The HyperLiquid Stack: BuilderCodes, CoreWriter, HIP-3, and Read Precompiles

On-chain perps always faced the same trilemma: UX, decentralisation, or sustainability. Hyperliquid cracked it with their L1, but that was just the start. Builder Codes, HIP-3, and CoreWriter now transform it from a DEX into a financial infra stack where anyone can launch markets without compromise.

This piece was made in collaboration with the Obejctive Labs team.

Sector Genesis: From CEX to DEX Perps

Definition:

- "Rolling" - Closing a position in a futures contract as it approaches expiration and simultaneously opening a new one in a later-dated contract (allowing continuous exposure without settlement).

- "Arbitrage" - Exploiting price differences between futures and spot markets (or between different exchanges) to make risk-free or low-risk profits, in turn keeping futures prices close to fair value.

In 1992, Nobel Prize-winning economist Robert Shiller, frustrated by the friction of rolling futures contracts to maintain continuous exposure, theorised the idea of Perpetual Futures Contracts.

Unlike normal futures contracts that: (a) expired quarterly, (b) required "rolling" to maintain positions, and (c) kept prices close to spot through arbitrage, Shiller's perpetuals would have no expiration date.

Instead, they would use a funding mechanism - periodic payments between long and short holders based on the contract's deviation from spot price - to keep prices anchored without settlement.

This way:

- Rolling overhead was eliminated - no more closing expiring positions and opening new ones;

- Basis risk was minimal - traders wouldn't lose money from unfavourable price differences between contract months during rolls.

However, traditional finance never adopted this model; The idea remained theoretical for decades as there wasn’t enough demand for such products.

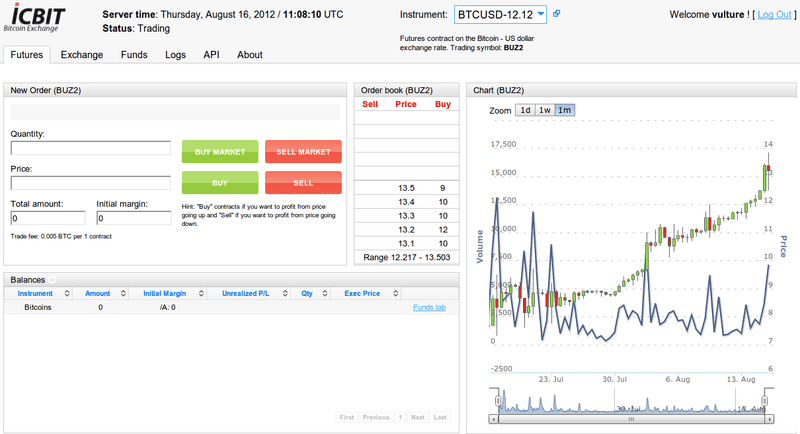

Finally, in 2011, Alexey Bragin developed the first practical implementation of perpetual futures at ICBIT. Specifically designed for cryptocurrency trading, his "inverse perpetual" used Bitcoin as margin, solving licensing issues for crypto exchanges (all operations could be settled in crypto) while providing leverage and shorting capabilities.

Bragin’s product paved the way for even more developed, mainstream perpetual futures products. The first of which was BitMEX’s XBTUSD perpetual swap. Launched in 2016, after their traditional quarterly futures failed to gain traction, XBTUSD concentrated all liquidity into its contract, creating the deep, 24/7 market that crypto traders desperately needed.

The product became wildly successful, handling $757.6M worth of volume in the first year of its launch. This led BitMEX to launch the first perp product without BTC as the margin - XBTCUSDT.

In subsequent years, more notable names followed in BitMEX's steps:

- Bybit launched its BTCUSD inverse perpetual in March 2018, building its entire exchange around the perpetual futures model;

- OKX (formerly OKCoin) integrated its BTC/USD inverse perpetual in December 2018;

- While Binance Futures followed in September 2019, recording an impressive $5.6B in trading volume within its first month of their BTC/USDT perpetual contract launch.

Until recently, perpetual futures were only accessible through centralised venues. In order to have access to these features, users had to abandon the core ethos of blockchain: self-custody and decentralisation. They were forced to deposit assets with centralised middlemen, reintroducing the very custody risks and regulatory vulnerabilities that crypto was meant to eliminate.

It all changed however with dYdX’s V2 launch in April 2020. As the first major on-chain perpetuals exchange, dYdX’s CLOB model allowed users to access leveraged perpetual futures while maintaining full custody of their assets.

Although it did open the doors for a totally new sector, the protocol still had its limits. Namely, as it was launched on Ethereum Mainnet, high gas fees and throughput limitations made small trades uneconomical, leading to poor user experience during volatile periods.

To address these fundamental bottlenecks, dYdX V3 launched in August 2021, migrating to the StarkEx Layer 2 and achieving CEX-like performance by solving the gas and speed limitations of V2. However, this came at a significant cost: it introduced an off-chain orderbook and a sequencer with trust assumptions - a clear step backwards in terms of decentralisation compared to the previous version.

The coming period was marked by teams experimenting with all kinds of different architecture, mainly motivated by introducing novel functionality or improving UX & speed.

GMX (originally Gambit) was first, launching in September 2021 with a multi-asset liquidity pool (GLP) as the direct counterparty to all trades. The model’s simple UX and minimal fees came with a major trade-off: LPs carried the full PnL risk of traders, effectively betting against all users.

Two months later, in November 2021 Drift V1 launched on Solana, trying to bridge the gap between AMMs and orderbooks with their Dynamic AMM (DAMM). Their design pulled liquidity from an AMM while still benefiting from on-chain orderbook price discovery and reduced slippage.

Level Finance launched in January 2023, on the BNB chain, with a tranche-based liquidity model where LPs could choose specific risk tiers for more precise capital allocation. But, this added precision also meant more operational nuance for the team.

Finally, in April 2023, Vertex launched on Arbitrum with a hybrid AMM + orderbook model, offering cross-margining to combine deep liquidity with efficient trading UX. However, the dual model required careful coordination between both systems.

Despite steady innovation, no protocol had yet cracked the fundamental trilemma: delivering CEX-like performance without compromising on decentralisation or sustainability. Each new design pushed the frontier forward, but always at a cost - some traded decentralisation for speed, others achieved scale but broke their economic models. The trade-offs seemed unavoidable.

This climate perfectly set the stage for HyperLiquid.

Rather than building on top of existing infrastructure and accepting its limitations, HyperLiquid took a 180º approach, creating a purpose-built L1 chain optimized specifically for perpetual futures trading.

By controlling the entire stack (from consensus to execution), HyperLiquid eliminated the external dependencies that plagued all previous protocols.No more Ethereum gas fees, Solana outages, or L2 sequencer risks.

No more choosing between decentralisation and performance.

HyperLiquid's architecture brings what the space has been looking for since dYdX's first on-chain attempt: truly decentralised perps with sub-millisecond execution, 0 gas fees for tradingTXs, and an economic model that aligns all participants.

.png)

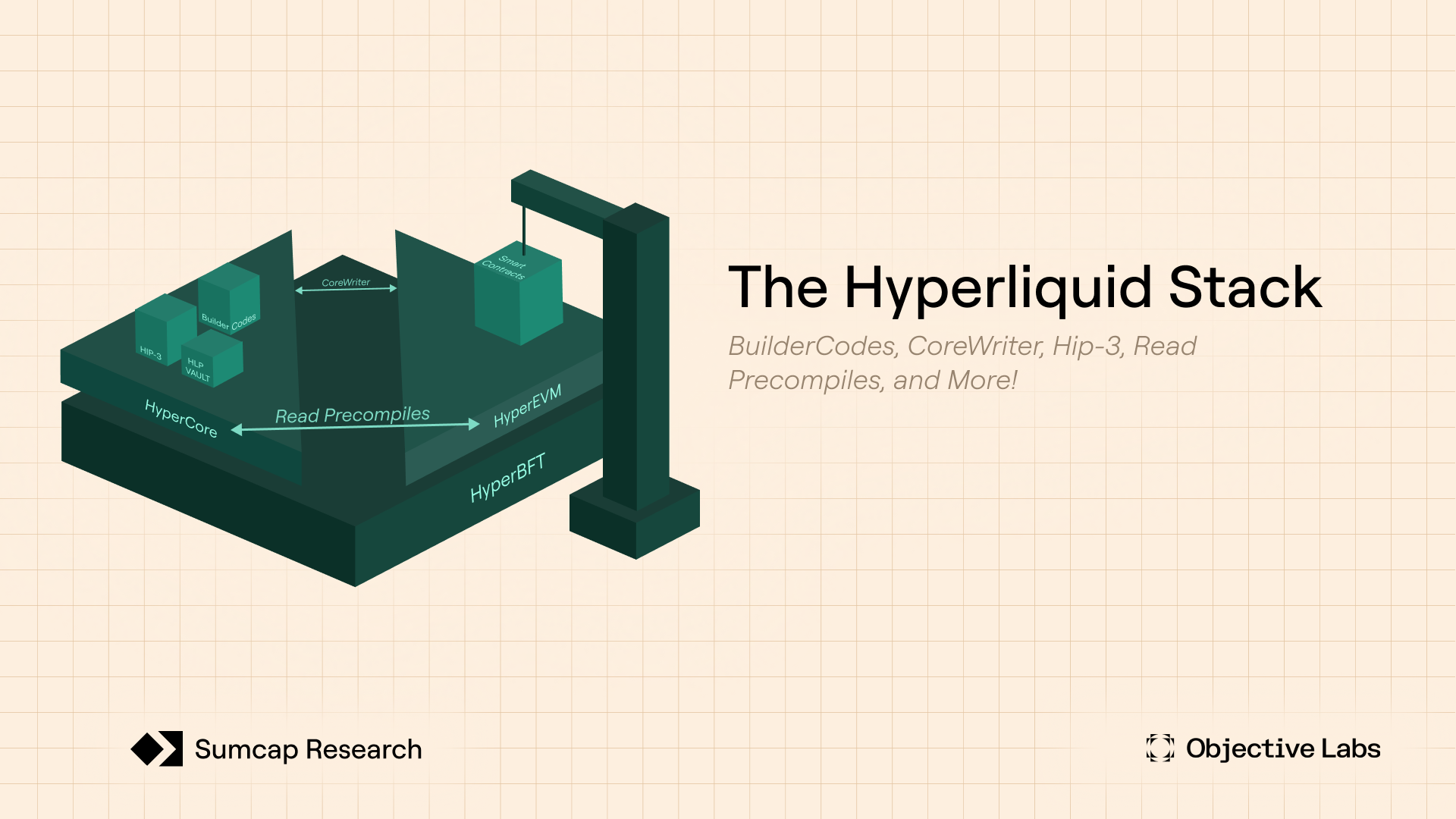

The Hyperliquid Stack

Hyperliquid is best explained as a high-performance technology stack for on-chain finance, built on three core pillars:

- HyperBFT Consensus: The heart of Hyperliquid and a breakthrough consensus algorithm that provides the low latency and high throughput that matches the performance of CEXs.

- Dual Execution Environment: HyperCore, a Layer 1 optimised for perpetual futures, and HyperEVM, a general-purpose EVM chain with full smart contract capabilities.

- Open Extensions: Hyperliquid opens its ecosystem to the world through extensions like Precompiles and CoreWriter, which merge smart contract DeFi with HyperCore, and Builder Codes and HIP-3, which invite externals to create their own markets and access liquidity.

These reinforce the core principles of DeFi: transparency, removing intermediaries and breaking down information silos, and they are all designed to generate revenue for $HYPE token holders.

HyperBFT: A Foundation for Speed and Security

Having originally launched with Tendermint, Hyperliquid has since transitioned to a fully custom consensus protocol called HyperBFT. HyperBFT is designed to maximize throughput and finality, enabling Hyperliquid’s fully on-chain order book to match (and in some cases exceed) the performance of centralised exchanges.

At its core, HyperBFT is a hybrid PoS-BFT algorithm inspired by the HotStuff protocol. It achieves a median block time of just 0.07s with end-to-end latency at 0.2s and a practical upper limit of 200,000 transactions per second. Block production is managed by a closed validator set (staking threshold: 10,000 HYPE), with leaders rotating each round to protect against downtime or malicious behavior. As a BFT-based system, HyperBFT guarantees immediate finality and eliminates chain re-orgs, giving traders confidence that transactions are immutable once confirmed.

That said, HyperBFT is not without tradeoffs. Its opinionated design strongly prioritises speed and scalability at the cost of broader decentralisation and validator diversity. In other words, it optimises for performance first, while making conscious compromises on the openness and security assumptions.

Dual Execution with HyperCore and HyperEVM

A big part of what makes Hyperliquid different is the way it splits execution into two layers that work hand in hand: HyperCore and HyperEVM. This structure lets the system deliver both the raw speed traders demand and the flexibility developers expect.

HyperCore is the Hyperliquid’s exchange engine, managing spot and perpetual order-books, liquidations, and margin trading directly at the protocol level. Thanks to HyperBFT’s exceptional speed and finality guarantees, HyperCore can handle hundreds of thousands of orders per second while giving users a seamless, exchange-like experience. Features like copy trading, market making vaults, and the clearinghouse are all native to this layer.

HyperEVM extends that foundation by adding a fully EVM-compatible smart contract environment, sharing consensus and state with HyperCore. That means developers can deploy familiar EVM contracts while also interacting directly with HyperCore’s financial primitives, pulling real-time prices or executing trades through built-in system contracts. This creates room for lending markets, structured products, or yield strategies that plug seamlessly into Hyperliquid’s liquidity and trading infrastructure.

This unified dual execution environment provides several strategic advantages that position Hyperliquid as a leader in DeFi innovation, including:

- Enhanced performance and efficiency through modular architecture that specialises each layer for specific function.

- Seamless interoperability through a unified state, allowing HyperEVM smart contracts to interact directly with HyperCore.

- Unified security with both layers secured by a shared validator set under HyperBFT consensus, reinforced by a transparent on-chain order book and oracle defenses.

A Unified Financial Stack

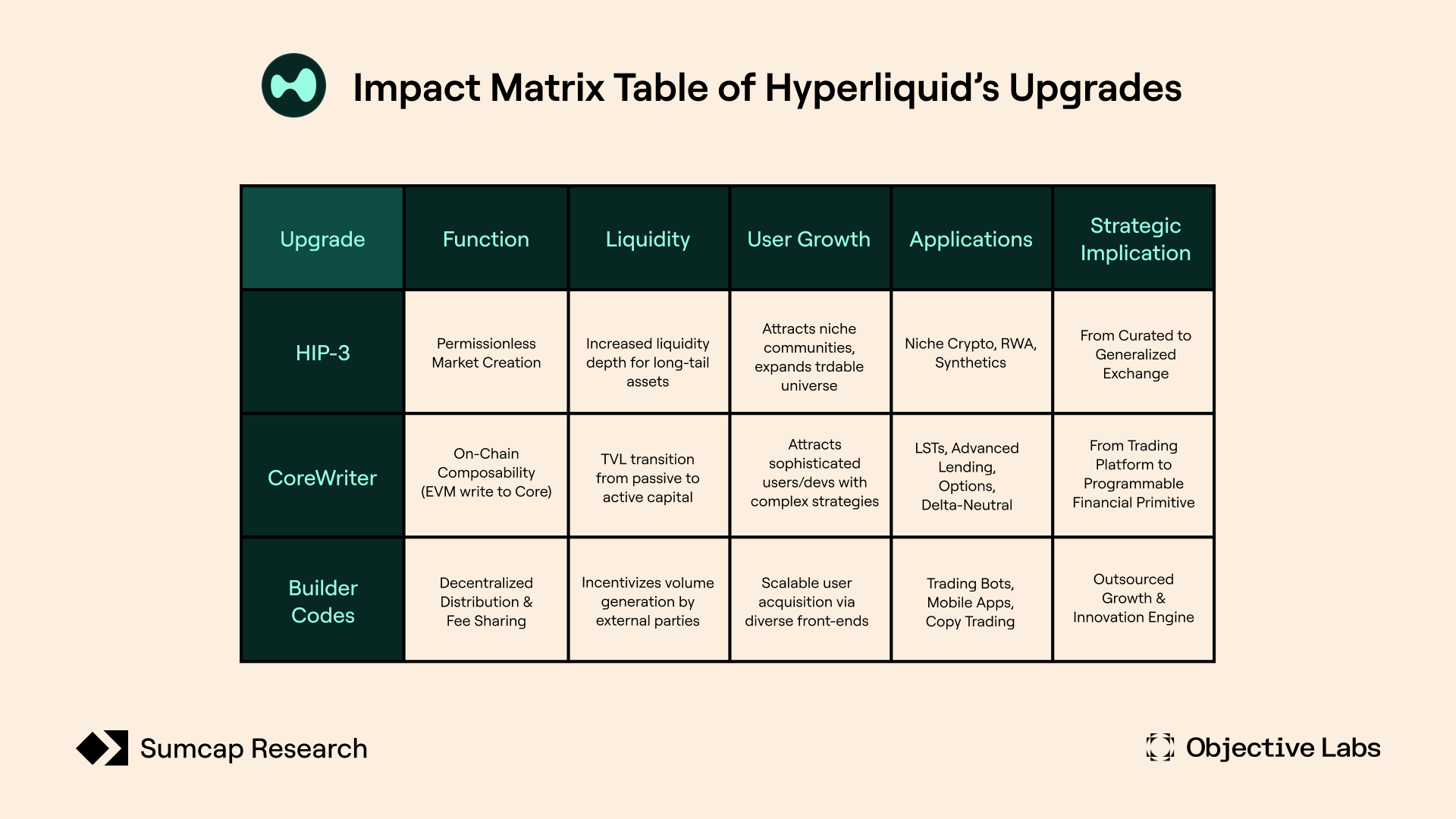

While we’ve outlined Hyperliquid’s architectural principles, architecture alone doesn’t create value - it’s what builders can do with it that matters. To enable this, Hyperliquid developed five core components: Builder Codes, Read Precompiles, CoreWriter, HIP-3, and the HLP Vault.

Together, these innovations form a unified financial stack where:

- Front-ends become revenue-sharing partners (Builder Codes)

- Native data access reduces external dependencies (Read Precompiles)

- Core actions are programmable (CoreWriter)

- Market creation becomes permissionless (HIP-3)

- Market-making is democratised (HLP)

De facto turning Hyperliquid’s infrastructure into a powerful economic engine for builders. The outcome? Opening the door to new business models, reducing time-to-market and lowering operational costs - all fully on-chain, while maintaining custody and performance intact.

Builder Codes: Democratising Liquidity

Historically, launching an exchange meant building a very heavy infrastructure from zero. Teams had to build matching engines, design custody models and navigate all sorts of extensive technical and regulatory barriers - each step adding costs, complexity and delay before the final product could go live.

Hyperliquid shifts this paradigm with Builder Codes, allowing any team to plug their front-end into Hyperliquid’s orderbook at no cost, letting builders earn revenue via a shared fee (Builder fee) when users trade through their interface. Developers are able to leverage Hyperliquid’s battle-tested core infrastructure granting new liquid venues faster and at a fraction of the cost. This creates a flywheel effect where:

More venues → More volume → Pulls in more liquidity → Reduces the slippage & attracts new traders → Even more volume → More revenue for builder codes → Attracts more builders

.png)

This flywheel could go a step further with the recently proposed Staking Referral Program.

When implemented, Builder Codes exchanges that stake $HYPE at a higher tier than their referred users could capture up to 100% of their fee differential - opening novel incentive dynamics between front-ends that might share this revenue with high-volume traders, permitting them a more cost-efficient trading and generating higher volumes for Hyperliquid.

That said, some critical voices argue that despite attracting additional volume, this could effectively result in net lower revenue for Hyperliquid, as a share of the revenue would be shared with front-ends. In any case, the proposal is still under research, so final implementation details are subject to changes.

Read Precompiles: A complement to Oracles

Oracles are a critical infrastructure component in the DeFi ecosystem - enabling access to external data and powering countless dApps. But as an external dependency, they come with tradeoffs: architectural complexity, high costs and additional trust assumptions.

In the Hyperliquid ecosystem, Read Precompiles function as the first bridge between HyperCore and HyperEVM. Rather than relying on third party oracles, they enable smart contracts direct read access to HyperCore native-protocol data.

A native dApp requiring position details, users equity, staking info or both spot/perps market prices can rely on HyperCore information directly, instantly and cost-free. For teams innovating on the Hyperliquid ecosystem, this helps reduce costs and operational overhead by removing unnecessary oracle calls, while simplifying system architecture.

.png)

Note: Read Precompiles are optimised for Hyperliquid native applications. For projects requiring non-native data (e.g. BTC price), traditional oracles may provide a more globally aggregated perspective.

CoreWriter: Elevating Trustless DeFi

Many applications in DeFi are neither decentralised nor permissionless. In many cases, operations still rely on multisigs and manual intervention, especially common in LST/LRT protocols or other liquid wrappers. These dependencies create friction, introduce trust assumptions, and limit the automation potential of on-chain systems.

Hyperliquid bridges this gap with CoreWriter, the natural evolution from read-only precompiles to bidirectional access. Whereas Read Precompiles only allowed contracts to pull data, CoreWriter enables smart contracts to also push instructions back into HyperCore.

With this feature, HyperEVM applications can interact with HyperCore, removing the operational barrier between the two environments. Some of the actions that can be performed with this feature are:

- Submitting orders to HyperCore;

- Transferring assets between accounts;

- Depositing into vaults;

- Staking user balances.

With all of this happening under custom on-chain logic, HyperEVM becomes HyperCore’s programmable layer.

.png)

This shift unlocks new design space for permissionless protocols, making it possible to build fully on-chain applications that interact with HyperCore without custodial intermediaries or manual intervention. It represents a fundamental step toward a more automated and trust-minimised DeFi, a topic explored in greater detail later in this article.

HIP-3: Permissionless market creation

Market creation has historically been a closed process, controlled by a few parties and shaped by their interests. This gatekeeping often made the launch of new markets slow, opaque, limited and often inaccessible to smaller teams.

HIP-3 proposes to change that, with the aim of democratising perpetual market creation. Under HIP-3, any user or project staking 1M $HYPE can deploy new markets directly into HyperCore.

Deployers become accountable for maintaining market health - keeping oracle feeds accurate and providing market-making to ensure smooth trading. Failure to meet these responsibilities could result in slashing of the 1M $HYPE stake, aligning incentives with users and the core protocol. In exchange, Hyperliquid shares its matching engine and up to 50% of the trading fees generated by the pair, incentivizing deployers to focus on high-demand and well-liquified markets.

This permissionless approach opens the door to a much wider space, enabling not just more crypto pairs, but also commodities, forex, ETFs, and alternative quote assets. It also widens the opportunity to entirely new business models such as borrowing $HYPE to bootstrap market deployment or decentralised HIP-3 market maintenance collectives.

.png)

By encouraging broader participation in $HYPE staking, HIP-3 not only diversifies available markets but also strengthens network security. Resulting in a more open, competitive, and innovative sector where market deployment and maintenance becomes an edge.

HLP: Permissionless and verifiable Market Making

Many DeFi projects face intense pressure to bootstrap liquidity through predatory market-making agreements, which often grant preferential terms to a single counterparty at the expense of the broader community.

HLP offers an alternative: a permissionless, community-driven and verifiable liquidity vault where anyone can deposit USDC to participate in market-making.

With this capital, the protocol provides liquidity serving as counterparty and executor, ensuring deep and fast execution. In return, the HLP captures exchange fees (maker/taker, liquidation penalties, and funding rate payments) and any profit from the spread or positions it absorbs, distributing it proportionately among the liquidity providers.

HLP allowed Hyperliquid to operate smoothly in its early stages, even before attracting external market makers. Over time, HLP has consistently delivered competitive returns to depositors while significantly improving the trading experience - lowering slippage, tightening spreads, and making liquidations more efficient.

Together, these components elevate Hyperliquid from a simple perps platform or conventional L1 into a full-fledged infrastructure layer - one that lets builders bypass typical liquidity and operational hurdles to focus on product differentiation, user experience, and target markets, without reinventing core primitives.

In the following sections, we’ll explore what this enables in practice: the products teams are already shipping using Hyperliquid’s stack

Competitive Landscape

Hyperliquid’s recent performance is remarkably strong when compared to its competitors - a success driven by key metrics across market share, user adoption, fees, revenue and number of perps listing.

Market Performance and Dominance

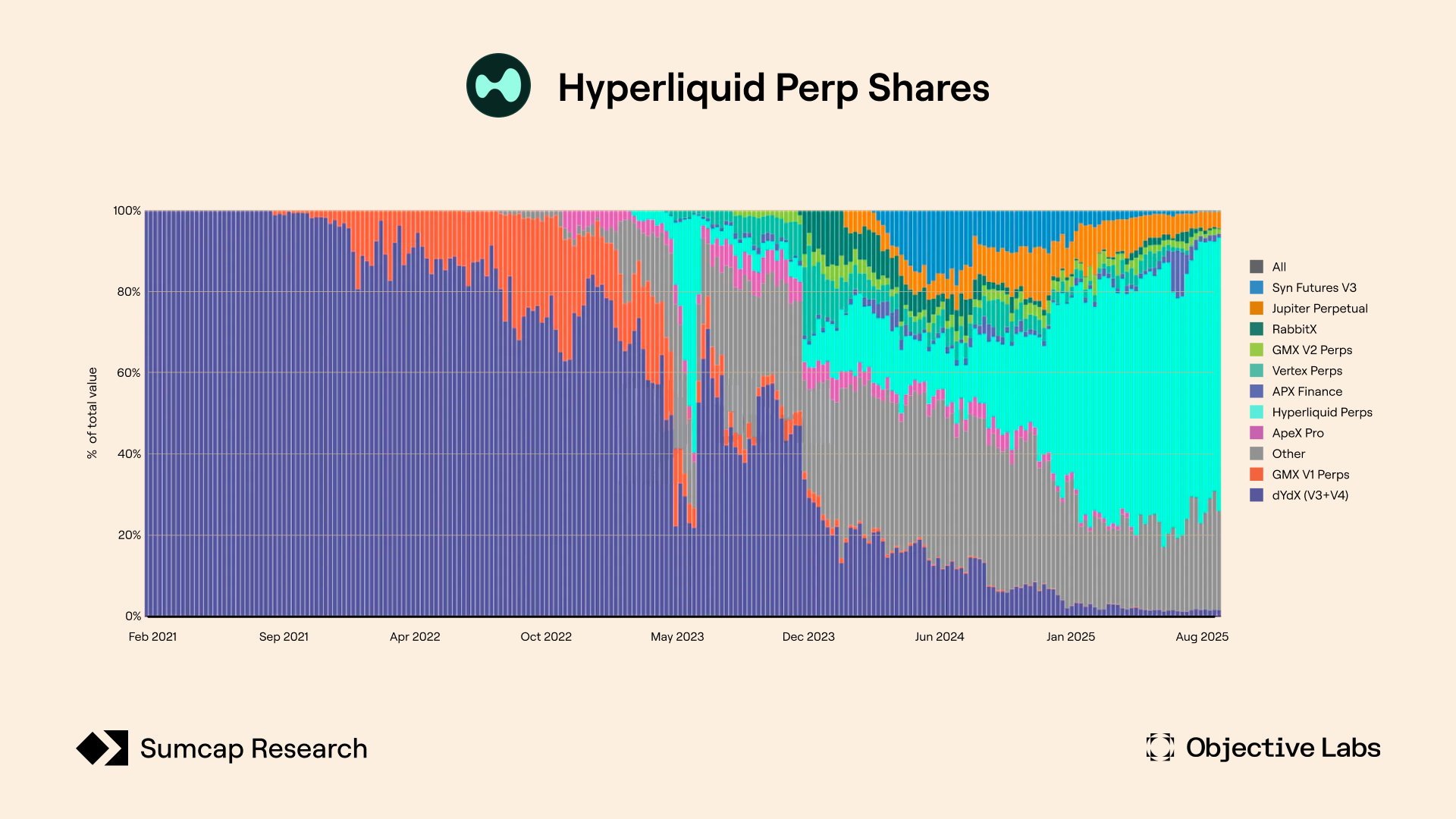

Hyperliquid has rapidly established itself as the dominant player in the on-chain perpetual futures market, commanding market share estimated between 50% and 65% in 2025.

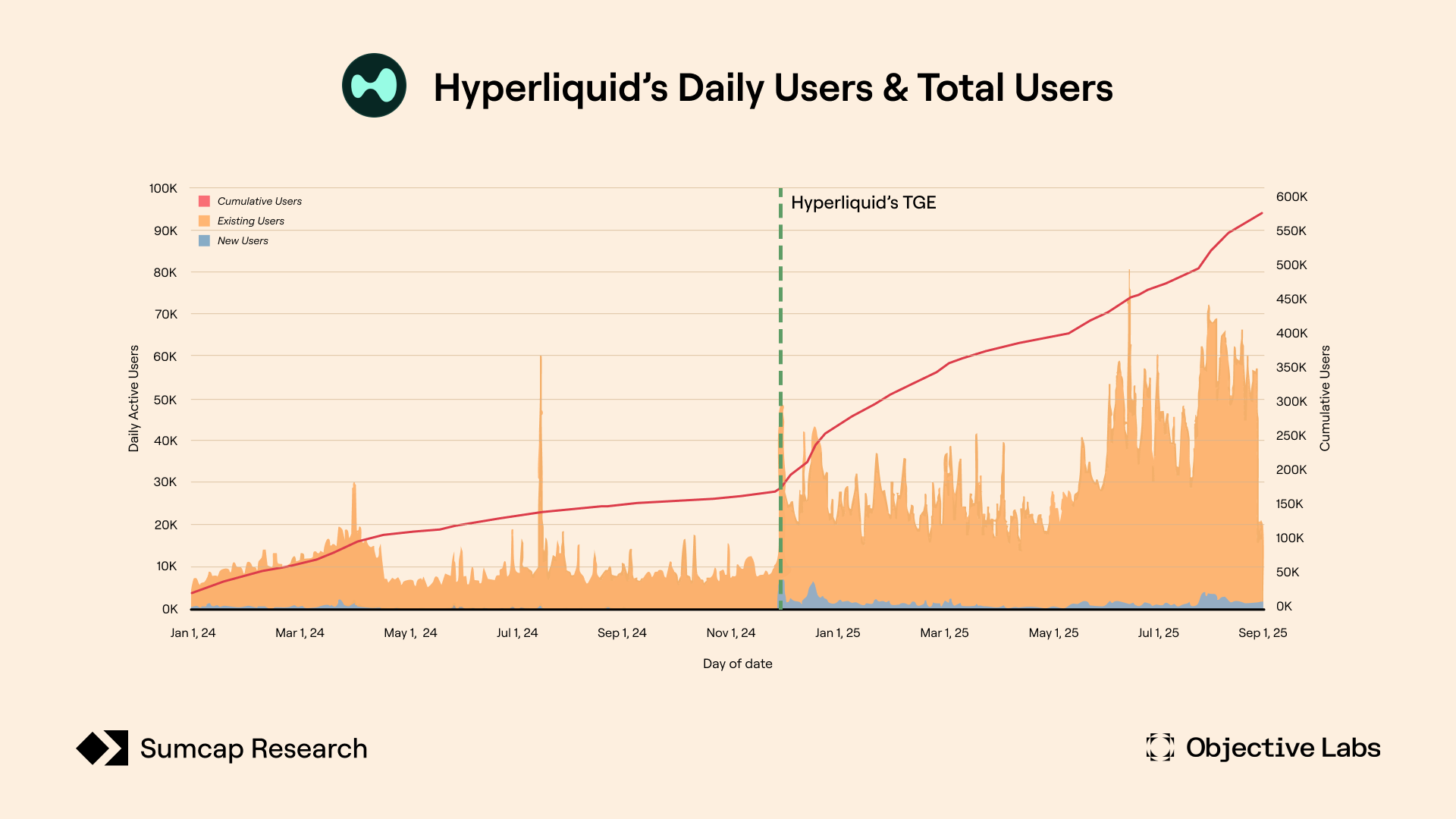

Its growth trajectory has been remarkably steep, beginning in early and throughout 2023 when it started gaining significant traction in the decentralised derivatives space. A major catalyst for its rapid expansion was the Token Generation Event (TGE) held on November 29, 2024. Counter to the usual trend, trading volumes on Hyperliquid have surged dramatically after TGE, further accelerating market capture. By late 2024, Hyperliquid was already servicing more than half of the perp market, with current market share nearing 70%.

Hyperliquid has profoundly reshaped the decentralised perp landscape. It has practically erased market share of once-established protocols like dYdX and GMX (which are now widely recognized as legacy). The remaining market is scattered across recent entrants building within the new paradigm commanded by Hyperliquid. However, having built an enormous liquidity moat, Hyperliquid still lacks a natural predator.

Since launch it has grown the pie for on-chain perpetuals, rekindling hope for decentralised trading as a viable alternative to established centralised venues. While previously the entire sector serviced $10-20B in weekly volume, >$100B weeks are not uncommon nowadays.

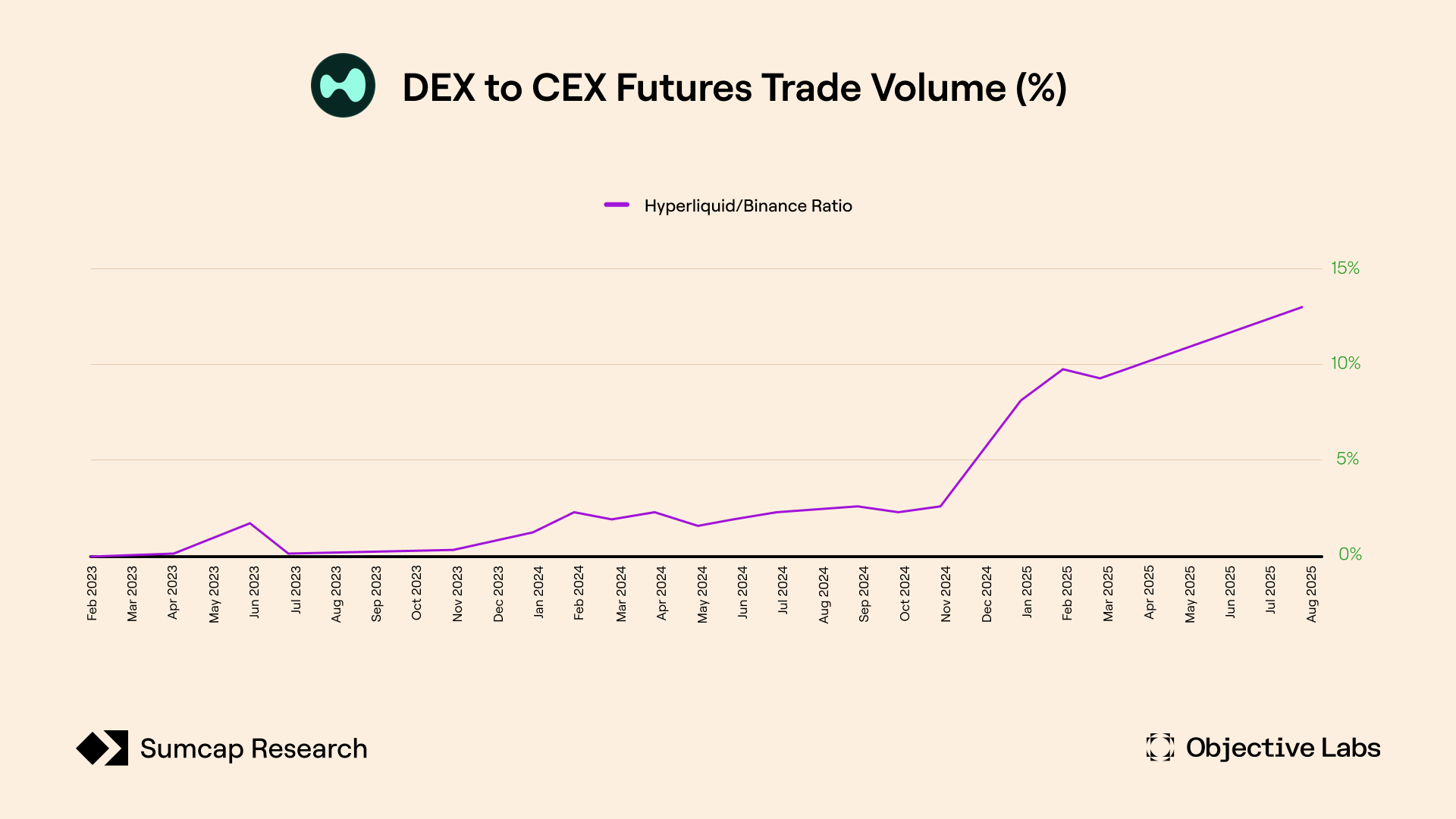

As the top dog in the DEX space, Hyperliquid has built a deep liquidity moat and a cult-like following, enough to now credibly compete with centralised giants like Binance, processing 12% of its volume in July 2025.

The broader DEX to CEX futures trade volume ratio has seen a marked increase in tandem with Hyperliquid’s rise. For most of 2022 and 2023, decentralised exchanges represented only around 1-3% of total futures trade volume relative to CEXes, now surpassing 10% in mid-2025. This shift evidences that Hyperliquid is not only dominating decentralised perpetual futures but is also significantly contributing to the overall migration of perp traders on-chain.

User Adoption and Platform Engagement

In 2025, Hyperliquid continued to expand its footprint in decentralised perps, combining rapid new user growth with sustained, high-volume engagement. It’s a rare case where a token launch didn’t just reward early users - it supercharged momentum, turning well-compensated traders into vocal evangelists. The days following the TGE were electric: over 11,000 new accounts were created within 48 hours, and daily active users have continued to hit new highs week after week.

Today, the platform onboards an average of 1.7k new traders every day with DAU rising from around 10k pre-TGE to over 50k in the past month. It’s not only more people in the door but more and more traders are sticking around and trading regularly. Hyperliquid’s user numbers are even more in comparison with competitors such as Jupiter with around 400 daily new users and nearly 6k in DAU, and edgeX at fewer than 100 daily new users.

.png)

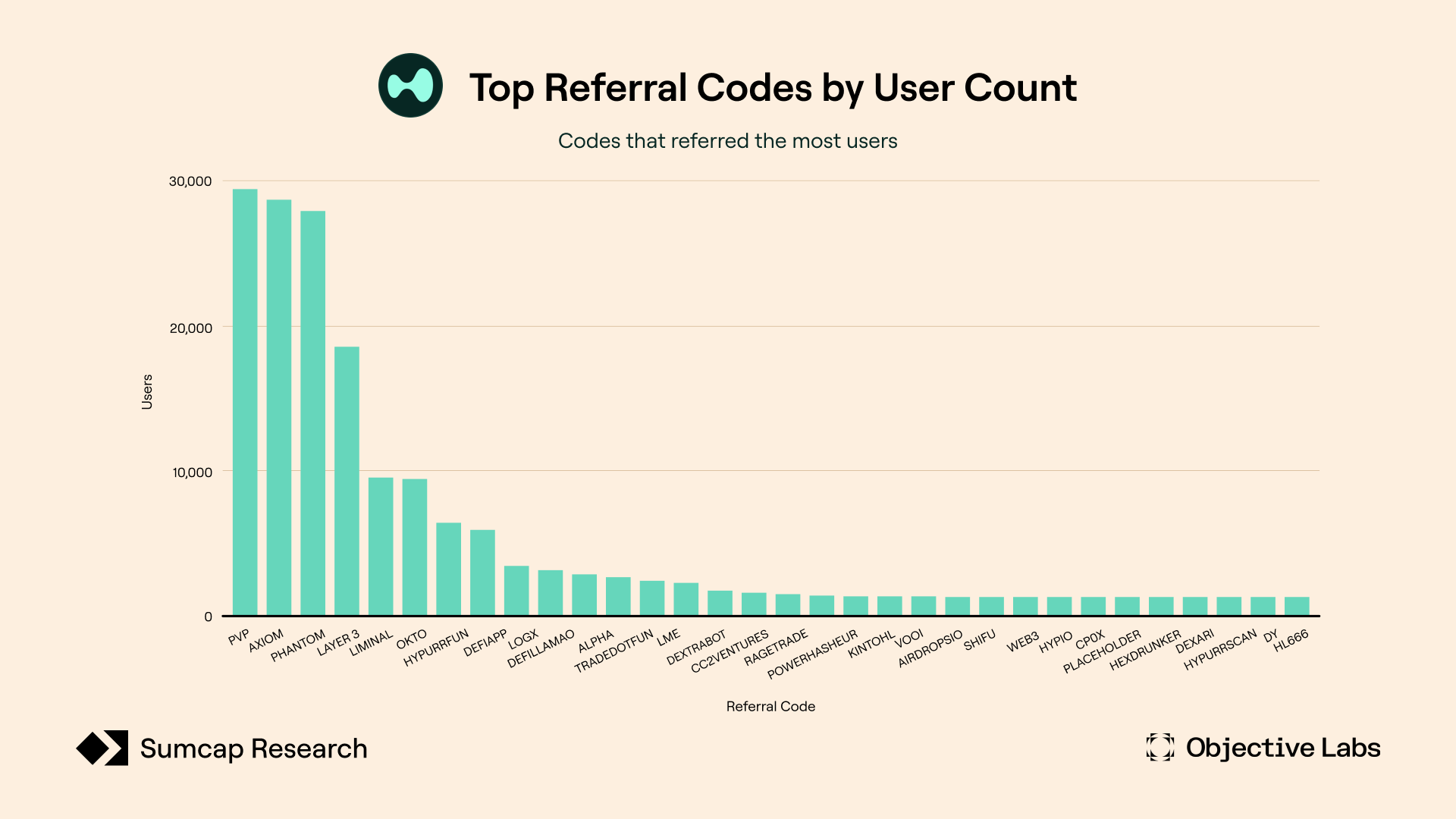

Part of this sustained momentum comes from having multiple acquisition channels feeding growth. Builder Codes have been a significant contributor, with more than 175 active builders, from wallets to trading bots to dApps, bringing in tens of thousands of traders. Three integrations alone have added between 25,000 and 30,000 users (PvP Trade, Axiom & Phantom Wallet), helping maintain a steady stream of new participants.

While some competitors see engagement peak during promotional cycles and taper off afterward, Hyperliquid’s pace has held steady across varying market conditions. Its mix of steady onboarding, active trading, and a committed user community has turned the momentum from late 2024 into a sustainable growth pattern through 2025.

Financial Metrics and Value Capture

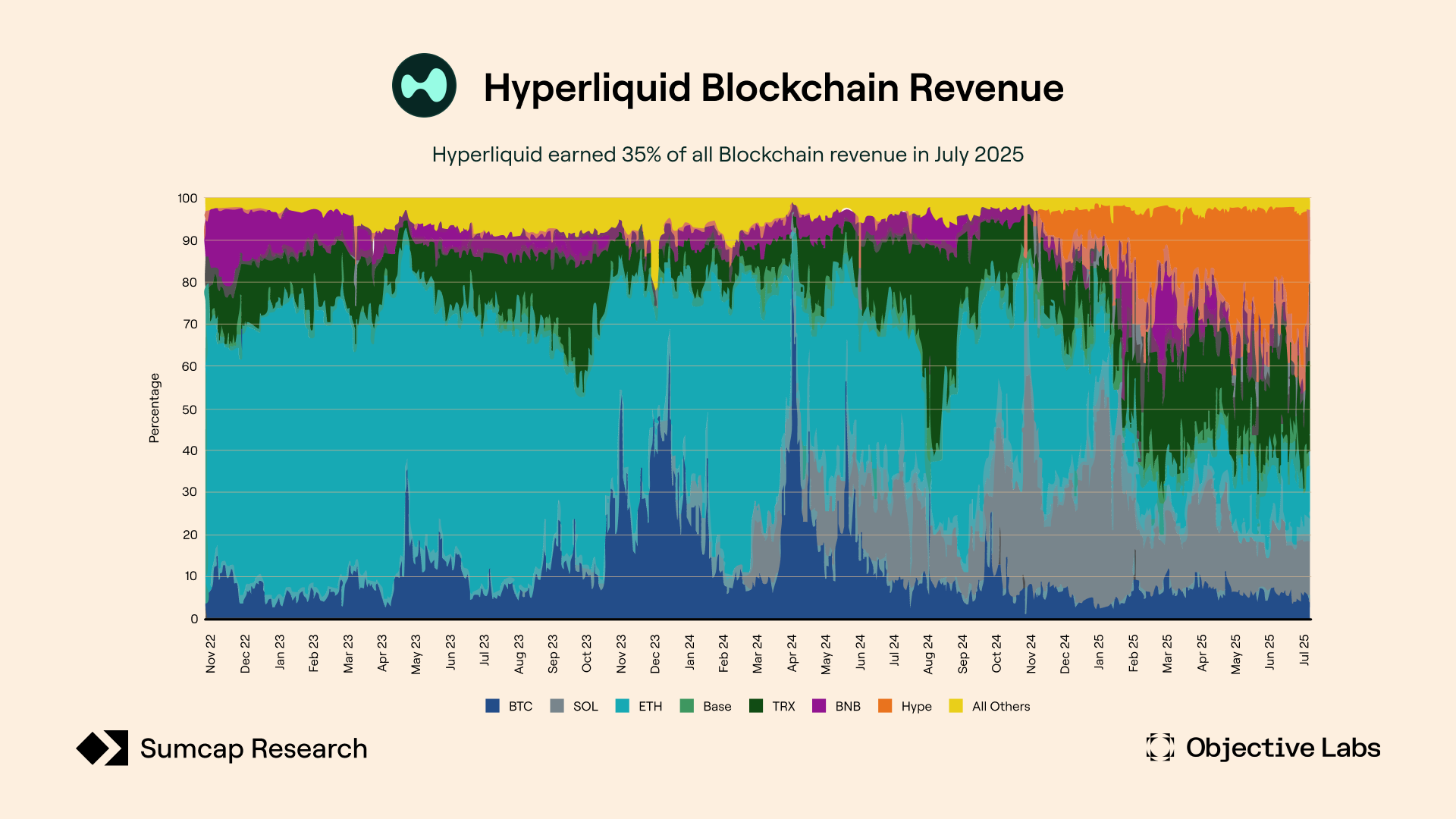

When it comes to generating and returning value to its community, Hyperliquid has become one of the most impressive stories in DeFi. Year-to-date, the platform has averaged $50 million in fee revenue per month with a projected annual run rate of $1.276 billion.

At the start of 2025, Hyperliquid was a small piece of the DeFi landscape, capturing just about 1.6% of total industry fees. But that picture has changed quickly. As the year has unfolded, Hyperliquid’s share of the overall market has grown steadily, now reaching around 4.6% of all DeFi monthly protocol fees.

.png)

Hyperliquid’s July revenue made up more than a third of all blockchain network revenue for that month. This is a record result putting Hyperliquid alongside major general-purpose smart contract blockchains, sparking conversations around traditional models of value capture in networks.

But here’s what makes it interesting: 100% of revenue flywheels back to users, creating long-term alignment between token holders and core contributors.

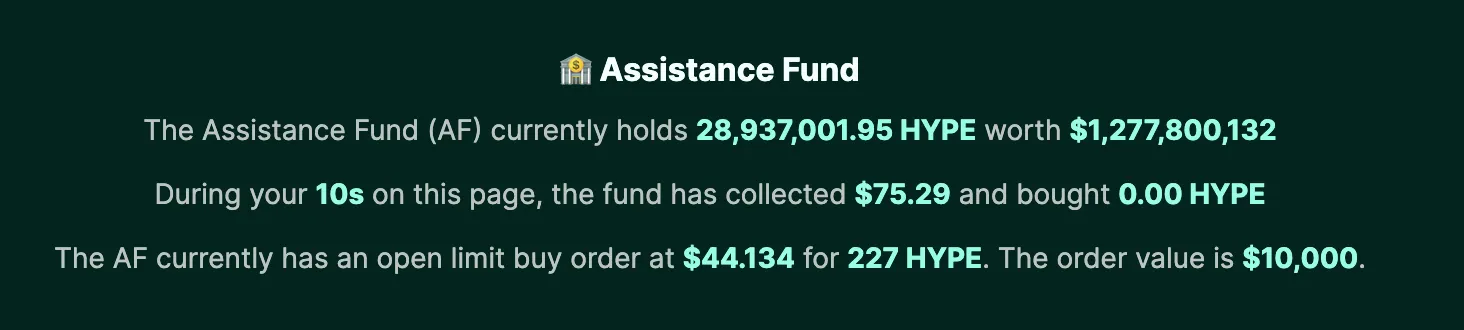

Nearly 93% of all fees stream into the Assistance Fund (AF) with one simple job: buy back $HYPE tokens from the open market. Since its inception, the AF has accumulated 28.93M $HYPE valued, at the time of writing, about $1.28B. The remainder ~7% goes to HLP depositors to incentivise market-making liquidity.

Instead of complex reward structures or splitting revenue across unrelated programs, Hyperliquid built a direct line from trading activity to token holder value. More trading means more buybacks, less circulating supply, and better alignment around long-term success.

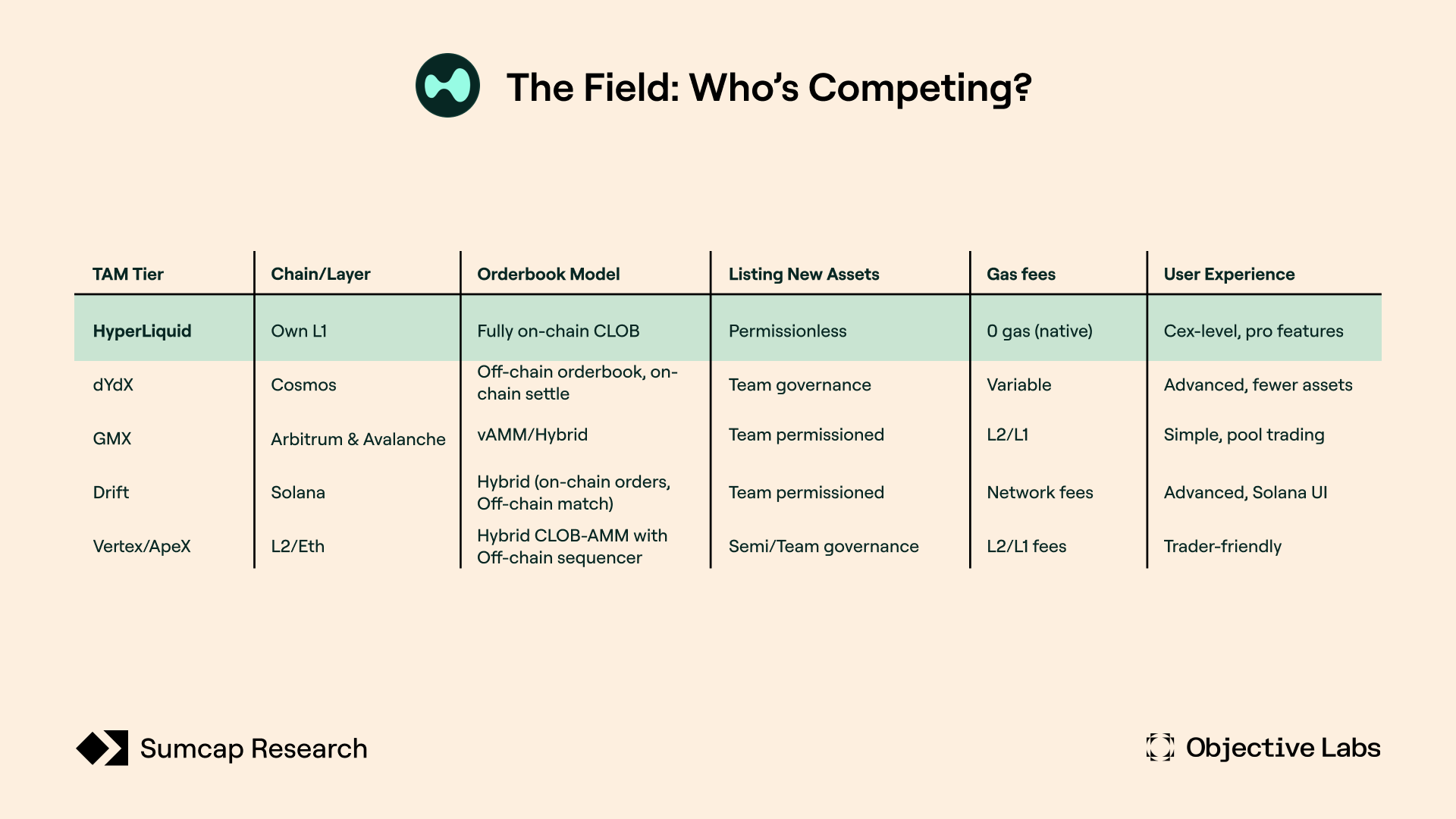

The Field: Who’s Competing?

To put things into perspective, here’s a quick snapshot of the main protocols in perpetual futures trading and the basics of how they operate:

In a crowded field of perpetual DEXs, Hyperliquid breaks away from the pack with a combination of speed, cost-efficiency, and openness that competitors can hardly match. Its edge comes down to three big reasons:

- Custom-built chain and fully on-chain order book: bring CEX-level speed and depth to DeFi, complete with advanced tools like TWAP and trailing stops - without the latency or MEV headaches that plague general-purpose chains.

- Gas-free trading: removing one of the biggest pain points for active and algorithmic traders and making high-frequency strategies far more practical.

- Permissionless listing framework: opening the door to new markets: HIP-1/2 (already live) lets anyone launch spot listings through Dutch auctions, while HIP-3 (coming soon) will do the same for perpetuals, with deployers providing market making and standardized liquidation logic ensuring safety.

Taken together, these features make Hyperliquid the most complete trading infrastructure in DeFi today, and explain its rapid rise to a leading position in the industry

Opportunity and TAM

The Growth Engines

Hyperliquid's strategic evolution will be fundamentally driven by a shift from a single-product exchange to a foundational financial infrastructure. This is made possible by the synergistic effect of its recent upgrades: 1) Builder Codes, 2) HIP-3, and 3) CoreWriter, which form a powerful, self-reinforcing flywheel that fundamentally expands its Total Addressable Market (TAM).

Builder Codes

The process begins with Builder Codes, which act as a decentralised distribution layer, onboarding new users through innovative and specialised front ends. This approach effectively outsources user acquisition to a distributed network of developers, a strategy that radically departs from traditional centralised models.

Current adoption metrics validate the program's effectiveness. As of July 2025, according to Hypeburn, there were 176 active builders, with a cumulative fee revenue of $10.8M. Early successes includes:

- Pvp Trade, a Telegram bot that has generated $7.2M.

- Okto, a mobile app with a total revenue of $690,000.

- Phantom, a major wallet, generated over $700,000 in just two weeks and has onboarded over 30K users.

This decentralised distribution funnel has demonstrated the model's potential to onboard large user bases efficiently and is contributing to the expansion of Hyperliquid’s market, positioning it to reach a much broader user base than would otherwise be possible.

HIP-3

The next growth engine, HIP-3, meets the rising demand from Hyperliquid’s expanding user base by empowering a permissionless network of “deployers” to create and monetise bespoke perpetual markets. Any qualified entity can now spin up markets directly on Hyperliquid’s Core infrastructure - marking a pivotal shift from Hyperliquid as a market operator to an infrastructure provider.

This transition has sparked what some are calling the “HIP-3 wars” - not a fight against rival platforms, but a high-stakes race among projects and institutional-grade dApps to become the dominant market providers within Hyperliquid itself. The stakes are high: deployers can earn up to 50% of trading fees from their markets, creating a powerful incentive for serious actors with the operational and financial scale to compete.

At the heart of this model is the 1 million HYPE staking requirement, which serves a dual purpose. It acts both as a security bond aligning deployer incentives with the protocol and as a significant demand sink for the HYPE token. Rather than a barrier, this high threshold is a strategic filter - designed to attract institutional-grade entities and foster the emergence of “staking collectives” or pseudo–on-chain BlackRocks capable of managing and launching markets at scale.

By opening up infrastructure access in this way, HIP-3 expands the total addressable market to include tokenised RWAs, equities, traditional indices, commodities, and FX - laying the foundation for a new era of on-chain financial primitives.

CoreWriter

The final component, CoreWriter, is the technical cornerstone that ensures the entire system functions as a cohesive, composable whole, so that this entire ecosystem of builders and deployers can natively and efficiently interact with HyperCore.

This seamless integration eliminates the security risks associated with cross-chain bridges and unlocks a new class of real-time financial applications. Early integrations already demonstrate the immense potential of CoreWriter.

Kinetiq, a liquid staking protocol that leverages the upgrade, attracted over $470 million in just two days after its launch, now having $1.3B in TVL. Other protocols are already exploring or implementing similar integrations, including lending protocols like HypurrFi, Hyperlend, and Felix, as well as yield protocols like Liminal.

The revenue from these integrations is not derived from simple trading fees but from fees associated with liquidations, lending, and automated trading strategies, which can transition capital from passive to active states. As of August 2025, Hyperliquid’s TVL is $634M, while the broader Hyperliquid L1 DeFi ecosystem TVL reaches $3.7B, based on data on DeFiLlama.

Sizing the Opportunity: Projecting a Multi-Trillion Dollar Market

Hyperliquid's total addressable market can be segmented and projected across three tiers, each building upon the platform's core strengths and new upgrades:

- Tier 1: Direct Perpetuals (Baseline TAM)

- The global perpetual trading market remains massive, historically dominated by CEXs.

- By mid-2025, Hyperliquid had already captured 6.3% of CEX perpetuals volume.

- With technical advantages and a loyal user base, Hyperliquid is positioned to keep gaining share.

- Conservative projection: 15% market share by end of 2026, representing trillions in annual volume.

- Tier 2: Builder-Driven Volume

- Builder Codes expand TAM by creating a decentralised, exponential user acquisition funnel.

- Early builders already show strong traction and revenue growth.

- As the network expands, Builder-driven flow is projected to match native frontend flow, similar to the shift from DEX frontends to aggregators in spot swaps.

- Tier 3: The “AWS of Liquidity”

- Long-term vision: evolve from DEX to foundational infrastructure layer for on-chain finance.

- Extends TAM beyond perpetuals into lending, liquid staking, structured products, and tokenised RWAs.

- HIP-3 and CoreWriter unlock this opportunity, positioning Hyperliquid as the financial operating system of on-chain finance.

Scenario-Level Analysis

Based on a scenario-level analysis, Hyperliquid's market trajectory can be viewed through three distinct lenses: conservative, base, and bull. Each scenario builds upon the platform's core strengths while accounting for different levels of adoption and the successful execution of its long-term strategy.

- 🚧 Conservative: Maintains leadership in decentralised perpetuals with steady but limited growth vs. CEXs.

- 📊 Base: Recognised as legitimate Tier 1 infrastructure, processing $3-6T annually and bridging traditional derivatives with DeFi.

- 🚀 Bull: Becomes dominant on-chain infrastructure, processing $8-12T annually and reshaping the CEX-DEX landscape.

- 📈 Realistic: Serves as essential institutional infrastructure, delivering CEX-quality execution and capturing $1.5-3T annually through differentiation.

Conclusion

Hyperliquid’s evolution from solving the on-chain perpetuals trilemma to building a comprehensive financial infrastructure marks a new era for blockchain markets. It has moved beyond simply being a top-tier perpetual DEX. By combining its HyperBFT consensus, the dual HyperCore and HyperEVM execution environment, and a suite of composable tools like Builder Codes, HIP-3, and CoreWriter, Hyperliquid has become an engine that allows anyone to launch, scale, and monetize markets of any kind.

These innovations are more than just new features; they redefine what’s possible for financial products and protocols. The platform provides a level playing field for builders and deployers with permissionless creation, native composability, deep liquidity, and an open revenue structure that gives participants a direct stake in its success. This open and programmable stack creates a self-reinforcing flywheel that drives growth, user acquisition, and value capture, connecting everyone in the ecosystem.

Hyperliquid is now poised to transition from a platform to a financial operating system. The protocol's proven increasing market share, rapid user adoption, expanding integrations, and significant fee revenue demonstrate the real-world impact of this vision. What started as a solution for perpetuals is now scaling into a multi-trillion dollar opportunity, encompassing direct trading, builder-driven innovation, and foundational liquidity infrastructure.

As legacy DeFi protocols give way to Hyperliquid's comprehensive stack, the very meaning of "on-chain finance" is changing. This innovation isn't just technical; it's also about architecture, social dynamics, and economics. Hyperliquid provides a stage where protocols, traders, and builders can create, compete, and collaborate natively and without compromise. It's not just building for the future of financial markets; it’s establishing the foundation on which that future will be built. The next chapter in DeFi belongs to those ready to build on this new stack.

The HyperLiquid Stack: BuilderCodes, CoreWriter, HIP-3, and Read Precompiles

On-chain perps always faced the same trilemma: UX, decentralisation, or sustainability. Hyperliquid cracked it with their L1, but that was just the start. Builder Codes, HIP-3, and CoreWriter now transform it from a DEX into a financial infra stack where anyone can launch markets without compromise.

This piece was made in collaboration with the Obejctive Labs team.

Sector Genesis: From CEX to DEX Perps

Definition:

- "Rolling" - Closing a position in a futures contract as it approaches expiration and simultaneously opening a new one in a later-dated contract (allowing continuous exposure without settlement).

- "Arbitrage" - Exploiting price differences between futures and spot markets (or between different exchanges) to make risk-free or low-risk profits, in turn keeping futures prices close to fair value.

In 1992, Nobel Prize-winning economist Robert Shiller, frustrated by the friction of rolling futures contracts to maintain continuous exposure, theorised the idea of Perpetual Futures Contracts.

Unlike normal futures contracts that: (a) expired quarterly, (b) required "rolling" to maintain positions, and (c) kept prices close to spot through arbitrage, Shiller's perpetuals would have no expiration date.

Instead, they would use a funding mechanism - periodic payments between long and short holders based on the contract's deviation from spot price - to keep prices anchored without settlement.

This way:

- Rolling overhead was eliminated - no more closing expiring positions and opening new ones;

- Basis risk was minimal - traders wouldn't lose money from unfavourable price differences between contract months during rolls.

However, traditional finance never adopted this model; The idea remained theoretical for decades as there wasn’t enough demand for such products.

Finally, in 2011, Alexey Bragin developed the first practical implementation of perpetual futures at ICBIT. Specifically designed for cryptocurrency trading, his "inverse perpetual" used Bitcoin as margin, solving licensing issues for crypto exchanges (all operations could be settled in crypto) while providing leverage and shorting capabilities.

Bragin’s product paved the way for even more developed, mainstream perpetual futures products. The first of which was BitMEX’s XBTUSD perpetual swap. Launched in 2016, after their traditional quarterly futures failed to gain traction, XBTUSD concentrated all liquidity into its contract, creating the deep, 24/7 market that crypto traders desperately needed.

The product became wildly successful, handling $757.6M worth of volume in the first year of its launch. This led BitMEX to launch the first perp product without BTC as the margin - XBTCUSDT.

In subsequent years, more notable names followed in BitMEX's steps:

- Bybit launched its BTCUSD inverse perpetual in March 2018, building its entire exchange around the perpetual futures model;

- OKX (formerly OKCoin) integrated its BTC/USD inverse perpetual in December 2018;

- While Binance Futures followed in September 2019, recording an impressive $5.6B in trading volume within its first month of their BTC/USDT perpetual contract launch.

Until recently, perpetual futures were only accessible through centralised venues. In order to have access to these features, users had to abandon the core ethos of blockchain: self-custody and decentralisation. They were forced to deposit assets with centralised middlemen, reintroducing the very custody risks and regulatory vulnerabilities that crypto was meant to eliminate.

It all changed however with dYdX’s V2 launch in April 2020. As the first major on-chain perpetuals exchange, dYdX’s CLOB model allowed users to access leveraged perpetual futures while maintaining full custody of their assets.

Although it did open the doors for a totally new sector, the protocol still had its limits. Namely, as it was launched on Ethereum Mainnet, high gas fees and throughput limitations made small trades uneconomical, leading to poor user experience during volatile periods.

To address these fundamental bottlenecks, dYdX V3 launched in August 2021, migrating to the StarkEx Layer 2 and achieving CEX-like performance by solving the gas and speed limitations of V2. However, this came at a significant cost: it introduced an off-chain orderbook and a sequencer with trust assumptions - a clear step backwards in terms of decentralisation compared to the previous version.

The coming period was marked by teams experimenting with all kinds of different architecture, mainly motivated by introducing novel functionality or improving UX & speed.

GMX (originally Gambit) was first, launching in September 2021 with a multi-asset liquidity pool (GLP) as the direct counterparty to all trades. The model’s simple UX and minimal fees came with a major trade-off: LPs carried the full PnL risk of traders, effectively betting against all users.

Two months later, in November 2021 Drift V1 launched on Solana, trying to bridge the gap between AMMs and orderbooks with their Dynamic AMM (DAMM). Their design pulled liquidity from an AMM while still benefiting from on-chain orderbook price discovery and reduced slippage.

Level Finance launched in January 2023, on the BNB chain, with a tranche-based liquidity model where LPs could choose specific risk tiers for more precise capital allocation. But, this added precision also meant more operational nuance for the team.

Finally, in April 2023, Vertex launched on Arbitrum with a hybrid AMM + orderbook model, offering cross-margining to combine deep liquidity with efficient trading UX. However, the dual model required careful coordination between both systems.

Despite steady innovation, no protocol had yet cracked the fundamental trilemma: delivering CEX-like performance without compromising on decentralisation or sustainability. Each new design pushed the frontier forward, but always at a cost - some traded decentralisation for speed, others achieved scale but broke their economic models. The trade-offs seemed unavoidable.

This climate perfectly set the stage for HyperLiquid.

Rather than building on top of existing infrastructure and accepting its limitations, HyperLiquid took a 180º approach, creating a purpose-built L1 chain optimized specifically for perpetual futures trading.

By controlling the entire stack (from consensus to execution), HyperLiquid eliminated the external dependencies that plagued all previous protocols.No more Ethereum gas fees, Solana outages, or L2 sequencer risks.

No more choosing between decentralisation and performance.

HyperLiquid's architecture brings what the space has been looking for since dYdX's first on-chain attempt: truly decentralised perps with sub-millisecond execution, 0 gas fees for tradingTXs, and an economic model that aligns all participants.

The Hyperliquid Stack

Hyperliquid is best explained as a high-performance technology stack for on-chain finance, built on three core pillars:

- HyperBFT Consensus: The heart of Hyperliquid and a breakthrough consensus algorithm that provides the low latency and high throughput that matches the performance of CEXs.

- Dual Execution Environment: HyperCore, a Layer 1 optimised for perpetual futures, and HyperEVM, a general-purpose EVM chain with full smart contract capabilities.

- Open Extensions: Hyperliquid opens its ecosystem to the world through extensions like Precompiles and CoreWriter, which merge smart contract DeFi with HyperCore, and Builder Codes and HIP-3, which invite externals to create their own markets and access liquidity.

These reinforce the core principles of DeFi: transparency, removing intermediaries and breaking down information silos, and they are all designed to generate revenue for $HYPE token holders.

HyperBFT: A Foundation for Speed and Security

Having originally launched with Tendermint, Hyperliquid has since transitioned to a fully custom consensus protocol called HyperBFT. HyperBFT is designed to maximize throughput and finality, enabling Hyperliquid’s fully on-chain order book to match (and in some cases exceed) the performance of centralised exchanges.

At its core, HyperBFT is a hybrid PoS-BFT algorithm inspired by the HotStuff protocol. It achieves a median block time of just 0.07s with end-to-end latency at 0.2s and a practical upper limit of 200,000 transactions per second. Block production is managed by a closed validator set (staking threshold: 10,000 HYPE), with leaders rotating each round to protect against downtime or malicious behavior. As a BFT-based system, HyperBFT guarantees immediate finality and eliminates chain re-orgs, giving traders confidence that transactions are immutable once confirmed.

That said, HyperBFT is not without tradeoffs. Its opinionated design strongly prioritises speed and scalability at the cost of broader decentralisation and validator diversity. In other words, it optimises for performance first, while making conscious compromises on the openness and security assumptions.

Dual Execution with HyperCore and HyperEVM

A big part of what makes Hyperliquid different is the way it splits execution into two layers that work hand in hand: HyperCore and HyperEVM. This structure lets the system deliver both the raw speed traders demand and the flexibility developers expect.

HyperCore is the Hyperliquid’s exchange engine, managing spot and perpetual order-books, liquidations, and margin trading directly at the protocol level. Thanks to HyperBFT’s exceptional speed and finality guarantees, HyperCore can handle hundreds of thousands of orders per second while giving users a seamless, exchange-like experience. Features like copy trading, market making vaults, and the clearinghouse are all native to this layer.

HyperEVM extends that foundation by adding a fully EVM-compatible smart contract environment, sharing consensus and state with HyperCore. That means developers can deploy familiar EVM contracts while also interacting directly with HyperCore’s financial primitives, pulling real-time prices or executing trades through built-in system contracts. This creates room for lending markets, structured products, or yield strategies that plug seamlessly into Hyperliquid’s liquidity and trading infrastructure.

This unified dual execution environment provides several strategic advantages that position Hyperliquid as a leader in DeFi innovation, including:

- Enhanced performance and efficiency through modular architecture that specialises each layer for specific function.

- Seamless interoperability through a unified state, allowing HyperEVM smart contracts to interact directly with HyperCore.

- Unified security with both layers secured by a shared validator set under HyperBFT consensus, reinforced by a transparent on-chain order book and oracle defenses.

A Unified Financial Stack

While we’ve outlined Hyperliquid’s architectural principles, architecture alone doesn’t create value - it’s what builders can do with it that matters. To enable this, Hyperliquid developed five core components: Builder Codes, Read Precompiles, CoreWriter, HIP-3, and the HLP Vault.

Together, these innovations form a unified financial stack where:

- Front-ends become revenue-sharing partners (Builder Codes)

- Native data access reduces external dependencies (Read Precompiles)

- Core actions are programmable (CoreWriter)

- Market creation becomes permissionless (HIP-3)

- Market-making is democratised (HLP)

De facto turning Hyperliquid’s infrastructure into a powerful economic engine for builders. The outcome? Opening the door to new business models, reducing time-to-market and lowering operational costs - all fully on-chain, while maintaining custody and performance intact.

Builder Codes: Democratising Liquidity

Historically, launching an exchange meant building a very heavy infrastructure from zero. Teams had to build matching engines, design custody models and navigate all sorts of extensive technical and regulatory barriers - each step adding costs, complexity and delay before the final product could go live.

Hyperliquid shifts this paradigm with Builder Codes, allowing any team to plug their front-end into Hyperliquid’s orderbook at no cost, letting builders earn revenue via a shared fee (Builder fee) when users trade through their interface. Developers are able to leverage Hyperliquid’s battle-tested core infrastructure granting new liquid venues faster and at a fraction of the cost. This creates a flywheel effect where:

More venues → More volume → Pulls in more liquidity → Reduces the slippage & attracts new traders → Even more volume → More revenue for builder codes → Attracts more builders

This flywheel could go a step further with the recently proposed Staking Referral Program.

When implemented, Builder Codes exchanges that stake $HYPE at a higher tier than their referred users could capture up to 100% of their fee differential - opening novel incentive dynamics between front-ends that might share this revenue with high-volume traders, permitting them a more cost-efficient trading and generating higher volumes for Hyperliquid.

That said, some critical voices argue that despite attracting additional volume, this could effectively result in net lower revenue for Hyperliquid, as a share of the revenue would be shared with front-ends. In any case, the proposal is still under research, so final implementation details are subject to changes.

Read Precompiles: A complement to Oracles

Oracles are a critical infrastructure component in the DeFi ecosystem - enabling access to external data and powering countless dApps. But as an external dependency, they come with tradeoffs: architectural complexity, high costs and additional trust assumptions.

In the Hyperliquid ecosystem, Read Precompiles function as the first bridge between HyperCore and HyperEVM. Rather than relying on third party oracles, they enable smart contracts direct read access to HyperCore native-protocol data.

A native dApp requiring position details, users equity, staking info or both spot/perps market prices can rely on HyperCore information directly, instantly and cost-free. For teams innovating on the Hyperliquid ecosystem, this helps reduce costs and operational overhead by removing unnecessary oracle calls, while simplifying system architecture.

Note: Read Precompiles are optimised for Hyperliquid native applications. For projects requiring non-native data (e.g. BTC price), traditional oracles may provide a more globally aggregated perspective.

CoreWriter: Elevating Trustless DeFi

Many applications in DeFi are neither decentralised nor permissionless. In many cases, operations still rely on multisigs and manual intervention, especially common in LST/LRT protocols or other liquid wrappers. These dependencies create friction, introduce trust assumptions, and limit the automation potential of on-chain systems.

Hyperliquid bridges this gap with CoreWriter, the natural evolution from read-only precompiles to bidirectional access. Whereas Read Precompiles only allowed contracts to pull data, CoreWriter enables smart contracts to also push instructions back into HyperCore.

With this feature, HyperEVM applications can interact with HyperCore, removing the operational barrier between the two environments. Some of the actions that can be performed with this feature are:

- Submitting orders to HyperCore;

- Transferring assets between accounts;

- Depositing into vaults;

- Staking user balances.

With all of this happening under custom on-chain logic, HyperEVM becomes HyperCore’s programmable layer.

This shift unlocks new design space for permissionless protocols, making it possible to build fully on-chain applications that interact with HyperCore without custodial intermediaries or manual intervention. It represents a fundamental step toward a more automated and trust-minimised DeFi, a topic explored in greater detail later in this article.

HIP-3: Permissionless market creation

Market creation has historically been a closed process, controlled by a few parties and shaped by their interests. This gatekeeping often made the launch of new markets slow, opaque, limited and often inaccessible to smaller teams.

HIP-3 proposes to change that, with the aim of democratising perpetual market creation. Under HIP-3, any user or project staking 1M $HYPE can deploy new markets directly into HyperCore.

Deployers become accountable for maintaining market health - keeping oracle feeds accurate and providing market-making to ensure smooth trading. Failure to meet these responsibilities could result in slashing of the 1M $HYPE stake, aligning incentives with users and the core protocol. In exchange, Hyperliquid shares its matching engine and up to 50% of the trading fees generated by the pair, incentivizing deployers to focus on high-demand and well-liquified markets.

This permissionless approach opens the door to a much wider space, enabling not just more crypto pairs, but also commodities, forex, ETFs, and alternative quote assets. It also widens the opportunity to entirely new business models such as borrowing $HYPE to bootstrap market deployment or decentralised HIP-3 market maintenance collectives.

By encouraging broader participation in $HYPE staking, HIP-3 not only diversifies available markets but also strengthens network security. Resulting in a more open, competitive, and innovative sector where market deployment and maintenance becomes an edge.

HLP: Permissionless and verifiable Market Making

Many DeFi projects face intense pressure to bootstrap liquidity through predatory market-making agreements, which often grant preferential terms to a single counterparty at the expense of the broader community.

HLP offers an alternative: a permissionless, community-driven and verifiable liquidity vault where anyone can deposit USDC to participate in market-making.

With this capital, the protocol provides liquidity serving as counterparty and executor, ensuring deep and fast execution. In return, the HLP captures exchange fees (maker/taker, liquidation penalties, and funding rate payments) and any profit from the spread or positions it absorbs, distributing it proportionately among the liquidity providers.

HLP allowed Hyperliquid to operate smoothly in its early stages, even before attracting external market makers. Over time, HLP has consistently delivered competitive returns to depositors while significantly improving the trading experience - lowering slippage, tightening spreads, and making liquidations more efficient.

Together, these components elevate Hyperliquid from a simple perps platform or conventional L1 into a full-fledged infrastructure layer - one that lets builders bypass typical liquidity and operational hurdles to focus on product differentiation, user experience, and target markets, without reinventing core primitives.

In the following sections, we’ll explore what this enables in practice: the products teams are already shipping using Hyperliquid’s stack

Competitive Landscape

Hyperliquid’s recent performance is remarkably strong when compared to its competitors - a success driven by key metrics across market share, user adoption, fees, revenue and number of perps listing.

Market Performance and Dominance

Hyperliquid has rapidly established itself as the dominant player in the on-chain perpetual futures market, commanding market share estimated between 50% and 65% in 2025.

Its growth trajectory has been remarkably steep, beginning in early and throughout 2023 when it started gaining significant traction in the decentralised derivatives space. A major catalyst for its rapid expansion was the Token Generation Event (TGE) held on November 29, 2024. Counter to the usual trend, trading volumes on Hyperliquid have surged dramatically after TGE, further accelerating market capture. By late 2024, Hyperliquid was already servicing more than half of the perp market, with current market share nearing 70%.

Hyperliquid has profoundly reshaped the decentralised perp landscape. It has practically erased market share of once-established protocols like dYdX and GMX (which are now widely recognized as legacy). The remaining market is scattered across recent entrants building within the new paradigm commanded by Hyperliquid. However, having built an enormous liquidity moat, Hyperliquid still lacks a natural predator.

Since launch it has grown the pie for on-chain perpetuals, rekindling hope for decentralised trading as a viable alternative to established centralised venues. While previously the entire sector serviced $10-20B in weekly volume, >$100B weeks are not uncommon nowadays.

As the top dog in the DEX space, Hyperliquid has built a deep liquidity moat and a cult-like following, enough to now credibly compete with centralised giants like Binance, processing 12% of its volume in July 2025.

The broader DEX to CEX futures trade volume ratio has seen a marked increase in tandem with Hyperliquid’s rise. For most of 2022 and 2023, decentralised exchanges represented only around 1-3% of total futures trade volume relative to CEXes, now surpassing 10% in mid-2025. This shift evidences that Hyperliquid is not only dominating decentralised perpetual futures but is also significantly contributing to the overall migration of perp traders on-chain.

User Adoption and Platform Engagement

In 2025, Hyperliquid continued to expand its footprint in decentralised perps, combining rapid new user growth with sustained, high-volume engagement. It’s a rare case where a token launch didn’t just reward early users - it supercharged momentum, turning well-compensated traders into vocal evangelists. The days following the TGE were electric: over 11,000 new accounts were created within 48 hours, and daily active users have continued to hit new highs week after week.

Today, the platform onboards an average of 1.7k new traders every day with DAU rising from around 10k pre-TGE to over 50k in the past month. It’s not only more people in the door but more and more traders are sticking around and trading regularly. Hyperliquid’s user numbers are even more in comparison with competitors such as Jupiter with around 400 daily new users and nearly 6k in DAU, and edgeX at fewer than 100 daily new users.

Part of this sustained momentum comes from having multiple acquisition channels feeding growth. Builder Codes have been a significant contributor, with more than 175 active builders, from wallets to trading bots to dApps, bringing in tens of thousands of traders. Three integrations alone have added between 25,000 and 30,000 users (PvP Trade, Axiom & Phantom Wallet), helping maintain a steady stream of new participants.

While some competitors see engagement peak during promotional cycles and taper off afterward, Hyperliquid’s pace has held steady across varying market conditions. Its mix of steady onboarding, active trading, and a committed user community has turned the momentum from late 2024 into a sustainable growth pattern through 2025.

Financial Metrics and Value Capture

When it comes to generating and returning value to its community, Hyperliquid has become one of the most impressive stories in DeFi. Year-to-date, the platform has averaged $50 million in fee revenue per month with a projected annual run rate of $1.276 billion.

At the start of 2025, Hyperliquid was a small piece of the DeFi landscape, capturing just about 1.6% of total industry fees. But that picture has changed quickly. As the year has unfolded, Hyperliquid’s share of the overall market has grown steadily, now reaching around 4.6% of all DeFi monthly protocol fees.

Hyperliquid’s July revenue made up more than a third of all blockchain network revenue for that month. This is a record result putting Hyperliquid alongside major general-purpose smart contract blockchains, sparking conversations around traditional models of value capture in networks.

But here’s what makes it interesting: 100% of revenue flywheels back to users, creating long-term alignment between token holders and core contributors.

Nearly 93% of all fees stream into the Assistance Fund (AF) with one simple job: buy back $HYPE tokens from the open market. Since its inception, the AF has accumulated 28.93M $HYPE valued, at the time of writing, about $1.28B. The remainder ~7% goes to HLP depositors to incentivise market-making liquidity.

Instead of complex reward structures or splitting revenue across unrelated programs, Hyperliquid built a direct line from trading activity to token holder value. More trading means more buybacks, less circulating supply, and better alignment around long-term success.

The Field: Who’s Competing?

To put things into perspective, here’s a quick snapshot of the main protocols in perpetual futures trading and the basics of how they operate:

In a crowded field of perpetual DEXs, Hyperliquid breaks away from the pack with a combination of speed, cost-efficiency, and openness that competitors can hardly match. Its edge comes down to three big reasons:

- Custom-built chain and fully on-chain order book: bring CEX-level speed and depth to DeFi, complete with advanced tools like TWAP and trailing stops - without the latency or MEV headaches that plague general-purpose chains.

- Gas-free trading: removing one of the biggest pain points for active and algorithmic traders and making high-frequency strategies far more practical.

- Permissionless listing framework: opening the door to new markets: HIP-1/2 (already live) lets anyone launch spot listings through Dutch auctions, while HIP-3 (coming soon) will do the same for perpetuals, with deployers providing market making and standardized liquidation logic ensuring safety.

Taken together, these features make Hyperliquid the most complete trading infrastructure in DeFi today, and explain its rapid rise to a leading position in the industry

Opportunity and TAM

The Growth Engines

Hyperliquid's strategic evolution will be fundamentally driven by a shift from a single-product exchange to a foundational financial infrastructure. This is made possible by the synergistic effect of its recent upgrades: 1) Builder Codes, 2) HIP-3, and 3) CoreWriter, which form a powerful, self-reinforcing flywheel that fundamentally expands its Total Addressable Market (TAM).

Builder Codes

The process begins with Builder Codes, which act as a decentralised distribution layer, onboarding new users through innovative and specialised front ends. This approach effectively outsources user acquisition to a distributed network of developers, a strategy that radically departs from traditional centralised models.

Current adoption metrics validate the program's effectiveness. As of July 2025, according to Hypeburn, there were 176 active builders, with a cumulative fee revenue of $10.8M. Early successes includes:

- Pvp Trade, a Telegram bot that has generated $7.2M.

- Okto, a mobile app with a total revenue of $690,000.

- Phantom, a major wallet, generated over $700,000 in just two weeks and has onboarded over 30K users.

This decentralised distribution funnel has demonstrated the model's potential to onboard large user bases efficiently and is contributing to the expansion of Hyperliquid’s market, positioning it to reach a much broader user base than would otherwise be possible.

HIP-3

The next growth engine, HIP-3, meets the rising demand from Hyperliquid’s expanding user base by empowering a permissionless network of “deployers” to create and monetise bespoke perpetual markets. Any qualified entity can now spin up markets directly on Hyperliquid’s Core infrastructure - marking a pivotal shift from Hyperliquid as a market operator to an infrastructure provider.

This transition has sparked what some are calling the “HIP-3 wars” - not a fight against rival platforms, but a high-stakes race among projects and institutional-grade dApps to become the dominant market providers within Hyperliquid itself. The stakes are high: deployers can earn up to 50% of trading fees from their markets, creating a powerful incentive for serious actors with the operational and financial scale to compete.

At the heart of this model is the 1 million HYPE staking requirement, which serves a dual purpose. It acts both as a security bond aligning deployer incentives with the protocol and as a significant demand sink for the HYPE token. Rather than a barrier, this high threshold is a strategic filter - designed to attract institutional-grade entities and foster the emergence of “staking collectives” or pseudo–on-chain BlackRocks capable of managing and launching markets at scale.

By opening up infrastructure access in this way, HIP-3 expands the total addressable market to include tokenised RWAs, equities, traditional indices, commodities, and FX - laying the foundation for a new era of on-chain financial primitives.

CoreWriter

The final component, CoreWriter, is the technical cornerstone that ensures the entire system functions as a cohesive, composable whole, so that this entire ecosystem of builders and deployers can natively and efficiently interact with HyperCore.

This seamless integration eliminates the security risks associated with cross-chain bridges and unlocks a new class of real-time financial applications. Early integrations already demonstrate the immense potential of CoreWriter.

Kinetiq, a liquid staking protocol that leverages the upgrade, attracted over $470 million in just two days after its launch, now having $1.3B in TVL. Other protocols are already exploring or implementing similar integrations, including lending protocols like HypurrFi, Hyperlend, and Felix, as well as yield protocols like Liminal.

The revenue from these integrations is not derived from simple trading fees but from fees associated with liquidations, lending, and automated trading strategies, which can transition capital from passive to active states. As of August 2025, Hyperliquid’s TVL is $634M, while the broader Hyperliquid L1 DeFi ecosystem TVL reaches $3.7B, based on data on DeFiLlama.

Sizing the Opportunity: Projecting a Multi-Trillion Dollar Market

Hyperliquid's total addressable market can be segmented and projected across three tiers, each building upon the platform's core strengths and new upgrades:

- Tier 1: Direct Perpetuals (Baseline TAM)

- The global perpetual trading market remains massive, historically dominated by CEXs.

- By mid-2025, Hyperliquid had already captured 6.3% of CEX perpetuals volume.

- With technical advantages and a loyal user base, Hyperliquid is positioned to keep gaining share.

- Conservative projection: 15% market share by end of 2026, representing trillions in annual volume.

- Tier 2: Builder-Driven Volume

- Builder Codes expand TAM by creating a decentralised, exponential user acquisition funnel.

- Early builders already show strong traction and revenue growth.

- As the network expands, Builder-driven flow is projected to match native frontend flow, similar to the shift from DEX frontends to aggregators in spot swaps.

- Tier 3: The “AWS of Liquidity”

- Long-term vision: evolve from DEX to foundational infrastructure layer for on-chain finance.

- Extends TAM beyond perpetuals into lending, liquid staking, structured products, and tokenised RWAs.

- HIP-3 and CoreWriter unlock this opportunity, positioning Hyperliquid as the financial operating system of on-chain finance.

Scenario-Level Analysis

Based on a scenario-level analysis, Hyperliquid's market trajectory can be viewed through three distinct lenses: conservative, base, and bull. Each scenario builds upon the platform's core strengths while accounting for different levels of adoption and the successful execution of its long-term strategy.

- 🚧 Conservative: Maintains leadership in decentralised perpetuals with steady but limited growth vs. CEXs.

- 📊 Base: Recognised as legitimate Tier 1 infrastructure, processing $3-6T annually and bridging traditional derivatives with DeFi.

- 🚀 Bull: Becomes dominant on-chain infrastructure, processing $8-12T annually and reshaping the CEX-DEX landscape.

- 📈 Realistic: Serves as essential institutional infrastructure, delivering CEX-quality execution and capturing $1.5-3T annually through differentiation.

Conclusion

Hyperliquid’s evolution from solving the on-chain perpetuals trilemma to building a comprehensive financial infrastructure marks a new era for blockchain markets. It has moved beyond simply being a top-tier perpetual DEX. By combining its HyperBFT consensus, the dual HyperCore and HyperEVM execution environment, and a suite of composable tools like Builder Codes, HIP-3, and CoreWriter, Hyperliquid has become an engine that allows anyone to launch, scale, and monetize markets of any kind.

These innovations are more than just new features; they redefine what’s possible for financial products and protocols. The platform provides a level playing field for builders and deployers with permissionless creation, native composability, deep liquidity, and an open revenue structure that gives participants a direct stake in its success. This open and programmable stack creates a self-reinforcing flywheel that drives growth, user acquisition, and value capture, connecting everyone in the ecosystem.

Hyperliquid is now poised to transition from a platform to a financial operating system. The protocol's proven increasing market share, rapid user adoption, expanding integrations, and significant fee revenue demonstrate the real-world impact of this vision. What started as a solution for perpetuals is now scaling into a multi-trillion dollar opportunity, encompassing direct trading, builder-driven innovation, and foundational liquidity infrastructure.

As legacy DeFi protocols give way to Hyperliquid's comprehensive stack, the very meaning of "on-chain finance" is changing. This innovation isn't just technical; it's also about architecture, social dynamics, and economics. Hyperliquid provides a stage where protocols, traders, and builders can create, compete, and collaborate natively and without compromise. It's not just building for the future of financial markets; it’s establishing the foundation on which that future will be built. The next chapter in DeFi belongs to those ready to build on this new stack.

.svg)