Stack: A Stablecoin-First and BTC-Native Blockchain

Plasma represents an architectural shift from general-purpose blockchains, positioning itself as infrastructure for Bitcoin and USDT settlement. The network is designed such as it:

- Commits state proofs to Bitcoin for security

- Maintains EVM compatibility through the Reth execution environment.

And to enable gasless USDT transfers at scale, Plasma employs two specialized validator sets:

1. One set is responsible general network security and consensus,

2. The other set processes USDT payments in a high-speed lane optimized for volume and cost efficiency.

PlasmaBFT

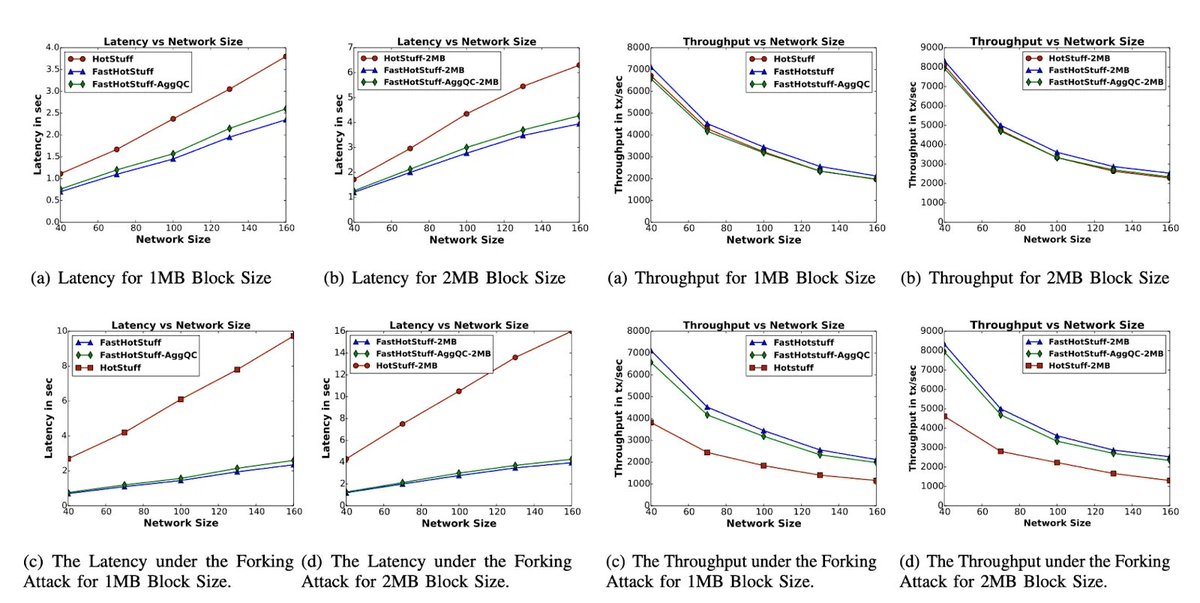

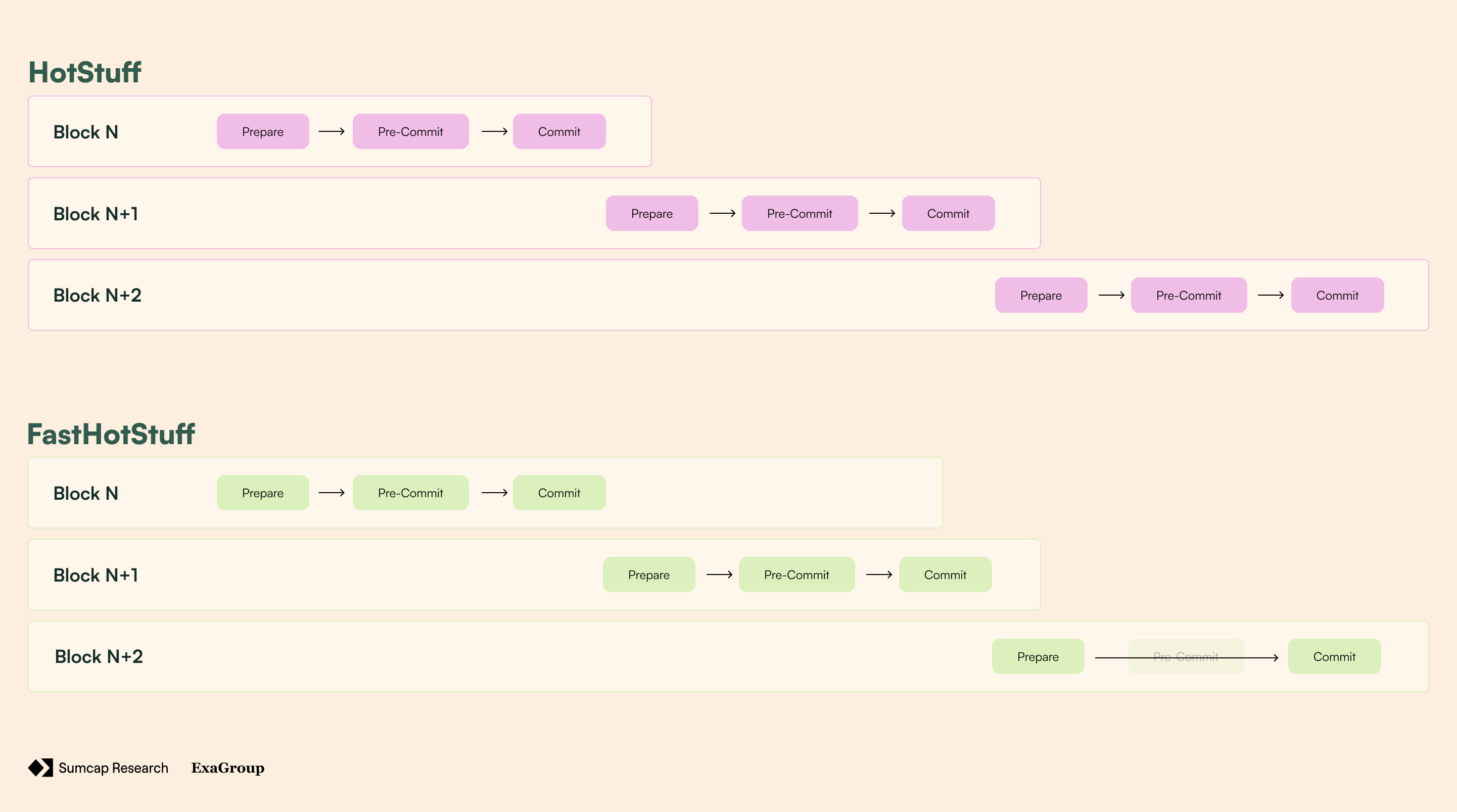

Plasma’s consensus layer, PlasmaBFT, secures the chain through a high-performance implementation of Fast-HotStuff written in Rust.

In traditional BFT protocols (e.g. HotStuff), finalizing a block is done through three phases - each producing a signed proof that a supermajority (more than 23) of validators agreed on that step:

- Prepare - The leader proposes a block, validators check its validity and vote to approve it;

- Pre-commit - Validators confirm that a supermajority approved the prepare phase, then “lock” onto that block to prevent forks;

- Commit - Validators confirm that a supermajority pre-committed, making the block final and irreversible.

Although this three-phase process does guarantee safety, it slows things down as every step requires network communication and coordination.

Fast-HotStuff trims this overhead with what’s called the two-chain commit rule:

If two consecutive blocks (N and N+1) both gather a supermajority, then N can be finalized immediately. This works because reaching a supermajority on block N+1 proves that validators were already locked on N when approving N+1, so the pre-commit phase is not needed.

In practice, the 3 phases collapse into 2:

- Phase 1 (Prepare) - vote on block N

- Phase 2 (Commit) - vote on block N+1, which finalizes block N

However, in edge cases where the network fails to hit the two consecutive supermajorities required for fast finality, PlasmaBFT falls back to the full three-phase commit protocol from classic HotStuff. This ensures that all honest validators securely "lock" onto the same block before finalisation, maintaining safety and liveness.

Once the fallback resolves, PlasmaBFT resumes the fast two-phase path.

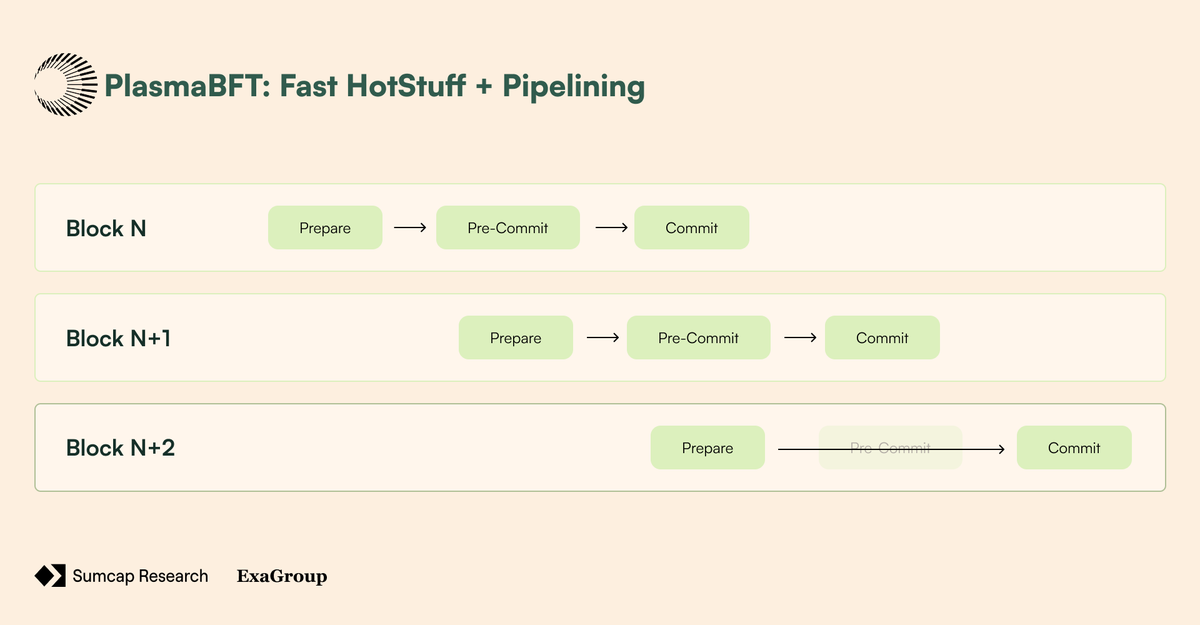

But, it doesn’t stop there. With pipelining, multiple blocks can be worked on at once by overlapping their phases:

While validators are in the commit phase for block N, they can already be in the prepare phase for block N+1. The next block doesn’t have to wait for the previous block to fully finalize before starting its voting process.

It effectively keeps the network busy at all times - maximizing efficiency without sacrifice.

Additionally, by only selecting a subset of validators (committee) via a cryptographically secure, stake-weighted random process for each round, Plasma reduces communication overhead while still applying the same supermajority rules.

Consensus Rollout & Validator Incentives

Plasma uses a Proof of Stake mechanism for validator selection, so validators earn rewards by participating in consensus and signing blocks. But, unlike in normal PoS, misbehavior is handled through reward slashing instead of stake destruction.

This allows Plasma to align with institutional expectations (where unexpected loss of funds is unacceptable), while still incentivizing correct behavior.

Plasma’s consensus will launch in three phases:

- Trusted Validator Launch - A small set of known validators secures the network at mainnet launch for stability;

- Validator Expansion - The validator set grows to test performance and throughput with larger committees;

- Permissionless Participation - Public validator access enables real decentralization while maintaining supermajority safety and PlasmaBFT’s fast-path optimizations.

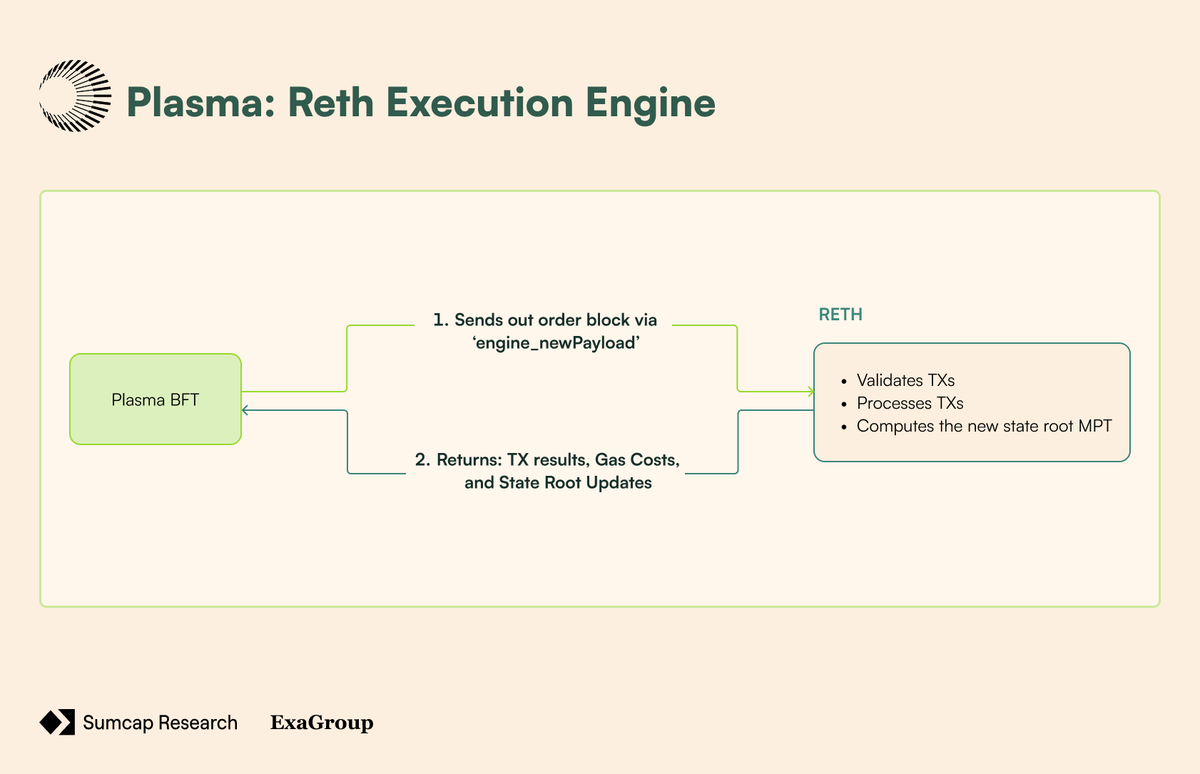

The Reth Execution Engine

Plasma's execution layer is built on Reth, a modern Ethereum client written in Rust that manages: state transitions, transaction processing, and EVM operations with complete EVM compatibility.

Every opcode, precompile, and execution behavior functions identically to Ethereum mainnet, making migration of existing contracts and tools easy.

Reth connects with the consensus layer through the same Engine API Ethereum has used since the Merge.

This separation of tasks allows PlasmaBFT to handle consensus and block ordering, while Reth focuses on transaction execution and state transitions:

- Block Proposal - the CL sends the ordered block (containing TXs) to Reth via the Engine API’s engine_newPayload call

- Transaction Validation - Reth validates each TX’s format, signature, nonce, and gas requirements before execution

- State Execution - Reth processes TXs sequentially

- State Root Calculation - After executing all TXs, Reth computes the new state root and TX receipt root using Merkle Patricia Tries (MPT) - used for storing and verifying data integrity

- Execution Confirmation - Reth returns the execution results, including gas usage, TX receipts, and the updated state root back to PlasmaBFT

- Block Finalization - PlasmaBFT incorporates the execution results into the final block header and completes the consensus process

Native BTC Bridge

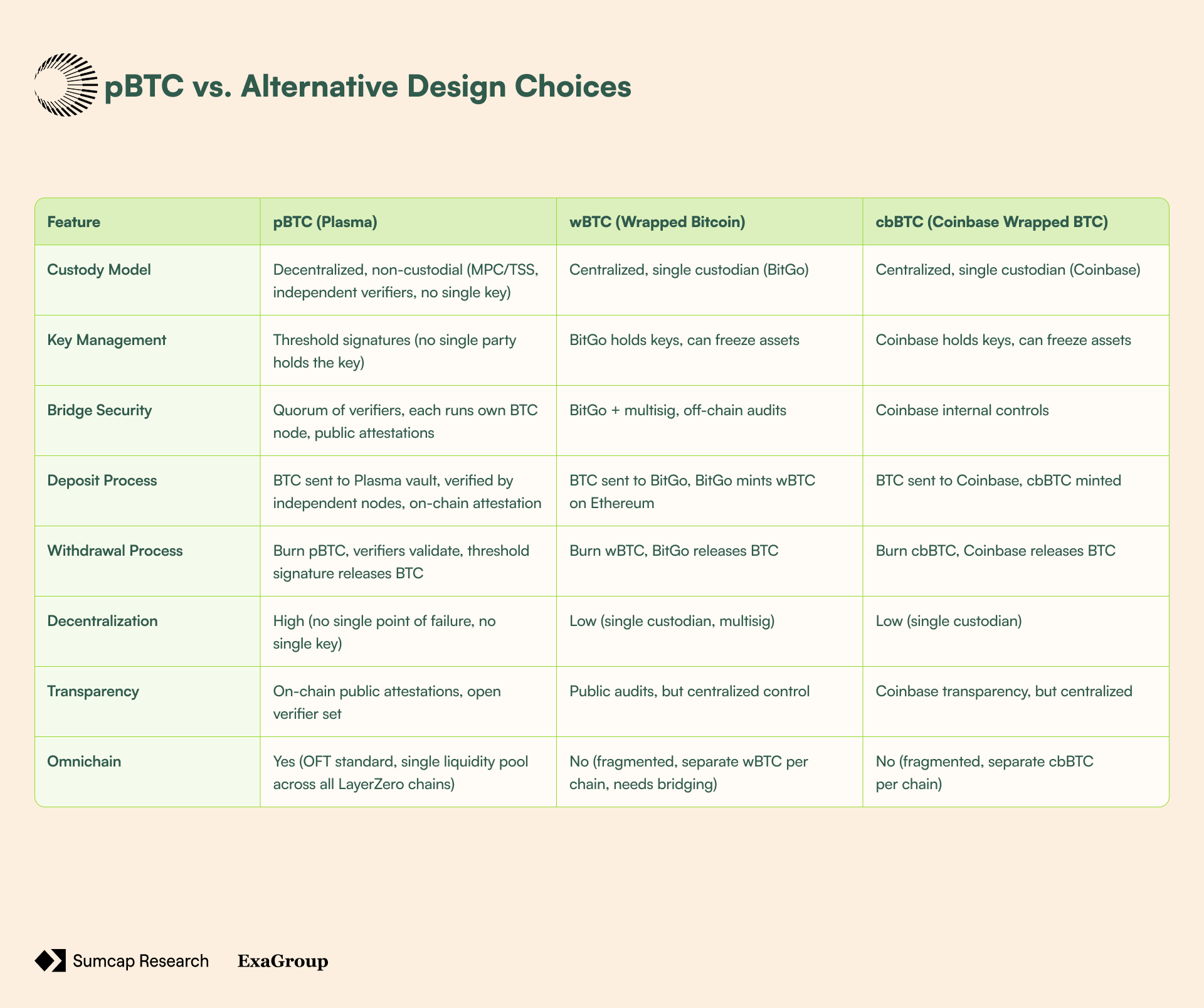

Most BTC bridges today look decentralized on the surface, but peel back the layers and you’ll find either:

- A single custodian (like BitGo the issuer of $wBTC) holding everyone’s coins, or

- A small multisig that can freeze the vault at any time.

That’s the tradeoff users have accepted: if you want BTC in DeFi, you give up Bitcoin’s trust-minimized design.

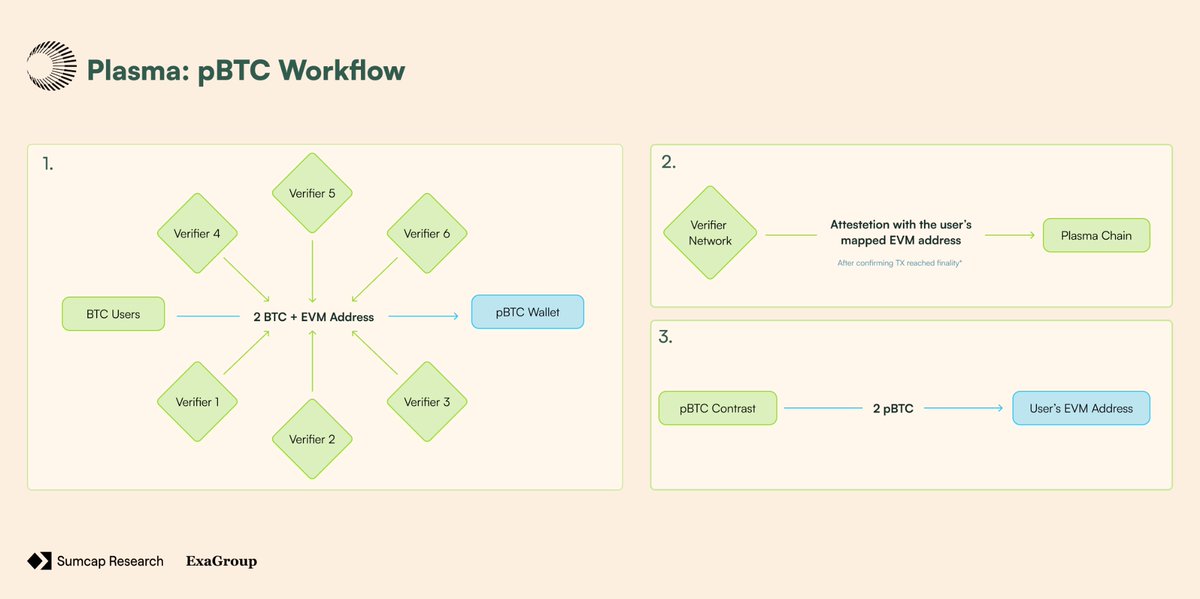

Plasma’s native Bitcoin bridge changes this. Instead of custody, it’s powered by a network of independent verifiers that each run their own Bitcoin node. No single party controls the vault, and for BTC to move in or out, a quorum of verifiers must collectively sign off using threshold signatures (MPC/TSS) - meaning no individual ever holds the keys.

When a user deposits BTC into the Plasma vault on Bitcoin, the process doesn’t rely on a custodian to “promise” the funds are there. Instead, every verifier:

- Independently “sees” the deposit through their own Bitcoin node,

- Confirms it reached finality,

- And then broadcasts an attestation on-chain.

Those public attestations prove that BTC was received and carry the user’s mapped EVM address, which the depositor specified in the transaction metadata. Once a supermajority of verifiers agree, pBTC is minted directly to that address on Plasma, and the attestations sent on-chain.

Withdrawals work the same way:

Burning pBTC signals to the verifier network that BTC should be released back on Bitcoin. A quorum of verifiers validates the burn on Plasma, then collectively produces a threshold signature to unlock the Bitcoin.

The key is never concentrated anywhere, so no single verifier can move coins alone, because the signature is stitched together from fragments that only exist in aggregate.

But the trust model improvements are just part of the story.

Most BTC bridges today suffer from another critical flaw: liquidity fragmentation. Take wBTC for example - it exists as a separate, incompatible version on every chain. wBTC on Ethereum can't directly interact with wBTC on Polygon or Arbitrum without additional bridging steps, separate liquidity pools, and more complexity for users and protocols.

Plasma solves this by implementing pBTC using LayerZero's OFT (Omnichain Fungible Token) standard. Instead of creating isolated token instances per chain, pBTC operates as a single token across all LayerZero-connected chains. When you move pBTC from Plasma to Ethereum or any other supported chain, you're not bridging to a wrapped version - you're moving the same native pBTC token.

This creates a single liquidity pool for pBTC that spans the entire omnichain ecosystem.

Bridge Roadmap

Even though the current verifier network already has significant trust minimization compared to custodial alternatives, the bridge architecture is made with expansion in mind.

Plasma is actively tracking developments in Bitcoin's ecosystem that could enable even deeper security guarantees:

- BitVM-style Bitcoin validation via onchain verification circuits

- Zero-knowledge proofs for cross-chain state attestations

- Bitcoin opcode upgrades such as OP_CAT for custom verification logic

Stablecoin-Native Design

Zero-Fee USDT Transfers

Plasma implements contract-level paymasters that sponsor transfer and transferFrom functions through a sophisticated account abstraction (AA) system built on EIP-4337 and EIP-7702 standards.

The paymaster operates as a network-funded account that automatically covers gas fees using XPL token reserves when verified users execute basic USDT payments.

When users initiate transfers, the paymaster performs real-time eligibility verification by checking sender patterns, transaction frequency, and user reputation before automatically covering costs. How?

- By evaluating multiple lightweight verification methods including zkEmail attestations, zkPhone verification, Cloudflare Turnstile, and signature-based allowlists.

- Rolling caps on subsidized transfers (e.g., 5 per 24 hours) enforced through either contract storage or signature-bound counters.

Custom Gas Tokens

The protocol-managed paymaster leverages EIP-4337 standards, calculating gas costs through oracle-derived rates with slippage protection. Unlike third-party paymasters that charge markup fees and depend on external funding, Plasma's approach guarantees consistent, fee-free operation across applications.

Confidential Payments

Plasma’s shielded transactions hide amounts, recipients, and metadata while preserving selective disclosure for compliance. This targets enterprise use cases where operational privacy provides competitive advantages such as payroll distribution and supplier payments.

This technical implementation employs

- Stealth Addresses: One-time addresses that hide recipients. Each payment goes to a unique address only the recipient can access.

- Encrypted Memos: Private notes attached to transactions. Only holders of the decryption key can read the contents.

- Selective Disclosure Proofs: Users control exactly which transaction details to reveal and when. Full privacy by default, with verifiable proof capabilities for compliance or audits.

Competitive Landscape & Opportunity Sizing

Total Addressable Market (TAM)

We’ve all heard of the classic business metaphor:

“Better to be a big fish in a small pond, than a small fish in a big pond.”

Plasma is doing exactly that in the world of on-chain payments and yield market opportunities.

Instead of competing as another general-purpose chain with a technical innovation that doesn’t bring any merit, Plasma is laser focused on becoming the infrastructure for institutional use.

And this focus couldn’t be more timely.

TradFi players are increasingly exploring BTC treasury strategies - with MicroStrategy leading the herd with over 636,500 BTC ($~70b) in custody. Meanwhile, the payments industry is racing to build faster and cheaper rails for cross-border transactions, with stablecoins emerging as the clear winner for international settlement.

“Native BTC”: Tokenisation and Yield Market Opportunities

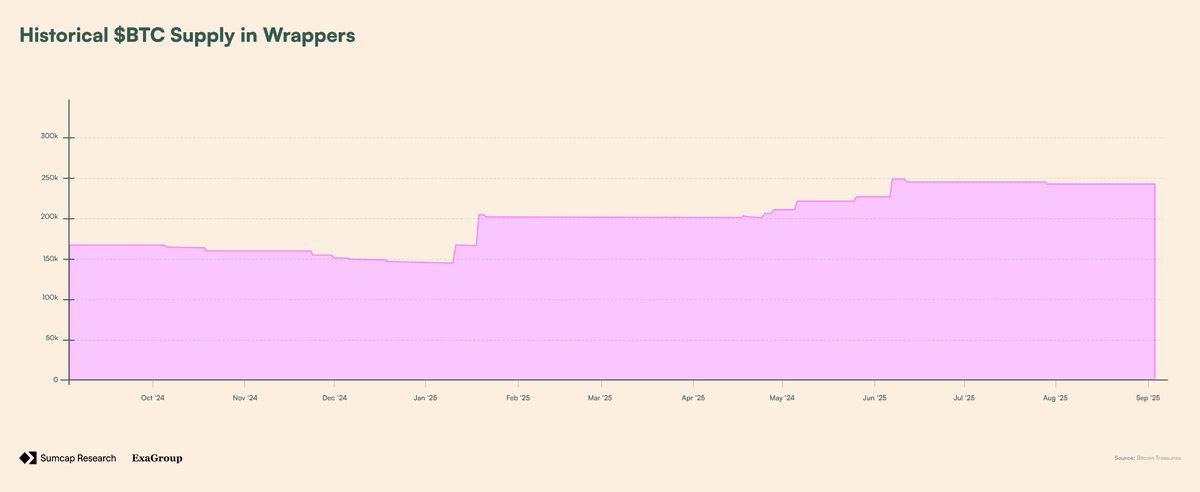

Even though it’s the largest crypto asset, BTC still remains unused across DeFi - with wrapper products removing all of its trust-minimized ideology.

As the most decentralised BTC wrapper solution, pBTC offers “Native BTC” DeFi opportunities that others just can’t mimic.

With over 242.6k BTC in wrapper solutions and 209.8k BTC (~86.5%) actually deployed across protocols & earning yield - pBTC’s base opportunity comes from retail users looking for safer ways:

- To use BTC across DeFi;

- To store BTC on, more accessible, EVM chains.

But, this retail demand is just part of the story.

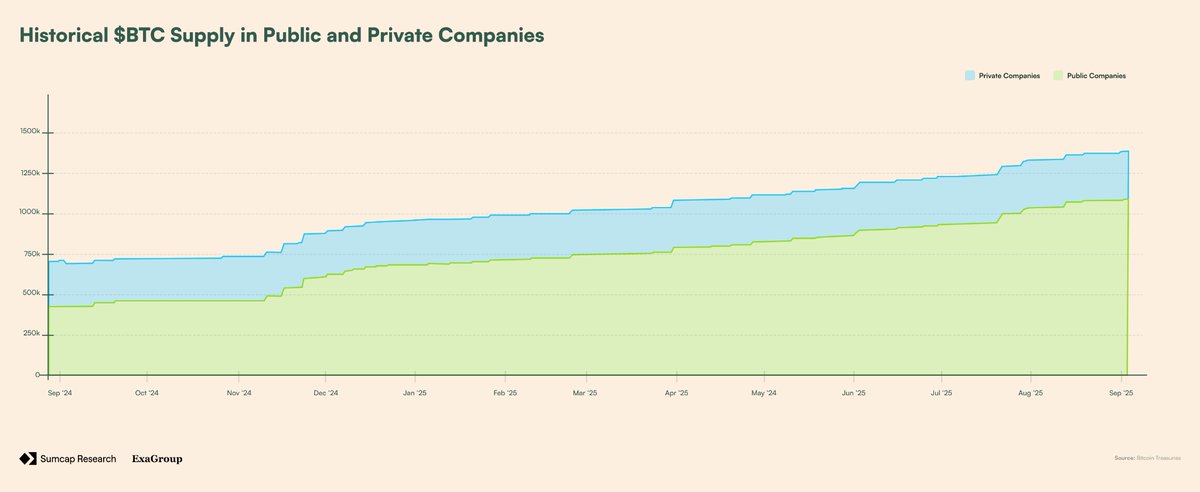

Institutional and corporate adoption is catching on, with public and private companies now holding a combined ~1.38M BTC. That’s a stark difference compared to that start of the year where these same entities held only 547k BTC in custody.

This 833k BTC increase highlights a clear trend in institutional adoption that’s only accelerating. But, here’s the key insight: as more and more institutions get BTC into treasuries, their strategies will evolve from simple holding to active management.

For this, pBTC represents the perfect intermediary - as these players prioritize infrastructural safety over everything else.

On-chain payments: Cross-border payments and Payroll

In 2023, 184M people (2.3% of the world’s population) were reported to live outside of their country of nationality. Usually driven by economic opportunities, these migrant workers often find themselves sending money back to their families and community across borders.

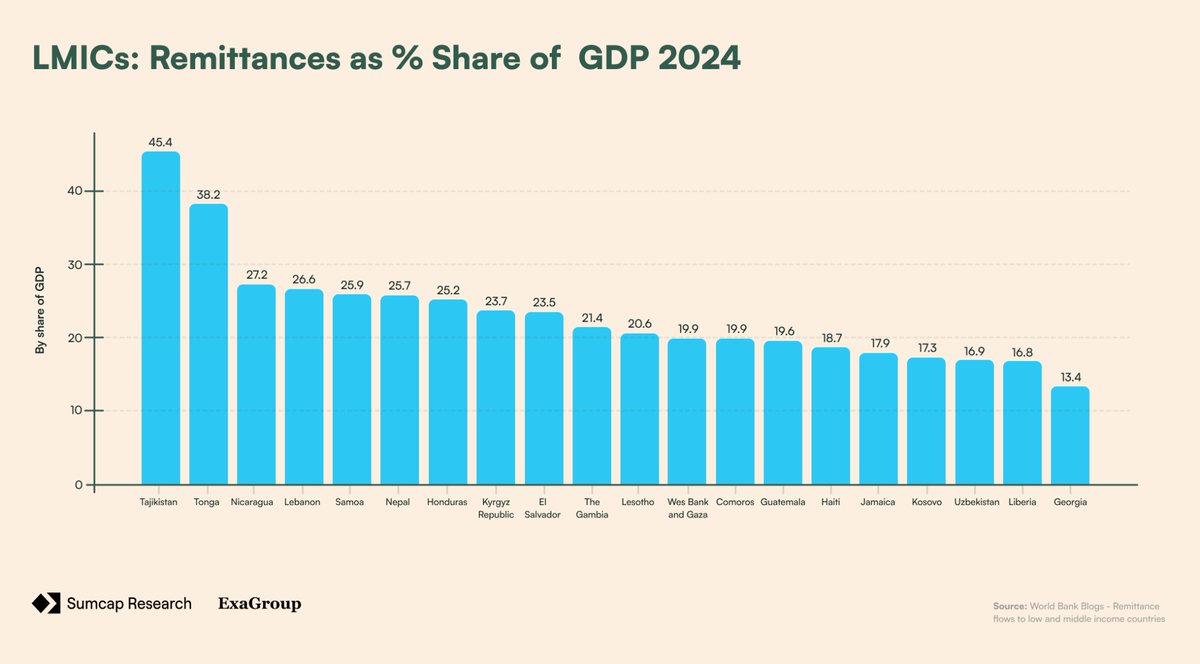

These cross-border payments (or “remittances”) play a crucial role in supporting the economies of low & middle income countries (LMICs) - and, for some of them, even amount to half of their gross domestic product (GDP).

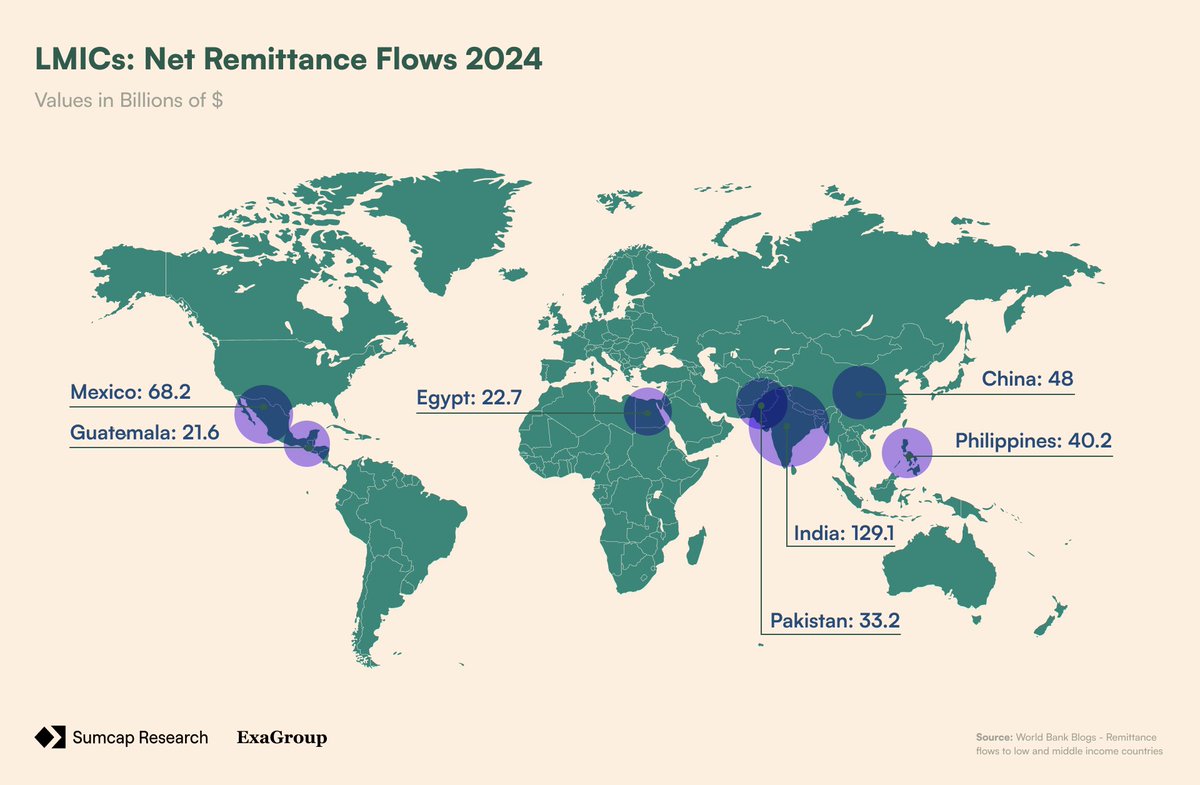

In 2024, remittance flows to LMICs came out to $685B, with the top 5 recipient countries being:

- India - $129B

- Mexico - $68B

- China - $48B

- Philippines - $40B

- Pakistan - $33B

These massive flows represent literal lifelines for millions of families across the world - but, they come with a hidden cost.

Take India for example. In 2023, India received a reported $16B in remittances from the US. At the average $200 transfer cost of 4.16% (Exchange Rate Margin + Fee), India lost $665M of that money to banks/FXs.

That’s $665M that hundreds of thousands or even millions of Indian households never received - and this pattern repeats across every major corridor.

Mexico, receiving roughly >$50B from the US annually, loses over $2.4B to fees at current transfer costs. Meanwhile, Nigeria, which receives $6B in remittance from the US, loses $180M.

The opportunity for Plasma here is clear. With their zero-fee USDT transfers, Plasma could eliminate the billion-dollar extraction that traditional rails impose on vulnerable populations each year.

A migrant worker could finally send the full $200 to their family in Guatemala, and not $187 after fees. Over time, this would amount to thousands of dollars saved per family - money that stays in the communities that need it most.

Remittances, however, represent only a part of Plasma’s reach. When we pair zero-fee USDT transfers with auditable confidentiality, Plasma opens the doors to a totally new market: on-chain payroll.

In 2023, the U.S. alone produced a total of $11.07T in wages and salaries across 134.06M employees.Thats 1.6B (12×134M) bank transfers annually - all of which incur fees to companies.

For simplicity, let’s assume those wages are paid monthly via ACH direct deposits. With flat fees ranging between $0.20-$1.50 per transfer (and a median of $0.85), U.S. companies are spending $1.37B annually just to move money to their employees’ accounts:

134.06M × 12 × $0.85 = $1.37B

Much like with remittances, money that can be better used by the companies sending out the transfers has to be wasted on fees.

With Plasma’s gasless USDT transfers, U.S. emoplyers would save ~$1.4B each year, while confidentiality adds another layer of value for both employers and employees:

- Employers - Salary data hidden from competitors while maintaining full auditablility

- Employees - Reduces fraud/theft targeting and protects from unwanted financial pressure

Sizing The Opportunity

Plasma sits at the intersection of three of the largest financial flows in the world:

- Savings and capital deployment - letting users earn yield on BTC without leaving DeFi.

- Cross-border payments - saving billions in remittance fees for migrant workers and families.

- Payroll - eliminating friction and fees in domestic and international wage payments.

Even modest adoption across each of these segments is enough for a multi-billion-dollar TAM. Sizing these opportunities across adoption possibilities, we get 3 distinct scenarios: Base, Bear, and Bull Case.

📊 Base Case Scenario:

- For pBTC, market capture assumes a 5% retail adoption of existing wrapped BTC users (~12k BTC) simply from seeking safer alternatives, plus a 3% institutional adoption (~41k BTC) as corporations begin exploring DeFi yield on treasury holdings.

Total pBTC capture: ~53k BTC ($5.7B) - For on-chain payments, a 1% remittance adoption ($6.85B) driven by cost savings awareness in key corridors like US-Mexico and US-India is realistic, alongside a 0.01% payroll adoption ($5B) from forward-thinking tech and remote-first companies prioritizing cost reduction and privacy.

Total on-chain payments capture: $11.85B

📉 Bear Case Scenario:

- As users stick with wBTC because of familiarity, it maintains its market monopoly through brand recognition and existing integration resulting in only a 0.5% retail adoption of existing wrapped BTC users (~1.2k BTC). Similarly, a 0.5% institutional adoption (~7k BTC) is limited by regulatory uncertainty and preference for established solutions.

Total pBTC capture: ~8.2k BTC ($890M) - For on-chain payments, remittance adoption is hindered by crypto literacy gaps in target demographics and regulatory barriers, resulting in only a 0.3% ($2.05B) capture, alongside a 0.005% payroll adoption ($2.5B) due to long enterprise sales cycles and strong resistance from traditional payroll providers.

Total on-chain payments capture: $4.55B

📈 Bull Case Scenario:

- For pBTC, market capture assumes 15% retail adoption of existing wrapped BTC users (~36k BTC) as crypto UX improves dramatically and trust-minimized solutions gain recognition, plus 8% institutional adoption (~110k BTC) driven by widespread corporate DeFi strategies and clear regulatory frameworks favoring decentralized solutions.

Total pBTC capture: ~146k BTC ($15.8B) - For on-chain payments, a 5% remittance adoption ($34.25B) as crypto becomes mainstream in emerging markets with government support and infrastructure improvements, alongside 0.05% payroll adoption ($25B) from progressive enterprises embracing crypto-native operations.

Total on-chain payments capture: $59.25B

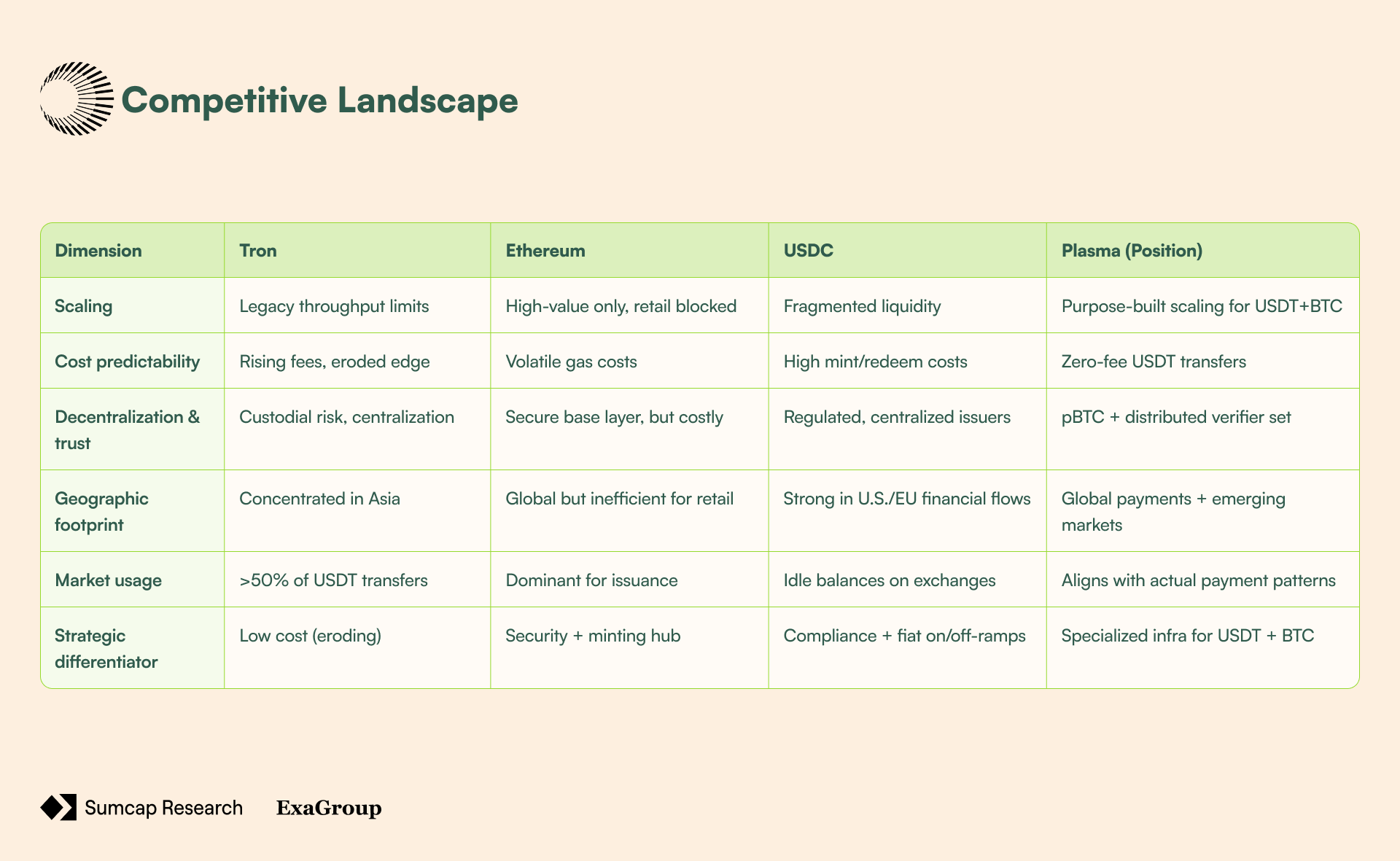

Competitive Landscape

Tron's Structural Constraints and Market Reality

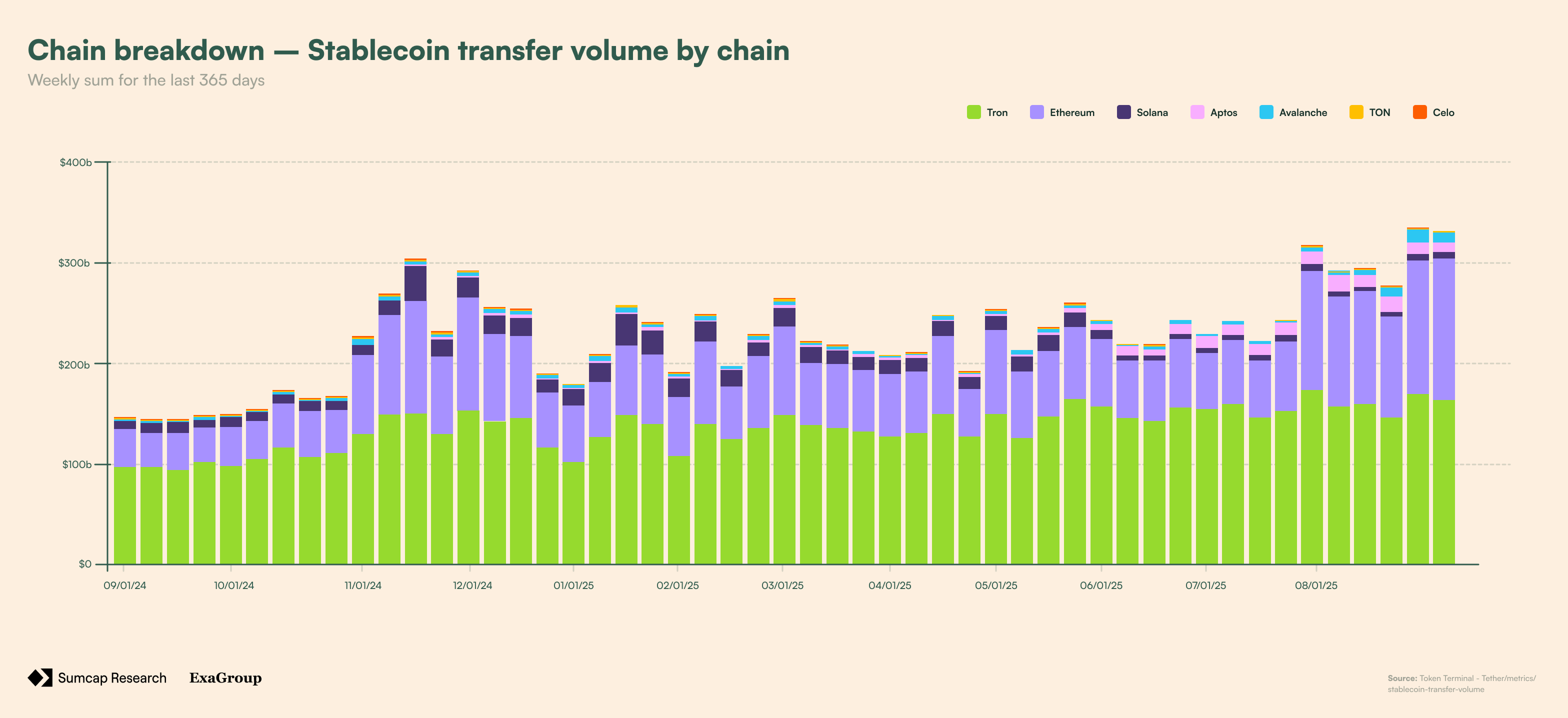

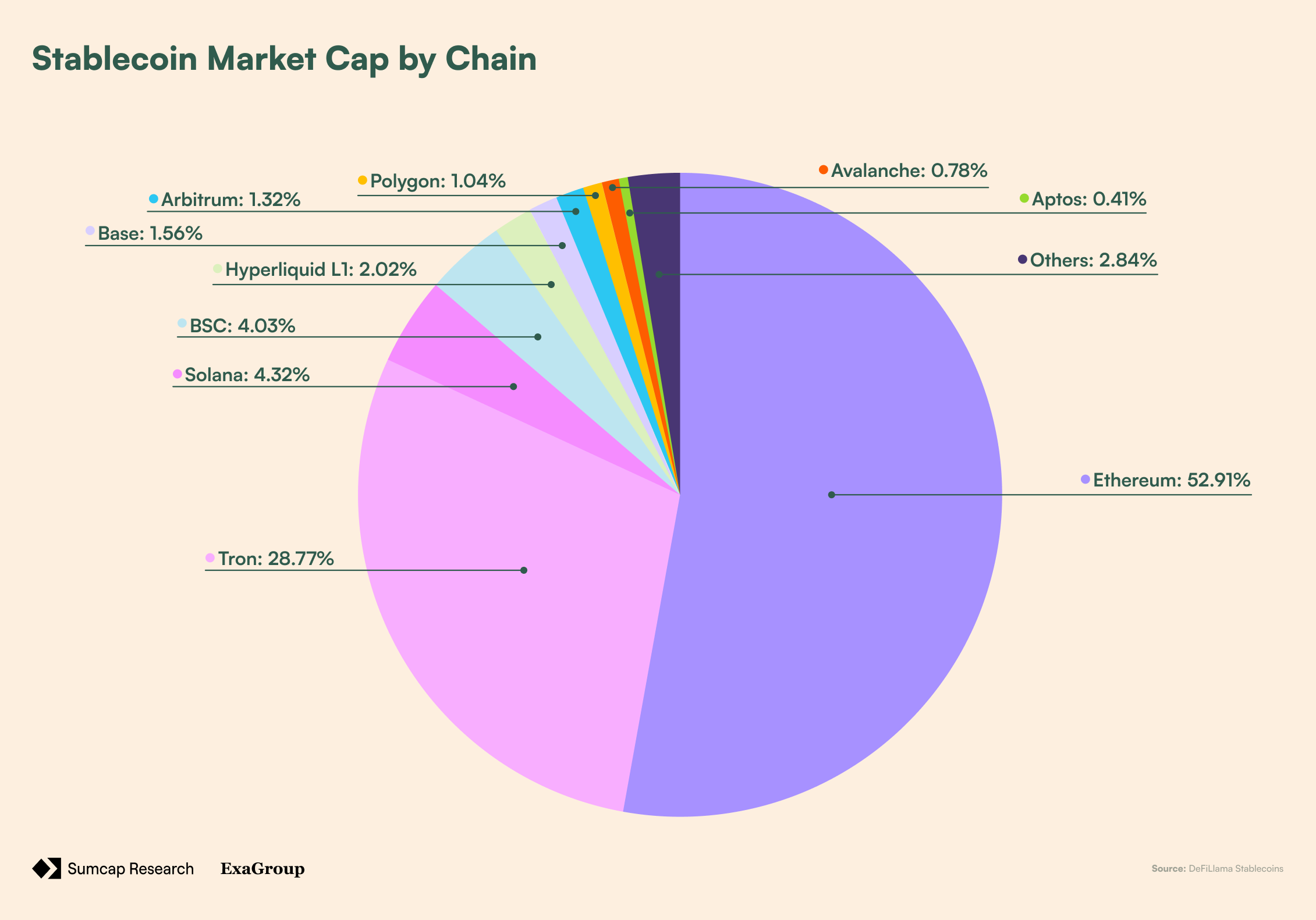

Despite processing the majority of USDT daily transaction volume (50>%), Tron faces fundamental architectural limitations that create opportunities for purpose-built alternatives:

- Lack of modern scaling capabilities and institutional-grade infrastructure features

- Rising stablecoin transfer costs

- Centralization concerns, leading to discomfort with maintaining significant inventory exposure

- Geographic concentration in Eastern markets, add costs without providing strategic benefits

Ethereum’s Payment Flow Limitations

Ethereum remains foundational for stablecoin issuance and large-value transfers where gas costs are negligible, but it is economically unviable for sub-dollar payments. Its general-purpose architecture forces stablecoin flows to compete with other applications for block space, resulting in unpredictable fees and latency that undermine its suitability as a retail payment infrastructure.

Infrastructure Mismatch in Emerging Markets

The limitations of current stablecoin infrastructure are most visible in emerging markets, where USDT demonstrates its strongest adoption patterns across remittances and local commerce. However, Ethereum’s cost structure renders small-value retail transactions economically unfeasible.

Ethereum continues to function effectively as a settlement layer for high-value transfers, but it lacks the characteristics required for day-to-day retail payments. This gap underscores the need for infrastructure purpose-built to support stable, predictable, and scalable consumer transactions.

Plasma directly addresses these constraints through specialized design choices:

- Protocol-managed paymasters remove dependence on volatile gas tokens, ensuring predictable costs in USDT.

- Dedicated validator sets optimize for USDT throughput without competing against general-purpose block space.

Together, these features align infrastructure with the real usage patterns of stablecoins in global payment flows.

Market Usage Patterns and Network Effects

Our analysis of transaction flows reveals a sharp divergence between stablecoin market capitalization and real economic activity:

- USDT consistently dominates actual consumer and business usage, accounting for roughly 80–85% of real-world flows, even though its market cap is more balanced relative to competitors.

- Much of the USDC supply remains idle on exchanges and trading platforms, highlighting its concentration in financial rather than commercial use cases.

- By contrast, USDT is entrenched in global payment networks, from small-scale merchants in Turkey and Brazil to remittance corridors across Latin America and Southeast Asia.

This adoption pattern reinforces strong network effects:

- Payment systems require both sender and recipient infrastructure to support the same stablecoin, which has positioned USDT as the global “export dollar” while USDC remains concentrated in U.S. and European markets.

- These differences suggest distinct addressable market segments and highlight the durability of USDT’s lead in global commerce.

Competitive Positioning Realities

The competitive landscape shows that basic performance characteristics such as speed and low cost have become commoditized. They are no longer sufficient as differentiating features.

- General-purpose blockchains optimize for broad functionality, but the resulting trade-offs limit their suitability for specialized payment infrastructure, creating opportunities for purpose-built settlement layers that align architecture directly with stablecoin usage.

However, technical optimization alone is not enough for market penetration. The payments market is characterized by:

- Strong network effects, where adoption depends on both senders and receivers.

- Path dependence, with entrenched relationships among exchanges, payment processors, and local infrastructure providers.

- These create significant barriers to entry, meaning successful solutions must combine both technical alignment and strategic market integration.

Conclusion

The evolution of crypto’s payments infrastructure has been shaped by incremental workarounds rather than deliberate design. This has created a mismatch between the assets driving adoption, Bitcoin and USDT, and the infrastructure they rely on.

Bitcoin, with over $2T in market capitalization, remains underutilized in financial applications and fragmented across custodial solutions, while USDT dominates global payments but depends on general-purpose blockchains like Ethereum and Tron, which face structural limits in cost, scale, and regulatory durability.

Plasma addresses these inefficiencies by re-architecting the base layer around Bitcoin and stablecoins:

- Stablecoins as the native gas asset: eliminates reliance on volatile utility tokens, enabling zero-fee USDT transfers, payroll, and remittances.

- pBTC as decentralized, omnichain Bitcoin: consolidates liquidity across chains via LayerZero’s OFT standard and enables productive deployment of Bitcoin in DeFi.

- Privacy and compliance features: confidential settlement channels align with enterprise requirements for predictable costs and operational security.

The implications extend across market segments. Enterprises gain cost-predictable, compliant settlement. Institutions can deploy Bitcoin treasuries productively. Retail users, particularly in emerging markets, unlock instant, low-cost remittances and payroll.

Plasma positions itself not as a general-purpose chain but as purpose-built settlement infrastructure for USDT and BTC. By aligning infrastructure with the assets that matter most, it bridges the gap left by Ethereum and Tron, supports real-world payment flows, and enables the next era of adoption across retail, enterprise, and institutional layers.

Plasma: The World of On-chain Payments

Bitcoin and USDT dominate crypto, yet both are second-class citizens-BTC fragmented across wrappers, USDT competing for general-purpose block space. Plasma rewrites this: stablecoins as native gas, pBTC as unified omnichain Bitcoin, building settlement rails for the assets that actually matter.

This piece was made in collaboration with the Exa Group team.

From “Sound Money” to Stable Money

Definition:

- TARP (Troubled Asset Relief Program) - U.S. program (2008) that bought troubled bank assets to stabilize the financial system.

- Stimulus packages - Government spending or tax measures to boost the economy during downturns.

In September 2008, the world watched a pillar of Wall Street crumble: “Lehman Brothers”, a 158-year-old investment bank, filed for bankruptcy after no buyer could be found.

Overnight, credit markets froze and trillions of dollars in complex mortgage-backed securities became worthless in spite of what ratings suggested. Governments scrambled: the U.S. launched TARP, central banks injected emergency liquidity, and stimulus packages rolled out worldwide.

For millions, the crisis wasn’t just an economic downturn, it was a sign “TradFi” couldn’t be trusted. Banks had taken reckless risks, regulators had looked the other way, and when it all collapsed, taxpayers were left holding the bill.

Three months after, on January 3rd 2009, the first Bitcoin block was mined, embedding a single headline: “Chancellor on brink of second bailout for banks.”

It referred to British Chancellor of the Exchequer, Alistair Darling, preparing yet another massive taxpayer-funded rescue for struggling banks (just months after the first).

The headline was a direct statement toward the very system that had just failed, a reminder, etched into Bitcoin’s first block, of why it existed.

Bitcoin entered the world as a total polar opposite: a fixed supply, no central authority, and a peer-to-peer network immune to bailouts and political manipulation. But, this “sound” money came with a trade-off: $-denominated volatility.

In traditional economics, money serves three functions:

- A medium of exchange,

- A store of value,

- And a unit of account.

Bitcoin excelled at the first two but failed on the third.

As crypto matured, one problem became obvious - people needed a way to hold value on-chain without constantly dealing with price swings.

Business owners wanted to invoice and pay predictably. Traders needed a way to lock in profits without fully cashing out. And everyday users wanted to participate in decentralization without volatility.

The tedious process of: (a) wiring funds to a bank, (b) waiting days for settlement, and (c) paying hefty fees along the way, created a demand for stable on-chain money.

The first to meet this demand was BitShares, with their BitUSD, launched in July 2014. The idea was ahead of its time: users could lock up $BTS (BitShares’ native token) as collateral to create BitUSD, which maintained its peg to the $ through smart contracts and market incentives.

However, the problem was that BitUSD’s peg relied entirely on the value of BTS. When BTS prices fell, collateral ratios could quickly slip below safety levels, triggering mass liquidations.

But, just four months later, in November 2014, Tether launched USDT - offering a simpler (fiat-backed) alternative where each token was redeemable 1:1 for U.S. dollars held in custody. USDT didn’t require overcollateralization or complex algorithms, and this simplicity is what allowed it to capture over $19.3M in volume & $1.45M in market cap in just one year.

To put it in perspective, at the time, $ETH was worth only ~$1, while $BTC hovered around $240.

Following USDT’s adoption, teams started searching for new ways to create stability without relying on a centralized issuer. The first major project was SAI (Single-Collateral Dai) by MakerDAO.

Launched on December 18th 2017, MakerDAO’s original system allowed users to lock ETH into Collateralized Debt Positions (CDPs) and mint SAI. While SAI did maintain a soft peg to the U.S. dollar through automated incentives and stability fees, relying only on ETH as collateral left it exposed to violent price swings - much like BitUSD.

To mitigate this risk - after exactly 2 years, on November 18th 2019 - MakerDAO launched Multi-Collateral Dai (DAI). The upgrade expanded the collateral set beyond ETH, improving risk diversification and capital efficiency.

It also introduced a more robust governance model, giving $MKR holders authority over critical parameters such as collateral onboarding, stability fees, and risk controls. With these changes, DAI became the first decentralised stablecoin to achieve broad adoption.

Meanwhile, traditional fiat-backed alternatives continued to grow in parallel. USDC launched on September 26th 2018 and positioned itself as a regulated, fully dollar-backed stablecoin with public attestations of reserves. It found its niche in compliant fintech integrations and became the dominant collateral in DeFi for a while.

Stablecoin Adoption & The Infra Gap

Today, stablecoins are crypto’s most adopted product by both usage and transaction velocity. The scale is difficult to overstate, given that Stablecoin’s Market Cap ($271.657B) is 1.6x bigger than the total DeFi TVL ($166.09B).

A common comparison used to depict the sheer scale of stablecoin usage is Visa’s Annual Payments Volume (APV). In 2024, Visa processed $13.2T in payments, while stablecoins moved $22T in unadjusted¹ on-chain volume, with an adjusted² figure of $5.67T (which excludes internal exchange transfers and MEV activity).

This adjusted figure has been on a climb for the past 12M, going from $432.3B all the way to $949.07B in daily volume, suggesting an increase in stablecoin demand.

Furthermore, the U.S. Genius Act, signed on July 18th 2025, recognises stables as formal payment instruments, putting them on par with other regulated financial rails like debit card networks, ACH transfers, and wire systems.

Notwithstanding, the core infrastructure for stablecoins hasn’t evolved at the same pace.

Stablecoins like USDT have become institutionally important, even holding the sector’s dominance with >60%, yet they still live on general-purpose chains that were never designed with them in mind, where:

- Transfers require volatile native gas tokens,

- and none of the underlying infra was purpose-built to meet the scale or compliance expectations of the institutions now entering the space.

This infra gap creates a massive imbalance. Despite moving almost as much annual volume as Visa and being recognized by governments as equal to traditional payment instruments, USDT still operates as a second-class citizen on infra that treats it as just another token.

Ironically, BTC faces a similar paradox. With a market cap larger than silver and a spot as the 7th most valuable asset in the world, BTC should be the most important building block in DeFi. Instead, most of it sits idle.

Existing “wrapped” solutions are little more than glorified custody, and even when BTC does make it into DeFi, it suffers from fragmentation: one wrapped version on Ethereum, another on Polygon, another on Arbitrum, each with its own liquidity pool and friction at every step.

To battle this, Plasma rethinks the foundation itself. Instead of treating stablecoins and Bitcoin as add-ons to a general-purpose chain, it makes them first-class citizens.

In Plasma’s design, stablecoins become the native gas asset, meaning transfers no longer require volatile tokens to move dollars on-chain. For institutions, this eliminates a key barrier to adoption. For users, it creates an experience that finally mirrors the simplicity of existing payment rails.

On the Bitcoin protocol side, Plasma introduces pBTC, secured by a decentralized verifier set rather than a single custodian. Unlike today’s fractured wrapped assets, pBTC is built using LayerZero’s OFT standard, which allows it to exist as one unified token across every connected chain.

By accommodating both stablecoins and Bitcoin at the base layer, Plasma positions itself to become the natural settlement rail for BTC-USDT activity. Together, these two assets represent the most important pillars of crypto - one as its largest store of value, the other as its most widely adopted medium of exchange.

1 - Volume from addresses that are labled as MEV Bots or Intra-Exchange, is considered an interlan transaction, or that have transacted >1k transactions or 10M transfer volume in any 30 day period.

2 - Volume from addresses that are labled as entities related to CEXs, DEXs, or others, or have not transactred >1k transaction or 10M transfer volume in any 30 day period.

The Plasma Stack: A Stablecoin-First and BTC-Native Blockchain

Plasma represents an architectural shift from general-purpose blockchains, positioning itself as infrastructure for Bitcoin and USDT settlement. The network is designed such as it:

- Commits state proofs to Bitcoin for security

- Maintains EVM compatibility through the Reth execution environment.

And to enable gasless USDT transfers at scale, Plasma employs two specialized validator sets:

1. One set is responsible general network security and consensus,

2. The other set processes USDT payments in a high-speed lane optimized for volume and cost efficiency.

PlasmaBFT

Plasma’s consensus layer, PlasmaBFT, secures the chain through a high-performance implementation of Fast-HotStuff written in Rust.

In traditional BFT protocols (e.g. HotStuff), finalizing a block is done through three phases - each producing a signed proof that a supermajority (more than 23) of validators agreed on that step:

- Prepare - The leader proposes a block, validators check its validity and vote to approve it;

- Pre-commit - Validators confirm that a supermajority approved the prepare phase, then “lock” onto that block to prevent forks;

- Commit - Validators confirm that a supermajority pre-committed, making the block final and irreversible.

Although this three-phase process does guarantee safety, it slows things down as every step requires network communication and coordination.

Fast-HotStuff trims this overhead with what’s called the two-chain commit rule:

If two consecutive blocks (N and N+1) both gather a supermajority, then N can be finalized immediately. This works because reaching a supermajority on block N+1 proves that validators were already locked on N when approving N+1, so the pre-commit phase is not needed.

In practice, the 3 phases collapse into 2:

- Phase 1 (Prepare) - vote on block N

- Phase 2 (Commit) - vote on block N+1, which finalizes block N

However, in edge cases where the network fails to hit the two consecutive supermajorities required for fast finality, PlasmaBFT falls back to the full three-phase commit protocol from classic HotStuff. This ensures that all honest validators securely "lock" onto the same block before finalisation, maintaining safety and liveness.

Once the fallback resolves, PlasmaBFT resumes the fast two-phase path.

But, it doesn’t stop there. With pipelining, multiple blocks can be worked on at once by overlapping their phases:

While validators are in the commit phase for block N, they can already be in the prepare phase for block N+1. The next block doesn’t have to wait for the previous block to fully finalize before starting its voting process.

It effectively keeps the network busy at all times - maximizing efficiency without sacrifice.

Additionally, by only selecting a subset of validators (committee) via a cryptographically secure, stake-weighted random process for each round, Plasma reduces communication overhead while still applying the same supermajority rules.

Consensus Rollout & Validator Incentives

Plasma uses a Proof of Stake mechanism for validator selection, so validators earn rewards by participating in consensus and signing blocks. But, unlike in normal PoS, misbehavior is handled through reward slashing instead of stake destruction.

This allows Plasma to align with institutional expectations (where unexpected loss of funds is unacceptable), while still incentivizing correct behavior.

Plasma’s consensus will launch in three phases:

- Trusted Validator Launch - A small set of known validators secures the network at mainnet launch for stability;

- Validator Expansion - The validator set grows to test performance and throughput with larger committees;

- Permissionless Participation - Public validator access enables real decentralization while maintaining supermajority safety and PlasmaBFT’s fast-path optimizations.

The Reth Execution Engine

Plasma's execution layer is built on Reth, a modern Ethereum client written in Rust that manages: state transitions, transaction processing, and EVM operations with complete EVM compatibility.

Every opcode, precompile, and execution behavior functions identically to Ethereum mainnet, making migration of existing contracts and tools easy.

Reth connects with the consensus layer through the same Engine API Ethereum has used since the Merge.

This separation of tasks allows PlasmaBFT to handle consensus and block ordering, while Reth focuses on transaction execution and state transitions:

- Block Proposal - the CL sends the ordered block (containing TXs) to Reth via the Engine API’s engine_newPayload call

- Transaction Validation - Reth validates each TX’s format, signature, nonce, and gas requirements before execution

- State Execution - Reth processes TXs sequentially

- State Root Calculation - After executing all TXs, Reth computes the new state root and TX receipt root using Merkle Patricia Tries (MPT) - used for storing and verifying data integrity

- Execution Confirmation - Reth returns the execution results, including gas usage, TX receipts, and the updated state root back to PlasmaBFT

- Block Finalization - PlasmaBFT incorporates the execution results into the final block header and completes the consensus process

Native BTC Bridge

Most BTC bridges today look decentralized on the surface, but peel back the layers and you’ll find either:

- A single custodian (like BitGo the issuer of $wBTC) holding everyone’s coins, or

- A small multisig that can freeze the vault at any time.

That’s the tradeoff users have accepted: if you want BTC in DeFi, you give up Bitcoin’s trust-minimized design.

Plasma’s native Bitcoin bridge changes this. Instead of custody, it’s powered by a network of independent verifiers that each run their own Bitcoin node. No single party controls the vault, and for BTC to move in or out, a quorum of verifiers must collectively sign off using threshold signatures (MPC/TSS) - meaning no individual ever holds the keys.

When a user deposits BTC into the Plasma vault on Bitcoin, the process doesn’t rely on a custodian to “promise” the funds are there. Instead, every verifier:

- Independently “sees” the deposit through their own Bitcoin node,

- Confirms it reached finality,

- And then broadcasts an attestation on-chain.

Those public attestations prove that BTC was received and carry the user’s mapped EVM address, which the depositor specified in the transaction metadata. Once a supermajority of verifiers agree, pBTC is minted directly to that address on Plasma, and the attestations sent on-chain.

Withdrawals work the same way:

Burning pBTC signals to the verifier network that BTC should be released back on Bitcoin. A quorum of verifiers validates the burn on Plasma, then collectively produces a threshold signature to unlock the Bitcoin.

The key is never concentrated anywhere, so no single verifier can move coins alone, because the signature is stitched together from fragments that only exist in aggregate.

But the trust model improvements are just part of the story.

Most BTC bridges today suffer from another critical flaw: liquidity fragmentation. Take wBTC for example - it exists as a separate, incompatible version on every chain. wBTC on Ethereum can't directly interact with wBTC on Polygon or Arbitrum without additional bridging steps, separate liquidity pools, and more complexity for users and protocols.

Plasma solves this by implementing pBTC using LayerZero's OFT (Omnichain Fungible Token) standard. Instead of creating isolated token instances per chain, pBTC operates as a single token across all LayerZero-connected chains. When you move pBTC from Plasma to Ethereum or any other supported chain, you're not bridging to a wrapped version - you're moving the same native pBTC token.

This creates a single liquidity pool for pBTC that spans the entire omnichain ecosystem.

Bridge Roadmap

Even though the current verifier network already has significant trust minimization compared to custodial alternatives, the bridge architecture is made with expansion in mind.

Plasma is actively tracking developments in Bitcoin's ecosystem that could enable even deeper security guarantees:

- BitVM-style Bitcoin validation via onchain verification circuits

- Zero-knowledge proofs for cross-chain state attestations

- Bitcoin opcode upgrades such as OP_CAT for custom verification logic

Stablecoin-Native Design

Zero-Fee USDT Transfers

Plasma implements contract-level paymasters that sponsor transfer and transferFrom functions through a sophisticated account abstraction (AA) system built on EIP-4337 and EIP-7702 standards.

The paymaster operates as a network-funded account that automatically covers gas fees using XPL token reserves when verified users execute basic USDT payments.

When users initiate transfers, the paymaster performs real-time eligibility verification by checking sender patterns, transaction frequency, and user reputation before automatically covering costs. How?

- By evaluating multiple lightweight verification methods including zkEmail attestations, zkPhone verification, Cloudflare Turnstile, and signature-based allowlists.

- Rolling caps on subsidized transfers (e.g., 5 per 24 hours) enforced through either contract storage or signature-bound counters.

Custom Gas Tokens

The protocol-managed paymaster leverages EIP-4337 standards, calculating gas costs through oracle-derived rates with slippage protection. Unlike third-party paymasters that charge markup fees and depend on external funding, Plasma's approach guarantees consistent, fee-free operation across applications.

Confidential Payments

Plasma’s shielded transactions hide amounts, recipients, and metadata while preserving selective disclosure for compliance. This targets enterprise use cases where operational privacy provides competitive advantages such as payroll distribution and supplier payments.

This technical implementation employs

- Stealth Addresses: One-time addresses that hide recipients. Each payment goes to a unique address only the recipient can access.

- Encrypted Memos: Private notes attached to transactions. Only holders of the decryption key can read the contents.

- Selective Disclosure Proofs: Users control exactly which transaction details to reveal and when. Full privacy by default, with verifiable proof capabilities for compliance or audits.

Competitive Landscape & Opportunity Sizing

Total Addressable Market (TAM)

We’ve all heard of the classic business metaphor:

“Better to be a big fish in a small pond, than a small fish in a big pond.”

Plasma is doing exactly that in the world of on-chain payments and yield market opportunities.

Instead of competing as another general-purpose chain with a technical innovation that doesn’t bring any merit, Plasma is laser focused on becoming the infrastructure for institutional use.

And this focus couldn’t be more timely.

TradFi players are increasingly exploring BTC treasury strategies - with MicroStrategy leading the herd with over 636,500 BTC ($~70b) in custody. Meanwhile, the payments industry is racing to build faster and cheaper rails for cross-border transactions, with stablecoins emerging as the clear winner for international settlement.

“Native BTC”: Tokenisation and Yield Market Opportunities

Even though it’s the largest crypto asset, BTC still remains unused across DeFi - with wrapper products removing all of its trust-minimized ideology.

As the most decentralised BTC wrapper solution, pBTC offers “Native BTC” DeFi opportunities that others just can’t mimic.

With over 242.6k BTC in wrapper solutions and 209.8k BTC (~86.5%) actually deployed across protocols & earning yield - pBTC’s base opportunity comes from retail users looking for safer ways:

- To use BTC across DeFi;

- To store BTC on, more accessible, EVM chains.

But, this retail demand is just part of the story.

Institutional and corporate adoption is catching on, with public and private companies now holding a combined ~1.38M BTC. That’s a stark difference compared to that start of the year where these same entities held only 547k BTC in custody.

This 833k BTC increase highlights a clear trend in institutional adoption that’s only accelerating. But, here’s the key insight: as more and more institutions get BTC into treasuries, their strategies will evolve from simple holding to active management.

For this, pBTC represents the perfect intermediary - as these players prioritize infrastructural safety over everything else.

On-chain payments: Cross-border payments and Payroll

In 2023, 184M people (2.3% of the world’s population) were reported to live outside of their country of nationality. Usually driven by economic opportunities, these migrant workers often find themselves sending money back to their families and community across borders.

These cross-border payments (or “remittances”) play a crucial role in supporting the economies of low & middle income countries (LMICs) - and, for some of them, even amount to half of their gross domestic product (GDP).

In 2024, remittance flows to LMICs came out to $685B, with the top 5 recipient countries being:

- India - $129B

- Mexico - $68B

- China - $48B

- Philippines - $40B

- Pakistan - $33B

These massive flows represent literal lifelines for millions of families across the world - but, they come with a hidden cost.

Take India for example. In 2023, India received a reported $16B in remittances from the US. At the average $200 transfer cost of 4.16% (Exchange Rate Margin + Fee), India lost $665M of that money to banks/FXs.

That’s $665M that hundreds of thousands or even millions of Indian households never received - and this pattern repeats across every major corridor.

Mexico, receiving roughly >$50B from the US annually, loses over $2.4B to fees at current transfer costs. Meanwhile, Nigeria, which receives $6B in remittance from the US, loses $180M.

The opportunity for Plasma here is clear. With their zero-fee USDT transfers, Plasma could eliminate the billion-dollar extraction that traditional rails impose on vulnerable populations each year.

A migrant worker could finally send the full $200 to their family in Guatemala, and not $187 after fees. Over time, this would amount to thousands of dollars saved per family - money that stays in the communities that need it most.

Remittances, however, represent only a part of Plasma’s reach. When we pair zero-fee USDT transfers with auditable confidentiality, Plasma opens the doors to a totally new market: on-chain payroll.

In 2023, the U.S. alone produced a total of $11.07T in wages and salaries across 134.06M employees.Thats 1.6B (12×134M) bank transfers annually - all of which incur fees to companies.

For simplicity, let’s assume those wages are paid monthly via ACH direct deposits. With flat fees ranging between $0.20-$1.50 per transfer (and a median of $0.85), U.S. companies are spending $1.37B annually just to move money to their employees’ accounts:

134.06M × 12 × $0.85 = $1.37B

Much like with remittances, money that can be better used by the companies sending out the transfers has to be wasted on fees.

With Plasma’s gasless USDT transfers, U.S. emoplyers would save ~$1.4B each year, while confidentiality adds another layer of value for both employers and employees:

- Employers - Salary data hidden from competitors while maintaining full auditablility

- Employees - Reduces fraud/theft targeting and protects from unwanted financial pressure

Sizing The Opportunity

Plasma sits at the intersection of three of the largest financial flows in the world:

- Savings and capital deployment - letting users earn yield on BTC without leaving DeFi.

- Cross-border payments - saving billions in remittance fees for migrant workers and families.

- Payroll - eliminating friction and fees in domestic and international wage payments.

Even modest adoption across each of these segments is enough for a multi-billion-dollar TAM. Sizing these opportunities across adoption possibilities, we get 3 distinct scenarios: Base, Bear, and Bull Case.

📊 Base Case Scenario:

- For pBTC, market capture assumes a 5% retail adoption of existing wrapped BTC users (~12k BTC) simply from seeking safer alternatives, plus a 3% institutional adoption (~41k BTC) as corporations begin exploring DeFi yield on treasury holdings.

Total pBTC capture: ~53k BTC ($5.7B) - For on-chain payments, a 1% remittance adoption ($6.85B) driven by cost savings awareness in key corridors like US-Mexico and US-India is realistic, alongside a 0.01% payroll adoption ($5B) from forward-thinking tech and remote-first companies prioritizing cost reduction and privacy.

Total on-chain payments capture: $11.85B

📉 Bear Case Scenario:

- As users stick with wBTC because of familiarity, it maintains its market monopoly through brand recognition and existing integration resulting in only a 0.5% retail adoption of existing wrapped BTC users (~1.2k BTC). Similarly, a 0.5% institutional adoption (~7k BTC) is limited by regulatory uncertainty and preference for established solutions.

Total pBTC capture: ~8.2k BTC ($890M) - For on-chain payments, remittance adoption is hindered by crypto literacy gaps in target demographics and regulatory barriers, resulting in only a 0.3% ($2.05B) capture, alongside a 0.005% payroll adoption ($2.5B) due to long enterprise sales cycles and strong resistance from traditional payroll providers.

Total on-chain payments capture: $4.55B

📈 Bull Case Scenario:

- For pBTC, market capture assumes 15% retail adoption of existing wrapped BTC users (~36k BTC) as crypto UX improves dramatically and trust-minimized solutions gain recognition, plus 8% institutional adoption (~110k BTC) driven by widespread corporate DeFi strategies and clear regulatory frameworks favoring decentralized solutions.

Total pBTC capture: ~146k BTC ($15.8B) - For on-chain payments, a 5% remittance adoption ($34.25B) as crypto becomes mainstream in emerging markets with government support and infrastructure improvements, alongside 0.05% payroll adoption ($25B) from progressive enterprises embracing crypto-native operations.

Total on-chain payments capture: $59.25B

Competitive Landscape

Tron's Structural Constraints and Market Reality

Despite processing the majority of USDT daily transaction volume (50>%), Tron faces fundamental architectural limitations that create opportunities for purpose-built alternatives:

- Lack of modern scaling capabilities and institutional-grade infrastructure features

- Rising stablecoin transfer costs

- Centralization concerns, leading to discomfort with maintaining significant inventory exposure

- Geographic concentration in Eastern markets, add costs without providing strategic benefits

Ethereum’s Payment Flow Limitations

Ethereum remains foundational for stablecoin issuance and large-value transfers where gas costs are negligible, but it is economically unviable for sub-dollar payments. Its general-purpose architecture forces stablecoin flows to compete with other applications for block space, resulting in unpredictable fees and latency that undermine its suitability as a retail payment infrastructure.

Infrastructure Mismatch in Emerging Markets

The limitations of current stablecoin infrastructure are most visible in emerging markets, where USDT demonstrates its strongest adoption patterns across remittances and local commerce. However, Ethereum’s cost structure renders small-value retail transactions economically unfeasible.

Ethereum continues to function effectively as a settlement layer for high-value transfers, but it lacks the characteristics required for day-to-day retail payments. This gap underscores the need for infrastructure purpose-built to support stable, predictable, and scalable consumer transactions.

Plasma directly addresses these constraints through specialized design choices:

- Protocol-managed paymasters remove dependence on volatile gas tokens, ensuring predictable costs in USDT.

- Dedicated validator sets optimize for USDT throughput without competing against general-purpose block space.

Together, these features align infrastructure with the real usage patterns of stablecoins in global payment flows.

Market Usage Patterns and Network Effects

Our analysis of transaction flows reveals a sharp divergence between stablecoin market capitalization and real economic activity:

- USDT consistently dominates actual consumer and business usage, accounting for roughly 80–85% of real-world flows, even though its market cap is more balanced relative to competitors.

- Much of the USDC supply remains idle on exchanges and trading platforms, highlighting its concentration in financial rather than commercial use cases.

- By contrast, USDT is entrenched in global payment networks, from small-scale merchants in Turkey and Brazil to remittance corridors across Latin America and Southeast Asia.

This adoption pattern reinforces strong network effects:

- Payment systems require both sender and recipient infrastructure to support the same stablecoin, which has positioned USDT as the global “export dollar” while USDC remains concentrated in U.S. and European markets.

- These differences suggest distinct addressable market segments and highlight the durability of USDT’s lead in global commerce.

Competitive Positioning Realities

The competitive landscape shows that basic performance characteristics such as speed and low cost have become commoditized. They are no longer sufficient as differentiating features.

- General-purpose blockchains optimize for broad functionality, but the resulting trade-offs limit their suitability for specialized payment infrastructure, creating opportunities for purpose-built settlement layers that align architecture directly with stablecoin usage.

However, technical optimization alone is not enough for market penetration. The payments market is characterized by:

- Strong network effects, where adoption depends on both senders and receivers.

- Path dependence, with entrenched relationships among exchanges, payment processors, and local infrastructure providers.

- These create significant barriers to entry, meaning successful solutions must combine both technical alignment and strategic market integration.

Conclusion

The evolution of crypto’s payments infrastructure has been shaped by incremental workarounds rather than deliberate design. This has created a mismatch between the assets driving adoption, Bitcoin and USDT, and the infrastructure they rely on.

Bitcoin, with over $2T in market capitalization, remains underutilized in financial applications and fragmented across custodial solutions, while USDT dominates global payments but depends on general-purpose blockchains like Ethereum and Tron, which face structural limits in cost, scale, and regulatory durability.

Plasma addresses these inefficiencies by re-architecting the base layer around Bitcoin and stablecoins:

- Stablecoins as the native gas asset: eliminates reliance on volatile utility tokens, enabling zero-fee USDT transfers, payroll, and remittances.

- pBTC as decentralized, omnichain Bitcoin: consolidates liquidity across chains via LayerZero’s OFT standard and enables productive deployment of Bitcoin in DeFi.

- Privacy and compliance features: confidential settlement channels align with enterprise requirements for predictable costs and operational security.

The implications extend across market segments. Enterprises gain cost-predictable, compliant settlement. Institutions can deploy Bitcoin treasuries productively. Retail users, particularly in emerging markets, unlock instant, low-cost remittances and payroll.

Plasma positions itself not as a general-purpose chain but as purpose-built settlement infrastructure for USDT and BTC. By aligning infrastructure with the assets that matter most, it bridges the gap left by Ethereum and Tron, supports real-world payment flows, and enables the next era of adoption across retail, enterprise, and institutional layers.

.svg)

{kind=link}