OlympusDAO: An Onchain Monetary System

Most DeFi projects barely think about what should give their token real value. Supply mechanics get locked in before the token even hits the market, with emissions and burns following a fixed timeline instead of adapting to market conditions. OlympusDAO, exact opposite of this.

Olympus DAO built an on-chain monetary system very similar to a central bank that manages a treasury with the aim to accrue value and utility to $OHM.

The treasury holds a diversified reserve base, namely $USDS and $sUSDe alongside other high-quality and is operated through dedicated treasury and policy wallets with scoped mandates. These wallets execute reserve management, deploy capital, service credit, and route generated yield back into policy mechanisms.

Olympus Architecture

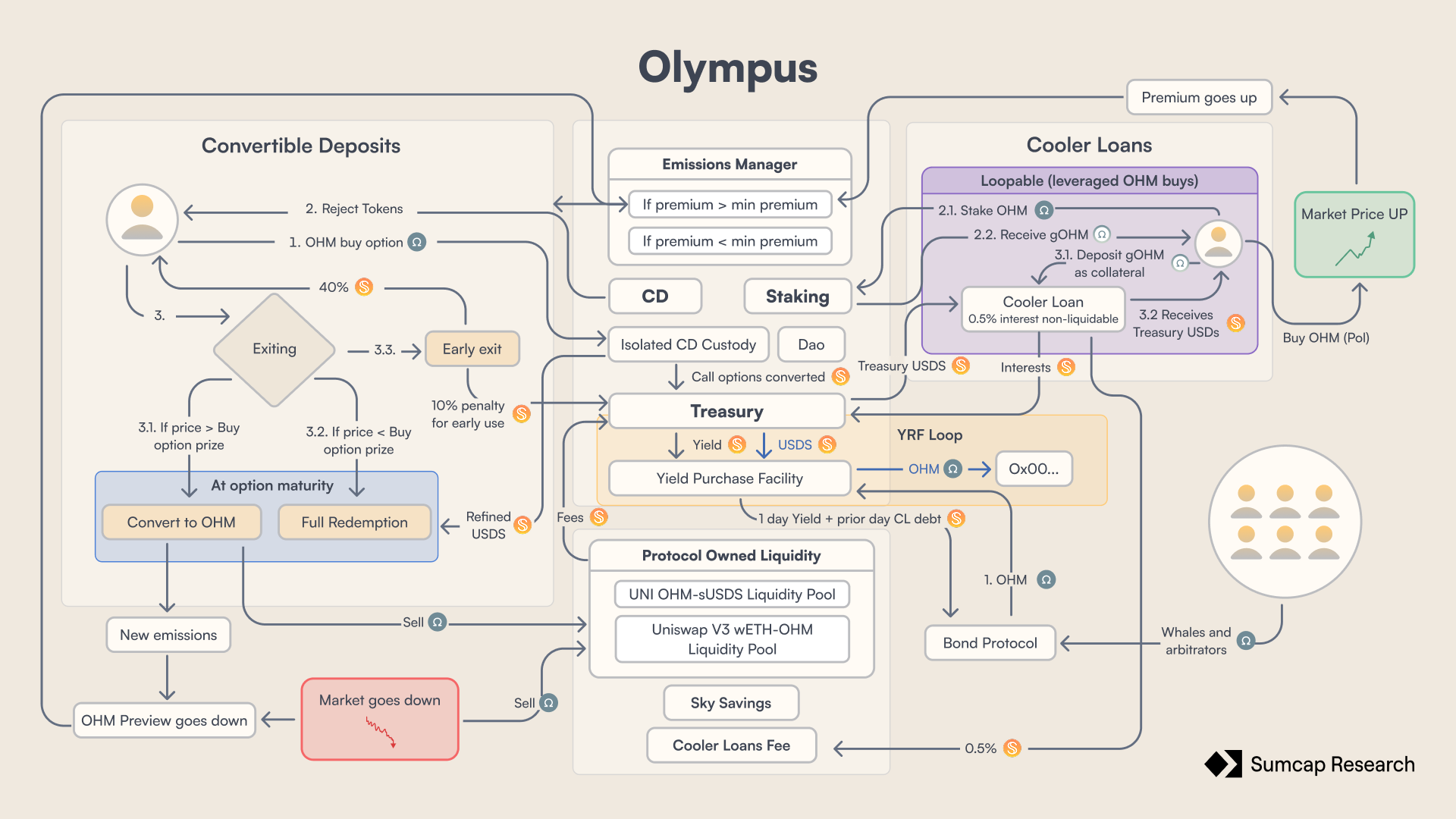

The treasury is the cornerstone of Olympus. It holds reserves and deploys them across three active mechanisms.

- Cooler Loans, a native credit facility;

- Yield Repurchase Facility (YRF), an automated buyback-and-burn engine;

- Convertible Deposits, demand-responsive $OHM issuance.

Each mechanism is designed to convert treasury activity into token holder value through a different channel.

This report explains Olympus through its core mechanisms, then connects them into a single system view focusing on second-order implications.

Active Mechanisms

Cooler Loans

Cooler Loans let users borrow $USDS directly from the Olympus Treasury by using $gOHM as collateral. Those Loans pay a fixed 0.5% APR (set by governance) and have no price-based liquidations, as they use the OLTV as reference price. Loans only default if unpaid interest accumulates past a governance-defined threshold.

The OLTV capacity expands over time via a LTV drip (governance-set), which gradually increases the borrowing capacity toward a target on a schedule, instead of relying on market price or external oracle feeds for liquidation logic. This is a deliberately slow, governance-controlled expansion rather than a market-reactive.

The Initial OLTV ratio (as of May 15, 2025) was ~11 USDS/OHM (2961.64 USDS/gOHM) with a target of 11.11 USDS/OHM, this was achieved on March 6th 2026.

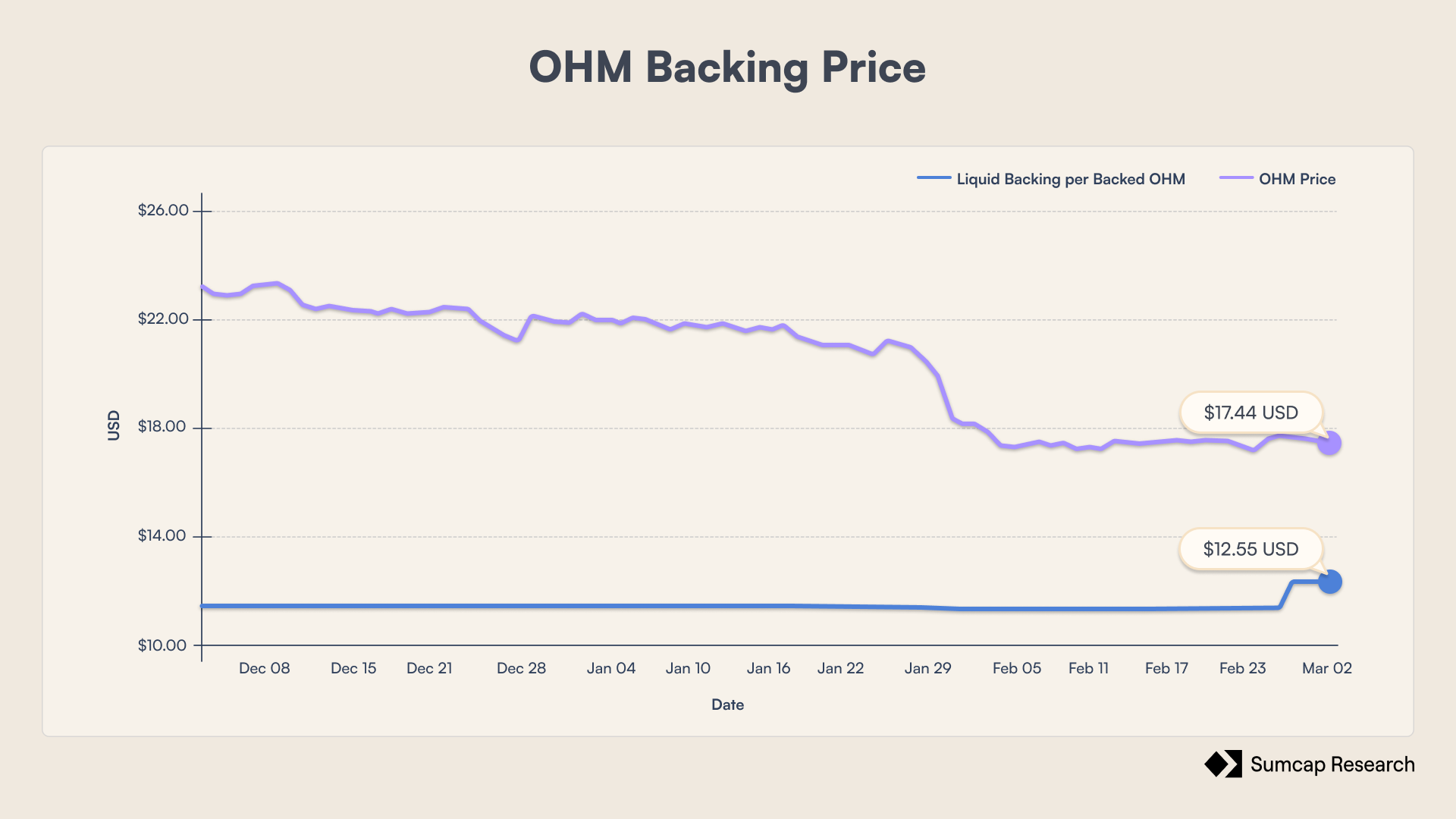

The liquid backing per $OHM price is the dollar amount of stablecoins, volatile assets and protocol-owned liquidity in the treasury, excluding $OHM. It serves as the fundamental solvency guarantee, as the OLTV is always set at a safe discount relative to the actual backing, ensuring the protocol remains solvent even if borrowers default.

The recent rise of the backing price is due to the fact that Olympus has started to burn the gOHM that where in the TokenMigrator contract as they are starting to deprecate it.

The primary use case of Cooler Loans is enabling capital-efficient leveraged $OHM exposure. At 0.5% APR with no liquidation risk from price volatility, Cooler Loans become the cheapest leverage in DeFi for $OHM. Borrowers can loop by borrowing $USDS, acquiring more OHM/gOHM, and adding collateral, creating leverage without liquidation cascades from market volatility (though default risk still exists if interest is not serviced). Also, as the borrow APY is so low, it's extremely useful to do a carry trade with this unlocked capital.

How do Cooler Loans generate value for $OHM?

First, interest paid on Cooler debt accrues directly to the Olympus treasury that feeds back into buyback capacity via the Yield Repurchasing Facility (YRF). Second, in case of default, the position is closed and the $gOHM collateral is burned. This reduces circulating gOHM/OHM claims while the previously borrowed $USDS automatically returns to the Treasury. Defaults are supply-supportive as borrowers lose collateral, but remaining holders get a more concentrated claim on reserves.

The trade-off is that Cooler Loans force a choice between growth and treasury optimisation. Lending $USDS at 0.5% lowers the treasury’s aggregate yield compared with allocating that same $USDS into higher yielding reserve strategies (for example, $USDS savings at around 4.5% APY). The effective cost of Cooler shifts with prevailing stablecoin yield.

Yield Repurchase Facility (YRF)

The Yield Repurchase Facility (YRF) is the automated buyback-and-burn engine.

The YRF increases its purchasing power by recycling backing, it buys $OHM (via Bond Protocol), then burns that $OHM and withdraws $USDS reserves from the Treasury at the max OLTV. This reduces $OHM supply and converts purchased $OHM into additional $USDS budget for future buybacks.

The architecture that the YRF uses to increase its purchasing power is essentially the same as the one used for Cooler Loans.

Mechanism & Cadence

The YRF is a smart contract that runs on Heart beats (every 8 hours). Its flows are split into two timescales: a weekly accounting step and daily execution.

Once per week, the system calculates the prior week’s yield earned from two sources:

- reserves deposited in the $USDS savings vault (~3.75% APY in SSR)

- interest earned from Cooler Loans (the 0.5% APY borrow rate).

Then, the contract pulls previous week’s computed yield from the Treasury in $SUSDS. Every day, a four-step execution loop runs.

- The YRF tracks $OHM captured from the prior day’s purchases (this $OHM sits in the YRF contract).

- Burn $OHM and, in exchange, withdraws reserves from the Treasury equal to a preconfigured backing value per $OHM.

- Unwraps one day’s worth of $USDS from its $SUSDS holdings for today’s buyback.

- Opens a 1-day Bond Protocol market to buy $OHM using

- today’s $USDS yield allocation

- the recycled $USDS backing obtained from the burn step.

Performance & Efficiency

So far, OlympusDAO has bought more than 11M $OHM through all its different mechanisms, including Inverse Bonds, the RBS lower cushion, YRF, and TWAP execution. These are gross purchases so they do not net out any $OHM that may have been sold elsewhere.

Within that total, YRF alone has bought and burned roughly 650k $OHM at an average price of $20.42 per $OHM.

Execution is not perfectly efficient as YRF routes purchases through Bond Protocol instead of sourcing directly from open markets, where arbitrage bots capture part (or most) of the spread. On a weighted basis, YRF has paid about 0.6% above the market price, and nearly half of Bond Protocol counterparties are bots, which suggests there is consistent extractable profit between the two venues.

Even with this leakage, the system still delivers what it is designed for. It creates persistent, buy flow and compresses supply through burns, which lowers circulating $OHM and reduces selling pressure from large holders.

Convertible Deposits & the Emissions Manager

When the premium (market value / backing value) exceeds a governance-set minimum premium (currently 100%, meaning $OHM trades at 2x or more of backing), the Emissions Manager activates a Convertible Deposits auction, offering a computed amount of newly issued $OHM in exchange for fresh $USDS reserves.

If the premium target has not been reached, the auction is disabled.

The equation for this emission is:

\[\ \text{NewSupply} = \text{TotalSupply} \times \text{BaseEmissionsRate} \times \frac{\left(\text{Premium} + 100\%\right)}{\left(\text{MinPremium} + 100\%\right)}\ \]

Where:

- Base emissions rate -> the base percentage of circulating supply to be sold per day (at minimum premium), currently 0.02% per day.

- Emissions rate = Base Rate × (1 + premium) / (1 + min premium)

- Minimum premium rate -> the threshold premium required for emissions to be active (set by governance)

- Premium = market price / backing price

The higher the premium, the greater the emission rate will be, effectively creating more sell pressure when the market overbuys $OHM.

At current settings, Convertible Deposits only turn on when $OHM trades at least 2.0× backing ( minPremium = 100%). In this case, Olympus prefers to monetise demand by selling newly issued $OHM (locked) for fresh reserves ($USDS) to grow the treasury, rather than letting premiums run.

Once active, governance has two main levers that control how aggressive this reflex becomes:

- minPremium (activation threshold): Higher values make emissions rarer but more “event-driven.” Lower values make emissions more frequent and start clipping premium earlier.

- baseRate (slope/throughput): Sets the baseline fraction of supply the system is willing to sell per day at exactly minPremium (currently at 0,02%/day), and scales linearly with premium. Increasing baseRate makes the system respond faster, but also increases the risk of overshooting and pushing premium down too hard.

This creates a negative feedback loop. Premium expands, emissions scale up, supply is sold into demand for $USDS, and the premium is pulled back toward the activation boundary. When premium cools below the threshold, emissions shut off. Convertible Deposits are a way to convert moments of demand into reserves, while using the auction format to push as much of the ‘premium monetisation’ as possible onto takers.

Auction Mechanics

The auction uses a tick-based system for dynamic price discovery.

- The system determines how many deposit tokens are needed to fill the remaining capacity of the current tick.

- If the bid exceeds this amount, it fills the current tick completely and moves to the next higher-priced tick.

- This continues across multiple ticks until the entire bid is processed.

If there are large bids spanning multiple ticks drive prices up faster, and insufficient demand causes tick prices to decay over time (with a floor set by auction parameters).

In case that $OHM is under-sold during the auction, a Bond Protocol market is created as a fallback to sell the remainder.

Convertible Deposits as a User

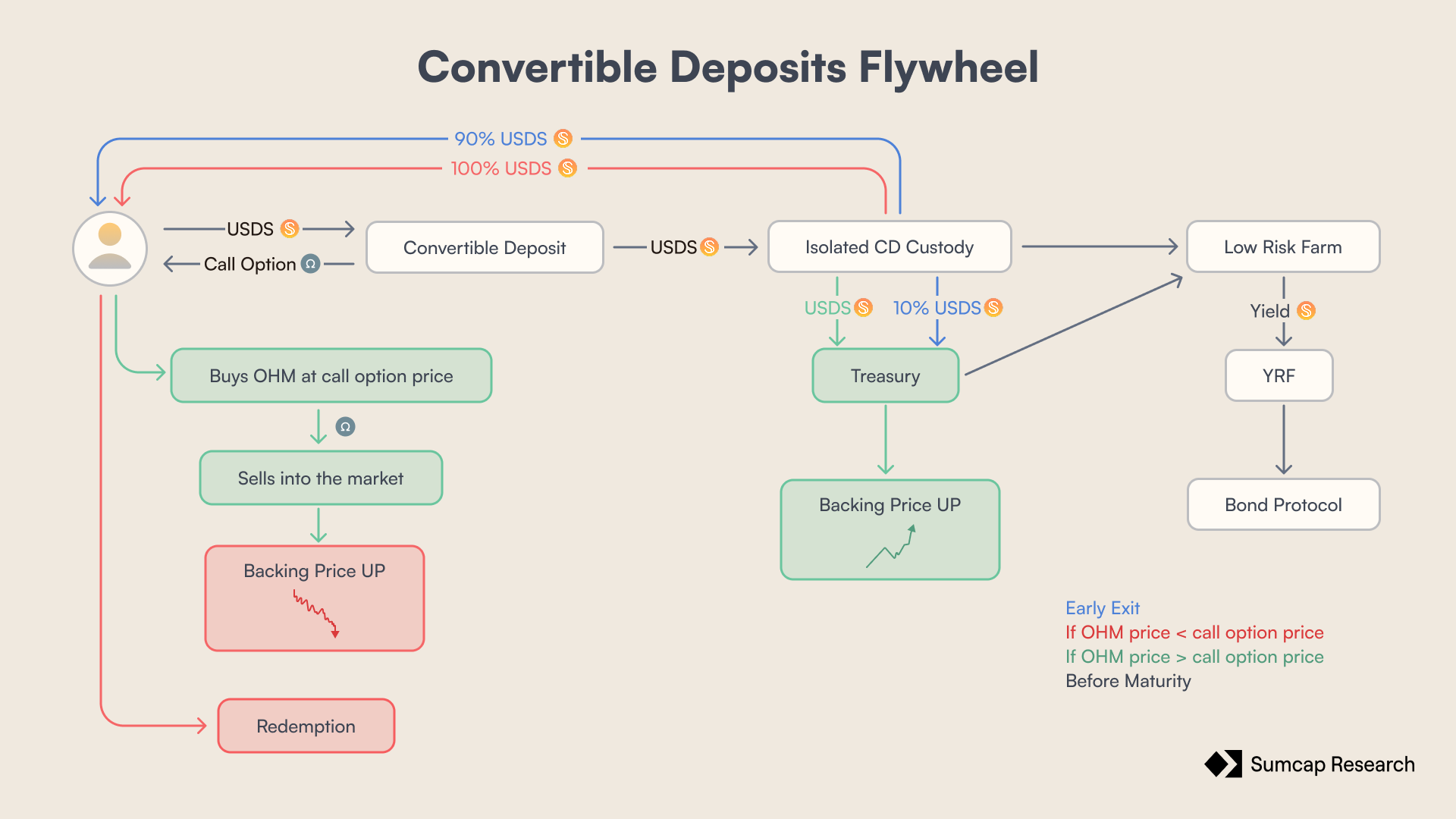

Users deposit $USDS and receive receipt tokens plus a non-fungible position that locks in a specific conversion price for $OHM (below current market).

Once the maturity day arrives, the user that has bought a CD has two choices:

- Execute the call option and get the $OHM, increasing the backing

- Redeem the $USDS deposited (This only makes sense if the market price < option)

If a user decides to redeem the $USDS before the maturity date, Olympus would take a 10% penalty fee that would be redirected to the treasury, increasing $OHM backing and reducing the premium.

While the position is open, the protocol deploys the deposited $USDS to earn yield until maturity, and that yield feeds into YRF buybacks. This makes the structure accretive across outcomes.

System Overview: How the Mechanisms Connect

All of these mechanisms affect $OHM supply, so the easiest way to see how they connect is to walk through a concrete scenario.

Imagine a user wants $OHM exposure. A capital efficient way to get it is to buy $OHM on the open market and then use a Cooler Loan, since the carry cost is close to zero. As the user buys, their order flow pushes price up, which also increases the $OHM premium.

At that point Olympus has already captured value. A large share of onchain liquidity is controlled by the protocol, so it earns swap fees on that flow. Olympus also earns the 0.5% APY on the borrowed $USDS, which increases the treasury over time.

Now the premium sits above the minimum threshold, so the Emissions Manager enables Convertible Deposits to stop price from drifting too far above backing. In practice, the protocol opens a bond style sale where users deposit $USDS in exchange for a position that can be converted into $OHM at a discounted conversion price.

After the sale, participant $USDS is moved into separate custody and deployed to farm yield until maturity. When maturity arrives, users choose whether to exercise. If they exercise, their $USDS moves to the treasury and continues earning yield while they receive $OHM. If they do not exercise, Olympus returns 100% of the deposited $USDS and keeps the yield earned during the term. If someone exits early, Olympus keeps 10% of the principal as a fee.

If enough users exercise, the additional $OHM supply creates near term sell pressure that tends to compress the premium. Once the premium falls back under the threshold, Convertible Deposits switch off.

All yield collected across the system feeds into YRF. That includes interest from Cooler Loans, fees from protocol owned liquidity, and the yield generated on Convertible Deposit USDS. YRF then uses this yield to buy $OHM.

Once per week, the YRF calculates last week’s yield earned, then pulls that amount from the Treasury as $SUSDS to fund the next week’s operations, and then every day it:

- Looks at the $OHM it bought the prior day;

- Borrows $USDS against that $OHM at a preset backing value, and burns the $OHM;

- Unwraps one day’s worth of $USDS out of $SUSDS for spending;

- Opens a 1-day Bond Protocol market that uses (today’s yield $USDS + the borrowed $USDS) to buy $OHM over that day.

YRF helps the price of $OHM by acting as a marginal buyer and burning supply. Additionally, as YRF buys $OHM that gets arbed in the open market, the premium (with no uptick in demand) becomes higher, and the loop may start again.

What's to Come

Burner Loans

At present, bearish positioning must occur externally, either through spot selling or derivatives markets. That activity does not directly benefit the protocol, that's what Burner Loans aim to internalize.

Where Cooler Loans allow users to borrow stables against $gOHM collateral and take leveraged long exposure, Burner Loans would allow users to borrow $OHM against $SUSD collateral and take short exposure.

Outcomes

Short fails

If the $OHM price rises and the short fails, the borrower must buy $OHM at a higher price in order to repay principal plus interest. All $OHM returned to the protocol is burned, and the borrower withdraws their collateral. In this scenario, the borrower realizes a loss. However, $OHM supply still decreases through the burned principal and interest, and the collateral yield accumulated during the loan duration would have been routed to YRF to fund additional buybacks.

If collateral value drops below 115% LTV, a liquidator would repay the outstanding $OHM debt and receive the corresponding $USDS collateral plus a liquidation bonus of 3%. Once liquidated, the repaid $OHM would be burned.

Short wins

If the $OHM price falls and the short succeeds, the borrower repurchases $OHM at a lower price, repays principal plus interest, and withdraws their collateral while retaining profit. All repaid $OHM is again burned. Supply contracts in exactly the same way as in the loss case. In addition, the yield generated throughout the duration of the loan would have supported YRF buybacks, likely at progressively cheaper $OHM prices during a declining market. In both profit and loss outcomes, the structural result is supply reduction.

How Burner Loans Generate Value for $OHM

Adding native short leverage to Olympus, would likely increase volatility, which tends to make Convertible Deposits more attractive and increase their uptake. At the same time, higher turnover would raise trading volume across POL, strengthening fee capture and improving the efficiency of Olympus. Both effects compound into higher revenue that will be routed into buybacks, while every Burner position still ends in $OHM being repaid and burned, turning short activity into a source of supply reduction.

Legacy: Deprecated Mechanisms

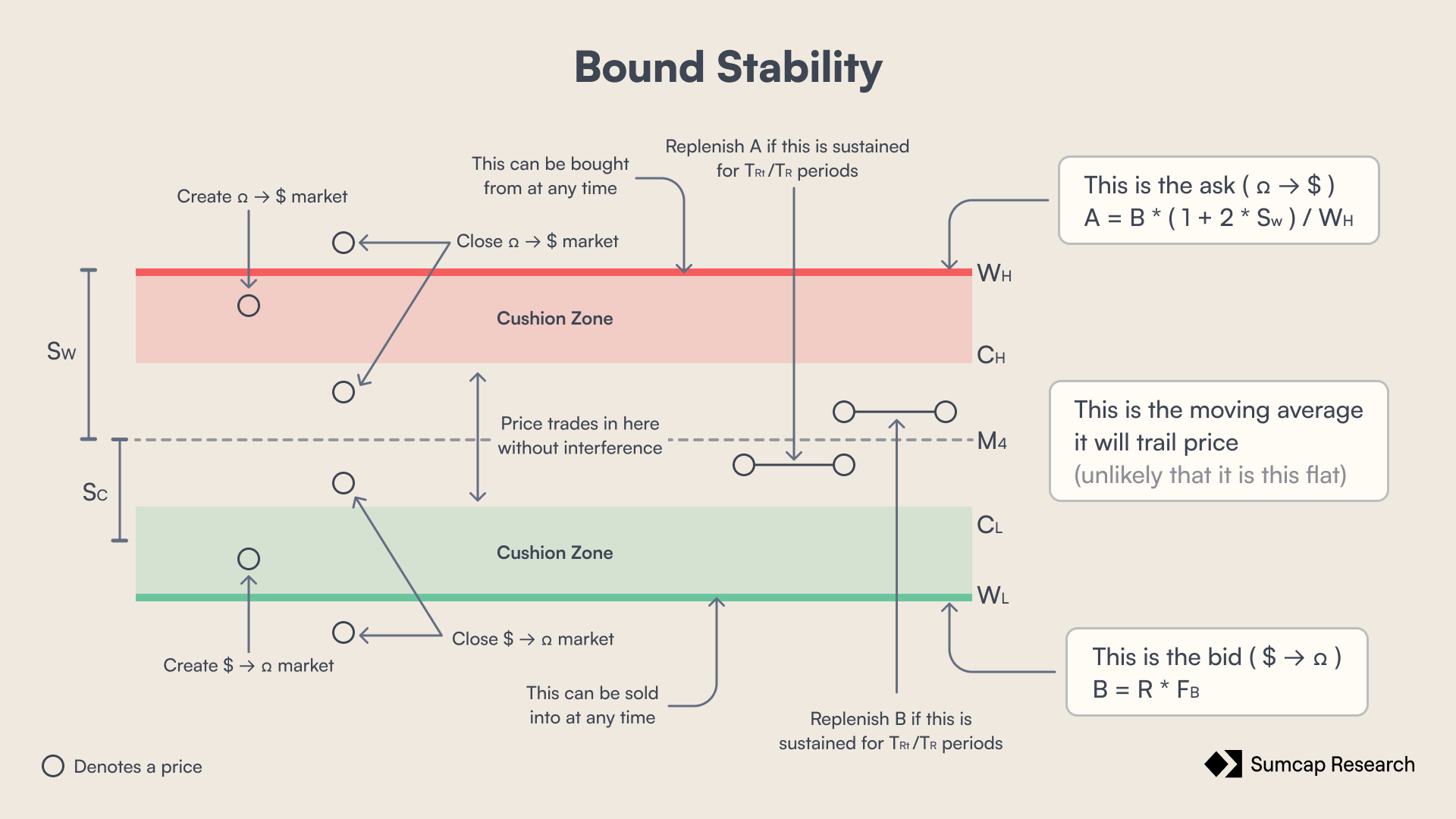

Range-Bound Stability (RBS)

Range-Bound Stability was Olympus’s original automated market operations framework, now replaced by Convertible Deposits and the YRF. It aimed to keep $OHM trading within a price band relative to its book value by maintaining a moving average (MA) of the $OHM/$USDS price over a configurable window (commonly 30 days), updated each system epoch.

RBS defined four price levels around MA using two governance-set spreads which were a wider Wall Spread and a tighter Cushion. The expressions of that walls are the following:

\[\ \text{Lower}_{\text{Wall}} = \text{MA} \times \left(1 - \text{Wall}_{\text{Spread}}\right)\ \]

\[\ \text{Upper}_{\text{Wall}} = \text{MA} \times \left(1 + \text{Wall}_{\text{Spread}}\right)\ \]

\[\ \text{Lower}_{\text{Cushion}} = \text{MA} \times \left(1 - \text{Cushion}_{\text{Spread}}\right)\ \]

\[\ \text{Upper}_{\text{Cushion}} = \text{MA} \times \left(1 + \text{Cushion}_{\text{Spread}}\right)\ \]

At the walls, Olympus became a direct counterparty. At the lower wall, users could swap $OHM for reserves directly with the protocol without open-market slippage. At the upper wall, users could swap reserves for $OHM directly without pushing price higher.

In both directions, Olympus relied on arbitrage to pull market price back toward the band.

Wall sizing was explicitly tied to the balance sheet.

The lower wall’s capacity (the bid) equalled a configured share of treasury reserves, effectively buying more when the reserves were rich.

\[\ \text{Bid}_{\text{Capacity}} = \text{Bid}_{\text{Factor}} \times \text{Reserves}\ \]

The upper wall (the ask) expressed capacity in $OHM terms, derived from bid capacity adjusted for the full spread:

\[\ \text{Ask}_{\text{Capacity}} = \text{Bid}_{\text{Capacity}} \times \frac{\left(1 + 2 \times \text{Wall}_{\text{Spread}}\right)}{\text{Upper}_{\text{Wall Price}}}\ \]

Once a wall’s capacity was depleted, the protocol stopped offering swaps on that side.

The cushions zones were softer, earlier interventions. When $OHM price reached the upper cushion boundary, Olympus deployed an instant-swap bond market selling $OHM for reserves. Pricing started at the upper wall price and could move down, bounded by the upper cushion price. The market closed if price reverted below the upper cushion, exceeded the upper wall, or if upper wall capacity was depleted. The lower cushion behaved symmetrically, buying $OHM with reserves.

Basically, the protocol automatically contracted supply in bearish conditions and expanded supply in overheated conditions. The intent was not to ‘peg’ $OHM, but to prevent disorderly downside deviations relative to its backing.

Ecosystem

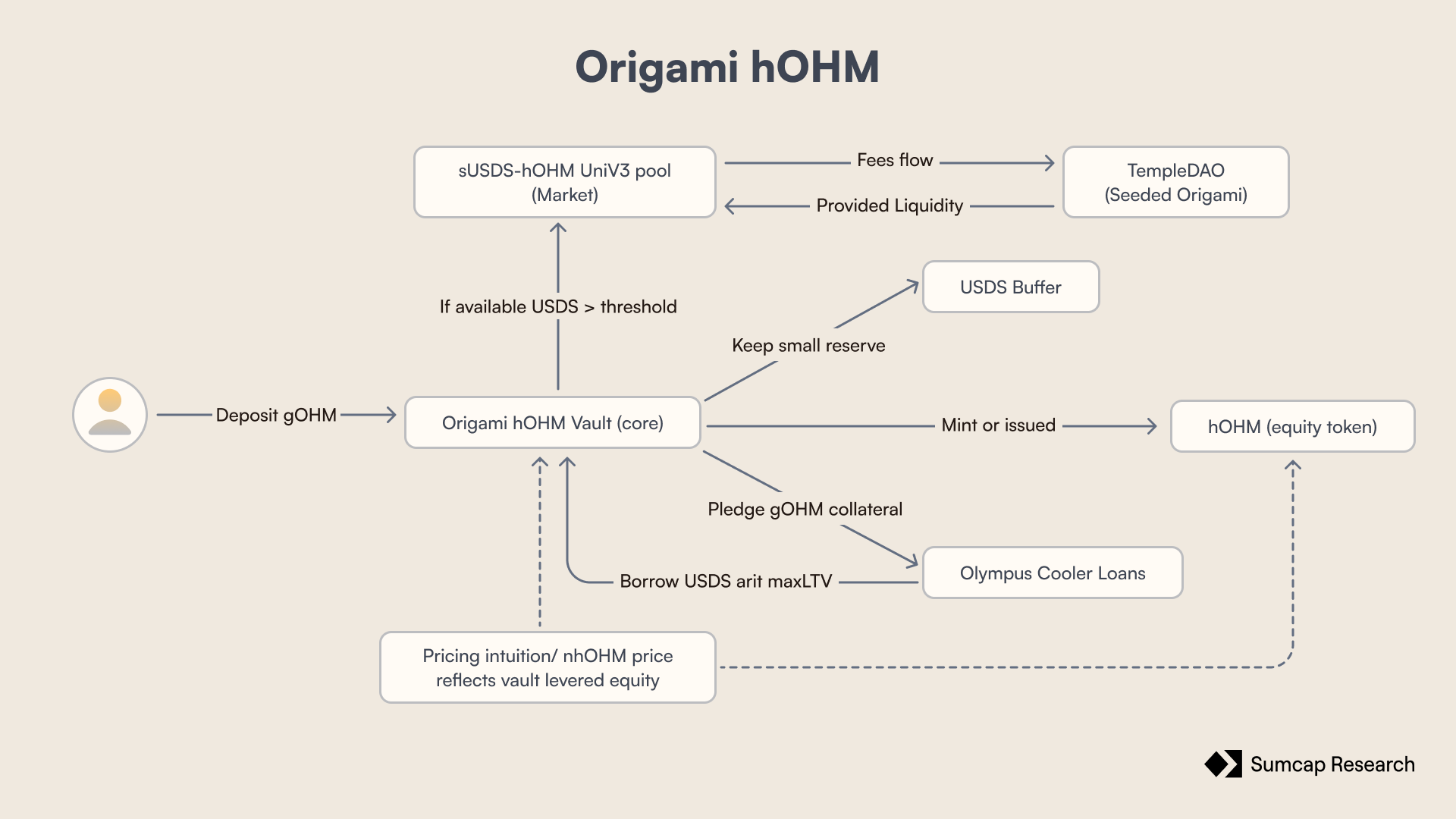

Origami’s hOHM

hOHM is Origami’s ‘lovOlympus’ vault token a liquid, automated, and optimised maximally-leveraged $OHM exposure token built on top of Olympus Cooler Loans. At a high level, $hOHM does $OHM looping automatically.

Users deposit $gOHM into Origami and receive $hOHM, representing the vault’s equity in a maximally-leveraged $OHM position. The vault borrows $USDS against the $gOHM collateral using Cooler Loans, exploiting the single-position-per-user structure and the automatic LTV increase toward OLTV. Origami can borrow close to the maximum and keep a small $USDS reserve to service interest by depositing it into SSR, so the position can remain healthy even with zero drip.

As the Cooler Loan’s effective borrow capacity increases toward the target LTV, Origami auto-borrows additional $USDS. That $USDS is used to increase $OHM exposure and keep the vault near target leverage. When available $USDS exceeds an internal threshold, Origami sources liquidity (e.g., via the sUSDS/hOHM UniV3 pool) to buy $hOHM from the market and burn it, updating $hOHM supply to reflect the vault’s evolving equity. The $hOHM price reflects the value of the vault’s levered equity.

Origami drives value to Olympus through three channels: structural demand for OHM/gOHM, treasury revenue via Cooler Loan interest, and market buy pressure created by the vault’s leverage rebalancing.

Berachain Investment

Olympus made a strategic investment in Berachain on April 1, 2022, at a $25M effective valuation ($50M FDV with deal terms). Payment was made in $OHM across three transactions: 99K $OHM (4/21/22), 95K $OHM (5/9/22), and 300K $OHM (6/2/22).

Vesting terms: 16.67% released at the 6-month anniversary of TGE (Feb 6, 2026), with the remaining 83.33% unlocking in equal monthly instalments over 30 months, reaching full unlock in August 2028.

Olympus received 4.245.099 $IBERA and 750.000 $IBERA, both held by BitGo. The community is currently seeking support to potentially exit through all available venues, depending on which provides the best overall outcome for the treasury.

Governance

The live framework is powered by $gOHM voting, a modified Governor Bravo with percent-based thresholds, and multisig-based controls that are being progressively migrated to on-chain timelock control.

To submit a proposal, a proposer must meet a threshold defined as a percentage of total $gOHM supply.

Once submitted, there is a 3-day voting delay before the 7-day voting period opens. Passing requires a quorum of 20% of $gOHM supply voting FOR at activation time, and an approval threshold of 60% of voting supply being FOR.

After passing, proposals enter a 1-day execution delay through the Governor Bravo Timelock, which holds privileged permissions.

For a full reference of configurable protocol parameters, contract addresses, and multisig signers, click here.

In early 2026, the Olympus Association proposed a credit line structure for FY26 operational funding (February 2026 to February 2027), requesting a credit line of up to 500,000 $OHM with a purchase option at the greater of 12 $USDS or liquid backing. Drawn $OHM must be repaid or purchased within 3 months.

The budget is expected to be similar to previous year which landed at $1.33M against an original $888K target, with the overshoot attributed to team expansion, Callisto development ($240K), and increased project scope

The credit line would also serve as a tool for strategic OTC deals with institutions in case the proposal passes.

Conclusions

Most protocols pick one direction, inflationary emissions or deflationary buybacks, and commit to it regardless of conditions. Olympus does both, but only when market signals warrant it, and shuts each mechanism off when they don't. That reflexivity is the core insight. Supply responds to demand, and the treasury captures value on both sides of the cycle. If the parameters stay well-tuned, this is one of the few token models that can genuinely compound backing per token over time.

The system performs very differently depending on which regime $OHM sits in. When the premium is high, every mechanism reinforces the others and the flywheel compounds. When premium is low, the protocol runs almost entirely on savings yield routed through the YRF and the flywheel slows considerably. Olympus's long-term thesis depends quite a bit on the belief that these quiet periods are temporary.

The YRF's execution is the most obvious area where value leaks. The 0.6% weighted average overpay to arbitrage bots on Bond Protocol means the protocol is systematically leaving value on the table. Whether Olympus has the governance appetite to explore tighter execution venues will matter more over time.

If Olympus can improve execution, it will make the model’s edge more effective.

OlympusDAO: An Onchain Monetary System

Most DeFi projects barely think about what should give their token real value. Supply mechanics get locked in before the token even hits the market, with emissions and burns following a fixed timeline instead of adapting to market conditions. OlympusDAO, exact opposite of this.

Olympus DAO built an on-chain monetary system very similar to a central bank that manages a treasury with the aim to accrue value and utility to $OHM.

The treasury holds a diversified reserve base, namely $USDS and $sUSDe alongside other high-quality and is operated through dedicated treasury and policy wallets with scoped mandates. These wallets execute reserve management, deploy capital, service credit, and route generated yield back into policy mechanisms.

Olympus Architecture

The treasury is the cornerstone of Olympus. It holds reserves and deploys them across three active mechanisms.

- Cooler Loans, a native credit facility;

- Yield Repurchase Facility (YRF), an automated buyback-and-burn engine;

- Convertible Deposits, demand-responsive $OHM issuance.

Each mechanism is designed to convert treasury activity into token holder value through a different channel.

This report explains Olympus through its core mechanisms, then connects them into a single system view focusing on second-order implications.

Active Mechanisms

Cooler Loans

Cooler Loans let users borrow $USDS directly from the Olympus Treasury by using $gOHM as collateral. Those Loans pay a fixed 0.5% APR (set by governance) and have no price-based liquidations, as they use the OLTV as reference price. Loans only default if unpaid interest accumulates past a governance-defined threshold.

The OLTV capacity expands over time via a LTV drip (governance-set), which gradually increases the borrowing capacity toward a target on a schedule, instead of relying on market price or external oracle feeds for liquidation logic. This is a deliberately slow, governance-controlled expansion rather than a market-reactive.

The Initial OLTV ratio (as of May 15, 2025) was ~11 USDS/OHM (2961.64 USDS/gOHM) with a target of 11.11 USDS/OHM, this was achieved on March 6th 2026.

The liquid backing per $OHM price is the dollar amount of stablecoins, volatile assets and protocol-owned liquidity in the treasury, excluding $OHM. It serves as the fundamental solvency guarantee, as the OLTV is always set at a safe discount relative to the actual backing, ensuring the protocol remains solvent even if borrowers default.

The recent rise of the backing price is due to the fact that Olympus has started to burn the gOHM that where in the TokenMigrator contract as they are starting to deprecate it.

The primary use case of Cooler Loans is enabling capital-efficient leveraged $OHM exposure. At 0.5% APR with no liquidation risk from price volatility, Cooler Loans become the cheapest leverage in DeFi for $OHM. Borrowers can loop by borrowing $USDS, acquiring more OHM/gOHM, and adding collateral, creating leverage without liquidation cascades from market volatility (though default risk still exists if interest is not serviced). Also, as the borrow APY is so low, it's extremely useful to do a carry trade with this unlocked capital.

How do Cooler Loans generate value for $OHM?

First, interest paid on Cooler debt accrues directly to the Olympus treasury that feeds back into buyback capacity via the Yield Repurchasing Facility (YRF). Second, in case of default, the position is closed and the $gOHM collateral is burned. This reduces circulating gOHM/OHM claims while the previously borrowed $USDS automatically returns to the Treasury. Defaults are supply-supportive as borrowers lose collateral, but remaining holders get a more concentrated claim on reserves.

The trade-off is that Cooler Loans force a choice between growth and treasury optimisation. Lending $USDS at 0.5% lowers the treasury’s aggregate yield compared with allocating that same $USDS into higher yielding reserve strategies (for example, $USDS savings at around 4.5% APY). The effective cost of Cooler shifts with prevailing stablecoin yield.

Yield Repurchase Facility (YRF)

The Yield Repurchase Facility (YRF) is the automated buyback-and-burn engine.

The YRF increases its purchasing power by recycling backing, it buys $OHM (via Bond Protocol), then burns that $OHM and withdraws $USDS reserves from the Treasury at the max OLTV. This reduces $OHM supply and converts purchased $OHM into additional $USDS budget for future buybacks.

The architecture that the YRF uses to increase its purchasing power is essentially the same as the one used for Cooler Loans.

Mechanism & Cadence

The YRF is a smart contract that runs on Heart beats (every 8 hours). Its flows are split into two timescales: a weekly accounting step and daily execution.

Once per week, the system calculates the prior week’s yield earned from two sources:

- reserves deposited in the $USDS savings vault (~3.75% APY in SSR)

- interest earned from Cooler Loans (the 0.5% APY borrow rate).

Then, the contract pulls previous week’s computed yield from the Treasury in $SUSDS. Every day, a four-step execution loop runs.

- The YRF tracks $OHM captured from the prior day’s purchases (this $OHM sits in the YRF contract).

- Burn $OHM and, in exchange, withdraws reserves from the Treasury equal to a preconfigured backing value per $OHM.

- Unwraps one day’s worth of $USDS from its $SUSDS holdings for today’s buyback.

- Opens a 1-day Bond Protocol market to buy $OHM using

- today’s $USDS yield allocation

- the recycled $USDS backing obtained from the burn step.

Performance & Efficiency

So far, OlympusDAO has bought more than 11M $OHM through all its different mechanisms, including Inverse Bonds, the RBS lower cushion, YRF, and TWAP execution. These are gross purchases so they do not net out any $OHM that may have been sold elsewhere.

Within that total, YRF alone has bought and burned roughly 650k $OHM at an average price of $20.42 per $OHM.

Execution is not perfectly efficient as YRF routes purchases through Bond Protocol instead of sourcing directly from open markets, where arbitrage bots capture part (or most) of the spread. On a weighted basis, YRF has paid about 0.6% above the market price, and nearly half of Bond Protocol counterparties are bots, which suggests there is consistent extractable profit between the two venues.

Even with this leakage, the system still delivers what it is designed for. It creates persistent, buy flow and compresses supply through burns, which lowers circulating $OHM and reduces selling pressure from large holders.

Convertible Deposits & the Emissions Manager

When the premium (market value / backing value) exceeds a governance-set minimum premium (currently 100%, meaning $OHM trades at 2x or more of backing), the Emissions Manager activates a Convertible Deposits auction, offering a computed amount of newly issued $OHM in exchange for fresh $USDS reserves.

If the premium target has not been reached, the auction is disabled.

The equation for this emission is:

\[\ \text{NewSupply} = \text{TotalSupply} \times \text{BaseEmissionsRate} \times \frac{\left(\text{Premium} + 100\%\right)}{\left(\text{MinPremium} + 100\%\right)}\ \]

Where:

- Base emissions rate -> the base percentage of circulating supply to be sold per day (at minimum premium), currently 0.02% per day.

- Emissions rate = Base Rate × (1 + premium) / (1 + min premium)

- Minimum premium rate -> the threshold premium required for emissions to be active (set by governance)

- Premium = market price / backing price

The higher the premium, the greater the emission rate will be, effectively creating more sell pressure when the market overbuys $OHM.

At current settings, Convertible Deposits only turn on when $OHM trades at least 2.0× backing ( minPremium = 100%). In this case, Olympus prefers to monetise demand by selling newly issued $OHM (locked) for fresh reserves ($USDS) to grow the treasury, rather than letting premiums run.

Once active, governance has two main levers that control how aggressive this reflex becomes:

- minPremium (activation threshold): Higher values make emissions rarer but more “event-driven.” Lower values make emissions more frequent and start clipping premium earlier.

- baseRate (slope/throughput): Sets the baseline fraction of supply the system is willing to sell per day at exactly minPremium (currently at 0,02%/day), and scales linearly with premium. Increasing baseRate makes the system respond faster, but also increases the risk of overshooting and pushing premium down too hard.

This creates a negative feedback loop. Premium expands, emissions scale up, supply is sold into demand for $USDS, and the premium is pulled back toward the activation boundary. When premium cools below the threshold, emissions shut off. Convertible Deposits are a way to convert moments of demand into reserves, while using the auction format to push as much of the ‘premium monetisation’ as possible onto takers.

Auction Mechanics

The auction uses a tick-based system for dynamic price discovery.

- The system determines how many deposit tokens are needed to fill the remaining capacity of the current tick.

- If the bid exceeds this amount, it fills the current tick completely and moves to the next higher-priced tick.

- This continues across multiple ticks until the entire bid is processed.

If there are large bids spanning multiple ticks drive prices up faster, and insufficient demand causes tick prices to decay over time (with a floor set by auction parameters).

In case that $OHM is under-sold during the auction, a Bond Protocol market is created as a fallback to sell the remainder.

Convertible Deposits as a User

Users deposit $USDS and receive receipt tokens plus a non-fungible position that locks in a specific conversion price for $OHM (below current market).

Once the maturity day arrives, the user that has bought a CD has two choices:

- Execute the call option and get the $OHM, increasing the backing

- Redeem the $USDS deposited (This only makes sense if the market price < option)

If a user decides to redeem the $USDS before the maturity date, Olympus would take a 10% penalty fee that would be redirected to the treasury, increasing $OHM backing and reducing the premium.

While the position is open, the protocol deploys the deposited $USDS to earn yield until maturity, and that yield feeds into YRF buybacks. This makes the structure accretive across outcomes.

System Overview: How the Mechanisms Connect

All of these mechanisms affect $OHM supply, so the easiest way to see how they connect is to walk through a concrete scenario.

Imagine a user wants $OHM exposure. A capital efficient way to get it is to buy $OHM on the open market and then use a Cooler Loan, since the carry cost is close to zero. As the user buys, their order flow pushes price up, which also increases the $OHM premium.

At that point Olympus has already captured value. A large share of onchain liquidity is controlled by the protocol, so it earns swap fees on that flow. Olympus also earns the 0.5% APY on the borrowed $USDS, which increases the treasury over time.

Now the premium sits above the minimum threshold, so the Emissions Manager enables Convertible Deposits to stop price from drifting too far above backing. In practice, the protocol opens a bond style sale where users deposit $USDS in exchange for a position that can be converted into $OHM at a discounted conversion price.

After the sale, participant $USDS is moved into separate custody and deployed to farm yield until maturity. When maturity arrives, users choose whether to exercise. If they exercise, their $USDS moves to the treasury and continues earning yield while they receive $OHM. If they do not exercise, Olympus returns 100% of the deposited $USDS and keeps the yield earned during the term. If someone exits early, Olympus keeps 10% of the principal as a fee.

If enough users exercise, the additional $OHM supply creates near term sell pressure that tends to compress the premium. Once the premium falls back under the threshold, Convertible Deposits switch off.

All yield collected across the system feeds into YRF. That includes interest from Cooler Loans, fees from protocol owned liquidity, and the yield generated on Convertible Deposit USDS. YRF then uses this yield to buy $OHM.

Once per week, the YRF calculates last week’s yield earned, then pulls that amount from the Treasury as $SUSDS to fund the next week’s operations, and then every day it:

- Looks at the $OHM it bought the prior day;

- Borrows $USDS against that $OHM at a preset backing value, and burns the $OHM;

- Unwraps one day’s worth of $USDS out of $SUSDS for spending;

- Opens a 1-day Bond Protocol market that uses (today’s yield $USDS + the borrowed $USDS) to buy $OHM over that day.

YRF helps the price of $OHM by acting as a marginal buyer and burning supply. Additionally, as YRF buys $OHM that gets arbed in the open market, the premium (with no uptick in demand) becomes higher, and the loop may start again.

What's to Come

Burner Loans

At present, bearish positioning must occur externally, either through spot selling or derivatives markets. That activity does not directly benefit the protocol, that's what Burner Loans aim to internalize.

Where Cooler Loans allow users to borrow stables against $gOHM collateral and take leveraged long exposure, Burner Loans would allow users to borrow $OHM against $SUSD collateral and take short exposure.

Outcomes

Short fails

If the $OHM price rises and the short fails, the borrower must buy $OHM at a higher price in order to repay principal plus interest. All $OHM returned to the protocol is burned, and the borrower withdraws their collateral. In this scenario, the borrower realizes a loss. However, $OHM supply still decreases through the burned principal and interest, and the collateral yield accumulated during the loan duration would have been routed to YRF to fund additional buybacks.

If collateral value drops below 115% LTV, a liquidator would repay the outstanding $OHM debt and receive the corresponding $USDS collateral plus a liquidation bonus of 3%. Once liquidated, the repaid $OHM would be burned.

Short wins

If the $OHM price falls and the short succeeds, the borrower repurchases $OHM at a lower price, repays principal plus interest, and withdraws their collateral while retaining profit. All repaid $OHM is again burned. Supply contracts in exactly the same way as in the loss case. In addition, the yield generated throughout the duration of the loan would have supported YRF buybacks, likely at progressively cheaper $OHM prices during a declining market. In both profit and loss outcomes, the structural result is supply reduction.

How Burner Loans Generate Value for $OHM

Adding native short leverage to Olympus, would likely increase volatility, which tends to make Convertible Deposits more attractive and increase their uptake. At the same time, higher turnover would raise trading volume across POL, strengthening fee capture and improving the efficiency of Olympus. Both effects compound into higher revenue that will be routed into buybacks, while every Burner position still ends in $OHM being repaid and burned, turning short activity into a source of supply reduction.

Legacy: Deprecated Mechanisms

Range-Bound Stability (RBS)

Range-Bound Stability was Olympus’s original automated market operations framework, now replaced by Convertible Deposits and the YRF. It aimed to keep $OHM trading within a price band relative to its book value by maintaining a moving average (MA) of the $OHM/$USDS price over a configurable window (commonly 30 days), updated each system epoch.

RBS defined four price levels around MA using two governance-set spreads which were a wider Wall Spread and a tighter Cushion. The expressions of that walls are the following:

\[\ \text{Lower}_{\text{Wall}} = \text{MA} \times \left(1 - \text{Wall}_{\text{Spread}}\right)\ \]

\[\ \text{Upper}_{\text{Wall}} = \text{MA} \times \left(1 + \text{Wall}_{\text{Spread}}\right)\ \]

\[\ \text{Lower}_{\text{Cushion}} = \text{MA} \times \left(1 - \text{Cushion}_{\text{Spread}}\right)\ \]

\[\ \text{Upper}_{\text{Cushion}} = \text{MA} \times \left(1 + \text{Cushion}_{\text{Spread}}\right)\ \]

At the walls, Olympus became a direct counterparty. At the lower wall, users could swap $OHM for reserves directly with the protocol without open-market slippage. At the upper wall, users could swap reserves for $OHM directly without pushing price higher.

In both directions, Olympus relied on arbitrage to pull market price back toward the band.

Wall sizing was explicitly tied to the balance sheet.

The lower wall’s capacity (the bid) equalled a configured share of treasury reserves, effectively buying more when the reserves were rich.

\[\ \text{Bid}_{\text{Capacity}} = \text{Bid}_{\text{Factor}} \times \text{Reserves}\ \]

The upper wall (the ask) expressed capacity in $OHM terms, derived from bid capacity adjusted for the full spread:

\[\ \text{Ask}_{\text{Capacity}} = \text{Bid}_{\text{Capacity}} \times \frac{\left(1 + 2 \times \text{Wall}_{\text{Spread}}\right)}{\text{Upper}_{\text{Wall Price}}}\ \]

Once a wall’s capacity was depleted, the protocol stopped offering swaps on that side.

The cushions zones were softer, earlier interventions. When $OHM price reached the upper cushion boundary, Olympus deployed an instant-swap bond market selling $OHM for reserves. Pricing started at the upper wall price and could move down, bounded by the upper cushion price. The market closed if price reverted below the upper cushion, exceeded the upper wall, or if upper wall capacity was depleted. The lower cushion behaved symmetrically, buying $OHM with reserves.

Basically, the protocol automatically contracted supply in bearish conditions and expanded supply in overheated conditions. The intent was not to ‘peg’ $OHM, but to prevent disorderly downside deviations relative to its backing.

Ecosystem

Origami’s hOHM

hOHM is Origami’s ‘lovOlympus’ vault token a liquid, automated, and optimised maximally-leveraged $OHM exposure token built on top of Olympus Cooler Loans. At a high level, $hOHM does $OHM looping automatically.

Users deposit $gOHM into Origami and receive $hOHM, representing the vault’s equity in a maximally-leveraged $OHM position. The vault borrows $USDS against the $gOHM collateral using Cooler Loans, exploiting the single-position-per-user structure and the automatic LTV increase toward OLTV. Origami can borrow close to the maximum and keep a small $USDS reserve to service interest by depositing it into SSR, so the position can remain healthy even with zero drip.

As the Cooler Loan’s effective borrow capacity increases toward the target LTV, Origami auto-borrows additional $USDS. That $USDS is used to increase $OHM exposure and keep the vault near target leverage. When available $USDS exceeds an internal threshold, Origami sources liquidity (e.g., via the sUSDS/hOHM UniV3 pool) to buy $hOHM from the market and burn it, updating $hOHM supply to reflect the vault’s evolving equity. The $hOHM price reflects the value of the vault’s levered equity.

Origami drives value to Olympus through three channels: structural demand for OHM/gOHM, treasury revenue via Cooler Loan interest, and market buy pressure created by the vault’s leverage rebalancing.

Berachain Investment

Olympus made a strategic investment in Berachain on April 1, 2022, at a $25M effective valuation ($50M FDV with deal terms). Payment was made in $OHM across three transactions: 99K $OHM (4/21/22), 95K $OHM (5/9/22), and 300K $OHM (6/2/22).

Vesting terms: 16.67% released at the 6-month anniversary of TGE (Feb 6, 2026), with the remaining 83.33% unlocking in equal monthly instalments over 30 months, reaching full unlock in August 2028.

Olympus received 4.245.099 $IBERA and 750.000 $IBERA, both held by BitGo. The community is currently seeking support to potentially exit through all available venues, depending on which provides the best overall outcome for the treasury.

Governance

The live framework is powered by $gOHM voting, a modified Governor Bravo with percent-based thresholds, and multisig-based controls that are being progressively migrated to on-chain timelock control.

To submit a proposal, a proposer must meet a threshold defined as a percentage of total $gOHM supply.

Once submitted, there is a 3-day voting delay before the 7-day voting period opens. Passing requires a quorum of 20% of $gOHM supply voting FOR at activation time, and an approval threshold of 60% of voting supply being FOR.

After passing, proposals enter a 1-day execution delay through the Governor Bravo Timelock, which holds privileged permissions.

For a full reference of configurable protocol parameters, contract addresses, and multisig signers, click here.

In early 2026, the Olympus Association proposed a credit line structure for FY26 operational funding (February 2026 to February 2027), requesting a credit line of up to 500,000 $OHM with a purchase option at the greater of 12 $USDS or liquid backing. Drawn $OHM must be repaid or purchased within 3 months.

The budget is expected to be similar to previous year which landed at $1.33M against an original $888K target, with the overshoot attributed to team expansion, Callisto development ($240K), and increased project scope

The credit line would also serve as a tool for strategic OTC deals with institutions in case the proposal passes.

Conclusions

Most protocols pick one direction, inflationary emissions or deflationary buybacks, and commit to it regardless of conditions. Olympus does both, but only when market signals warrant it, and shuts each mechanism off when they don't. That reflexivity is the core insight. Supply responds to demand, and the treasury captures value on both sides of the cycle. If the parameters stay well-tuned, this is one of the few token models that can genuinely compound backing per token over time.

The system performs very differently depending on which regime $OHM sits in. When the premium is high, every mechanism reinforces the others and the flywheel compounds. When premium is low, the protocol runs almost entirely on savings yield routed through the YRF and the flywheel slows considerably. Olympus's long-term thesis depends quite a bit on the belief that these quiet periods are temporary.

The YRF's execution is the most obvious area where value leaks. The 0.6% weighted average overpay to arbitrage bots on Bond Protocol means the protocol is systematically leaving value on the table. Whether Olympus has the governance appetite to explore tighter execution venues will matter more over time.

If Olympus can improve execution, it will make the model’s edge more effective.

.svg)