Inside TempleDAO's Treasury

Most DeFi treasuries have no framework to deploy capital or measure performance. TempleDAO built an on-chain treasury that not only grows by generating yield that grows the price floor of its main asset. Here's the full breakdown.

Treasury Reserve Vault (TRV)

The TRV sits at the center of TempleDAO’s capital allocation architecture. It custody-holds core reserves and functions as an internal lender to approved strategy borrowers. The borrow-and-repay framing creates an accounting model that makes strategies directly comparable against a common benchmark.

TRV Architecture

The TRV is a DAI-based reserve where every loan must be authorised by governance. To protect the protocol, governance assigns each borrower a strict spending limit (debt ceiling). Furthermore, the system uses automated circuit breakers to stop unusually large or suspicious transfers, ensuring that even if a borrower is approved, they cannot accidentally or intentionally drain the treasury.

For a full reference of configurable protocol parameters, contract addresses and signers, see here.

Each treasury strategy is implemented as a whitelisted Strategy Borrower contract that draws capital from the TRV, deploys it into a defined opportunity set, and repays over time. The framework supports two operational models; automated strategies, which operate with deterministic, programmatic execution of borrows and repayments, and manually operated strategies that use a wrapper pattern where the borrower contract serves as the accounting shell while execution is delegated to an operator multisig for discretionary actions. In both cases, treasury capital usage is tracked as debt, and the strategy must eventually return capital through the repayment rail.

When a strategy draws funds, the system mints internal debt-share tokens ($dUSD for stable-denominated loans, $dTEMPLE for TEMPLE-denominated loans) representing principal owed to the TRV. The debt balance accrues at a continuously compounding Treasury Funding Rate:

\[r_{\text{funding}} = r_{\text{benchmark}} + r_{\text{risk premium}} \]

Currently \( r_{\text{risk premium}} = 0 \) for all strategies.

The benchmark rate represents the treasury’s baseline opportunity cost (referenced to the Origami sUSDS+ vault yield), while the risk premium encodes the additional required return for strategy-specific risks. This framework forces every strategy to clear a hurdle rate, meaning that if its producing nominal yield but failing to outperform the benchmark after premium then, in treasury accounting terms, underperforming.

Since all strategies carry a debt ceiling, a persistently underperforming strategy will see its accrued debt grow toward the ceiling. At that point, it must either repay the TRV or face governance action to close or restructure. To date, no strategy has triggered this scenario.

Active Strategies

As of March 2026, the TempleDAO treasury runs multiple strategies whose combined holdings are displayed at ~$130M. However, this figure is misleading as it represents the raw market value of all assets sitting in the strategy wallets without subtracting liabilities.

The net exposure, which strips out borrowed capital and accounts for outstanding debt, sits at roughly $47M. The gap between the two numbers is the clearest indicator of how aggressively the treasury uses leverage across its strategy set.

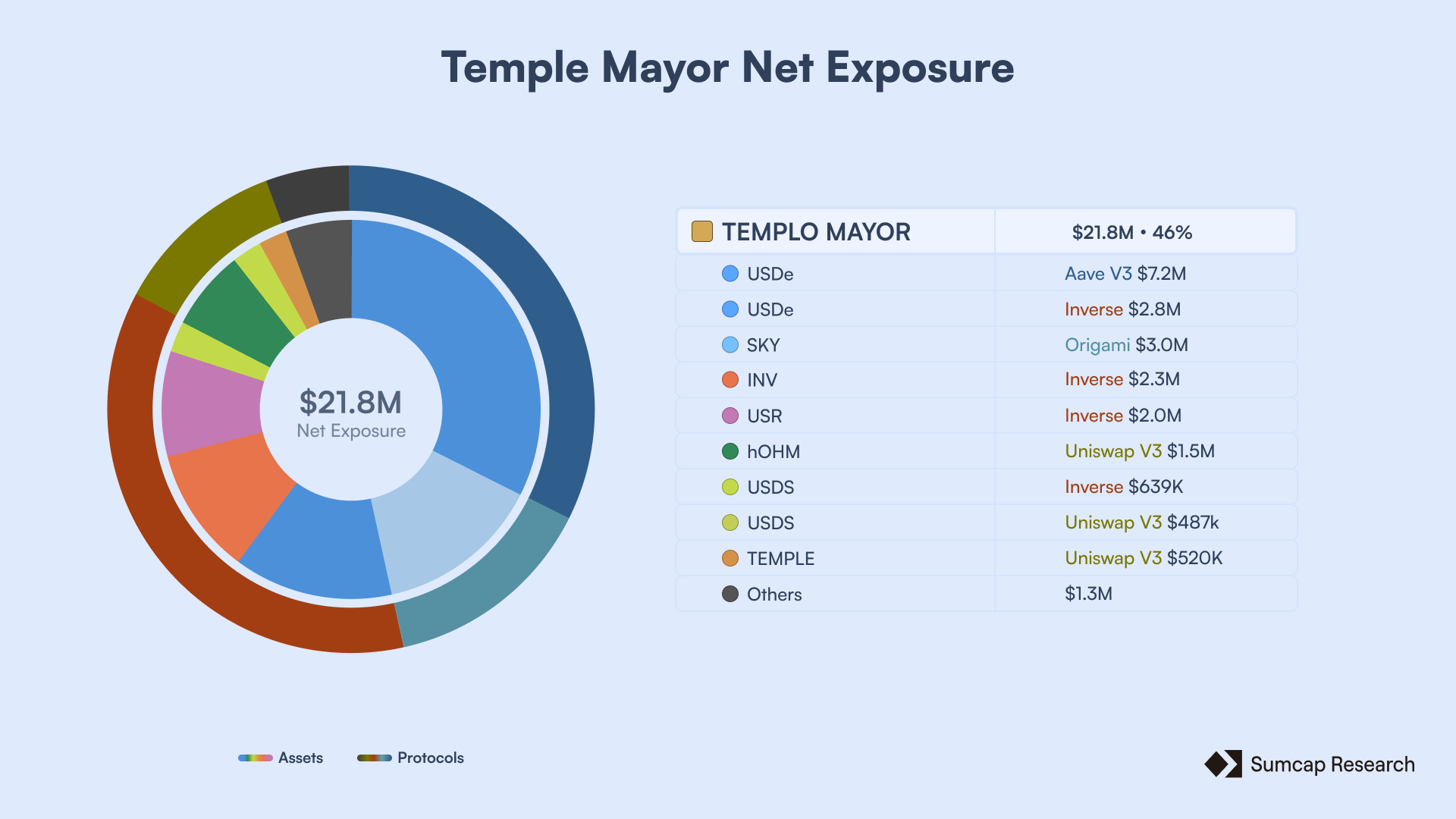

Templo Mayor (Omnibus Strategy)

Templo Mayor is TempleDAO’s largest and most complex strategy, structured as an Omnibus Strategy operated through a Gnosis Safe multisig. This format is used when full automation is not feasible due to technical or operational constraints. Unlike a single-position automated strategy, Templo Mayor groups multiple related exposures under the same umbrella while maintaining the same debt-tracking and approval framework.

The strategy's dashboard displays holdings of over $103M, but this figure also represents gross exposure:

After subtracting all liabilities, the net exposure is approximately $22M.

The strategy was initially funded with an initial credit line of $24.4M from the TRV and currently maintains roughly $22M in net assets, with an important negative benchmark equity, what suggests that the strategy is not performing as expected.

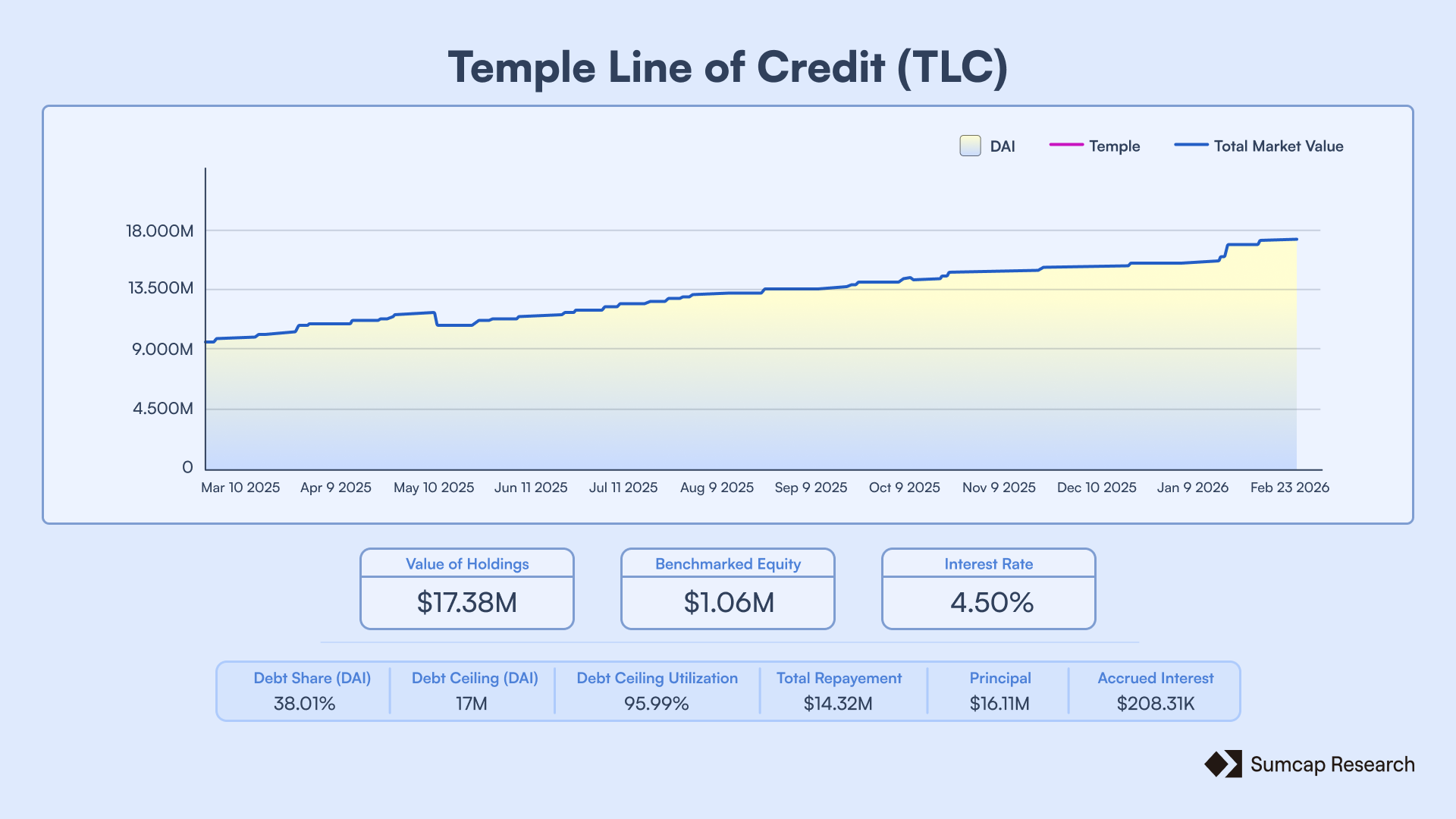

Temple Line of Credit (TLC)

TLC converts a portion of the treasury’s stablecoin reserves into a risk-managed lending book. The DAO allocates $DAI (notably, this strategy has not migrated to $USDS) as a borrowable asset against $TEMPLE. Collateral valuation is anchored to the Treasury Price Index (TPI) rather than spot market price, providing borrowers with more stable and predictable terms. More to follow on the TPI below. Since inception it, has generated $1.05M in excess returns over the benchmark rate, with $14.32M in total repayments and $185.29K in accrued interest. The strategy currently holds $16.94M with a benchmarked equity of $1.05M, confirming consistent performance above the hurdle rate.

Borrowers can draw up to 85% loan-to-value (LTV), with liquidation triggered at 90% LTV. The borrow rate is periodically recalibrated using the formula:

\[ \text{Borrow}_{\text{rate}} = \text{sDAI} _{\text{rate}} \times \max(1.1, 1 + \text{TEMPLE}_{\text{staked}}\%) \]

With the above expression, Temple ensures that this strategy will always outperform the DAI Savings Rate by at least 10%. Currently, this benchmark reflects a yield of 1.25% for sDAI, though it is important to note the wider yield environment: the Sky Savings Rate (SSR) for USDS is providing a higher baseline of 3.75%. This follows a recent 25bps reduction from its previous 4% target, which was implemented on March 9, 2026.

FOHMO

FOHMO maintains a maximally looped $OHM position based on Cooler loans, using Origami hOHM as the execution vehicle. This strategy has had a really good performance thanks to the good timing that TempleDAO had with the repayments to the TRV.

The total value of holdings ($8.86M) reflects only the gross value still sitting inside FOHMO today. It does not capture value that has already been realised and returned to the treasury through repayments ($8.19M total). Additionally, the strategy currently shows 0% debt ceiling utilisation, indicating no open debt position. The benchmarked equity stands at $13.97M, representing pure profit after accounting for all capital costs.

Base Sky Autofarm

Idle capital in the TRV is automatically directed to a Base Strategy to earn yield (i.e., $USDS received from Temple Gold Auctions). The current implementation of the Base Strategy deposits idle capital into the Sky Auto Farm through Origami sUSDS+ which deploys $SUSDS choosing the most optimal farm between vanilla $USDS staking and farming $SKY with auto-compounding based on which side has higher yield. Notably, TempleDAO seeded the $1.5M rise of Origami, but the terms of this round were not made public.

The return of the Base Strategy also serves as the performance benchmark for active strategies, establishing the risk-free reference rate against which all deployed capital is measured.

Cosecha Segunda Strategy (CSS)

The Cosecha Segunda Strategy (CSS) acts as the TRV’s strategic investment and incubation arm, focused on vetting and supporting new partners and projects. Because these early-stage investments typically involve vested tokens rather than instant cash, the CSS lacks the immediate liquidity found in other treasury strategies.

To bridge this liquidity gap, governance can approve the redirection of these vested tokens to Temple Gold Auctions within the Spice Bazaar. The CSS Repay Contract acts as the collection point for all $USDS bids generated by these auctions. Once a sufficient balance of $USDS has accumulated, the operator uses these liquid funds to systematically pay down the CSS’s debt to the TRV.

Token Architecture and Value Flows

TempleDAO's economy operates through three tokens, each serving a distinct function within the protocol. Understanding how these tokens interact is essential to evaluating the protocol's sustainability and the incentive alignment of its participants.

$TEMPLE is the protocol's central asset around which the DAO's economic mechanisms are designed. The treasury architecture and governance serve to accrue value for $TEMPLE.

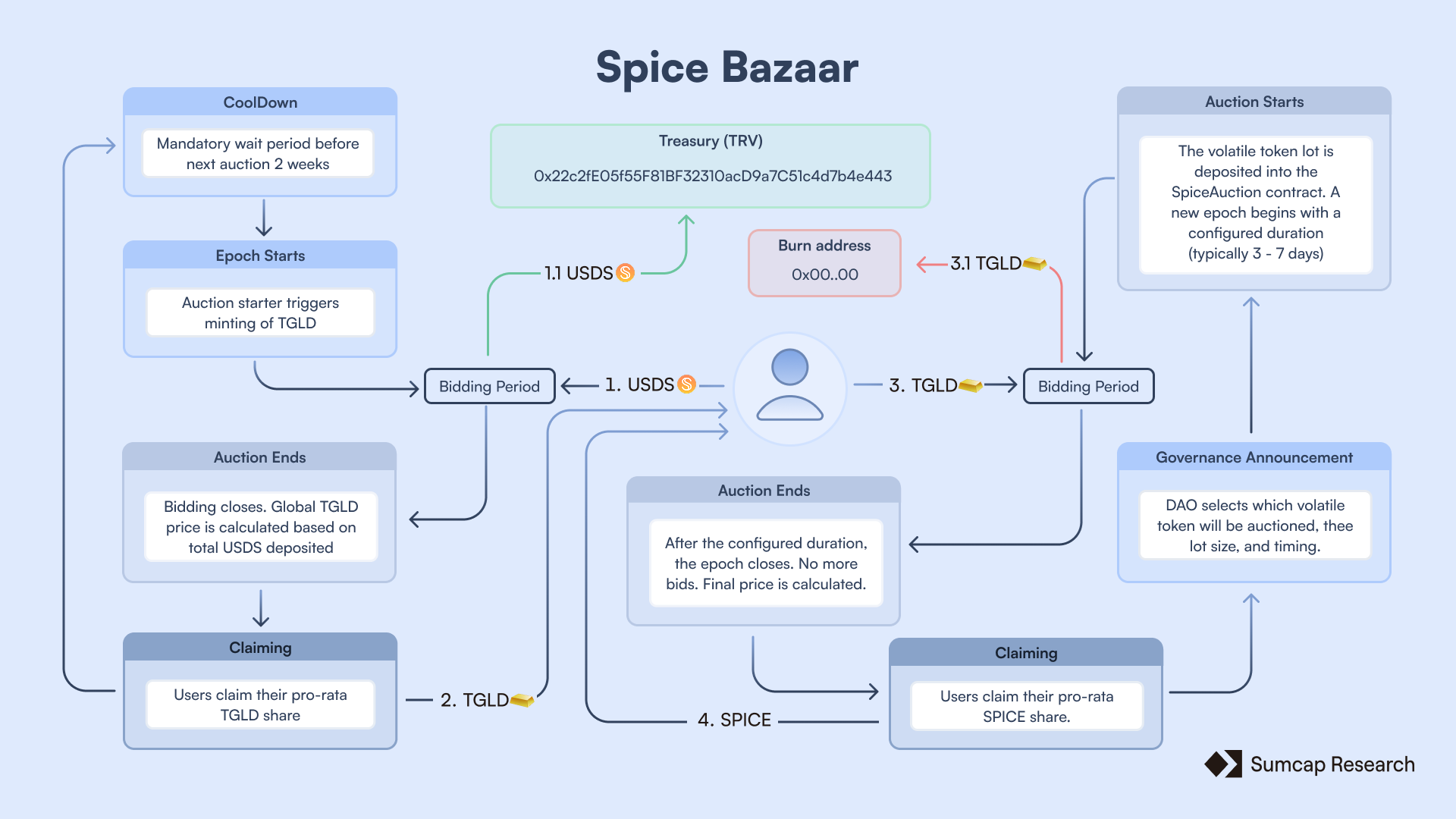

The system architecture builds on this foundation through two core mechanisms. The Spice Bazaar introduces a dual-auction mechanism that converts external stablecoin inflows into internal claim tokens ($TGLD), which are subsequently used to distribute volatile treasury assets (SPICE).

$TEMPLE - The Base Asset

$TEMPLE serves as the foundational asset of the ecosystem with three primary utility vectors.

- As collateral: Temple Line of Credit (TLC), it enables users to borrow $DAI against their holdings at the TPI referenced value, generating interest revenue that flows back to the treasury.

- Staking: When staked, $TEMPLE earns $TGLD emissions, which serve as the internal auction currency for the Spice Bazaar.

- Governance: staked $TEMPLE carries governance weight, used to vote on Temple Improvement Proposals (TIPs).

Treasury Price Index (TPI)

The TPI tracks the stable backing per $TEMPLE and functions as the protocol's internal reference price. Rather than fluctuating with market sentiment, the TPI establishes a floor that appreciates over time as treasury activities generate returns.

The appreciation mechanism works through the "TPI Drip." The Temple Logicians propose a target TPI value and a target date, and the index increases linearly between the current value and the target over the specified timeframe (the same concept as how $OHM's backing price works). The underlying economic driver is the treasury revenue (yield + stablecoin inflows from Gold Auctions + volatile assets not sold through SPICE Auctions). As these revenues are liquidated into stablecoins, the per-token backing rises, which in turn justifies and sustains the TPI's upward trajectory.

The first target was set at $2.15 DAI per $TEMPLE by December 31, 2025. Having surpassed this ahead of schedule, the current target stands at $2.25 $DAI per $TEMPLE by June 30, 2026.

$TGLD - Temple Gold

$TGLD serves as the dedicated rewards and auction token within the ecosystem. It is non-transferable and can only be obtained through two channels: staking $TEMPLE or bidding $USDS in bi-weekly (every two weeks) Gold Auctions. This design ensures that all Spice Bazaar participants must either hold and stake $TEMPLE or contribute with stablecoins to the treasury.

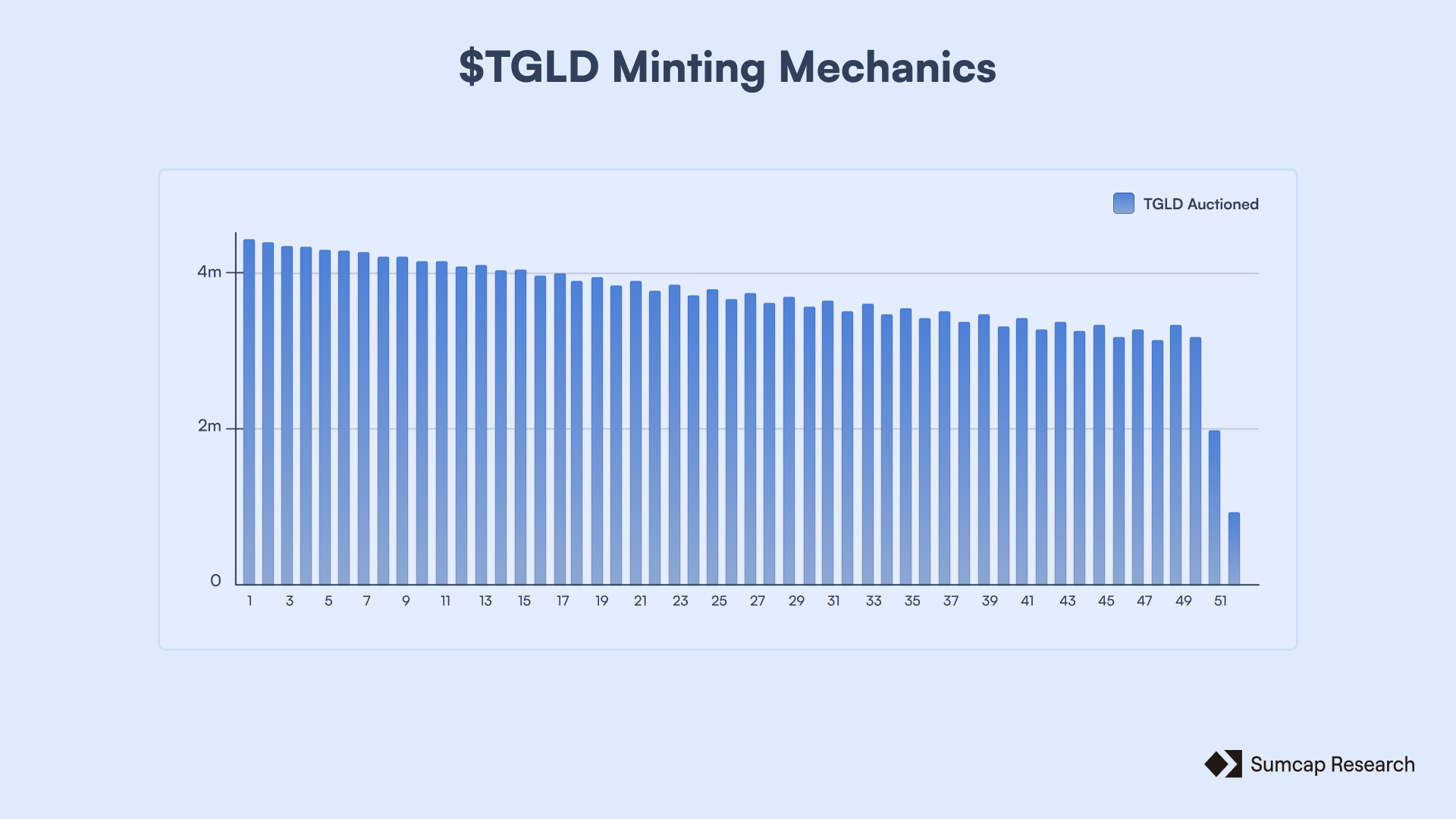

Minting Mechanics

The issuance of $TGLD is managed by a public mint() function, allowing any user to trigger the protocol’s emission schedule. This schedule follows an exponential decay model designed to gradually approach a fixed maximum supply of 1 billion tokens. The amount issued per call is determined by the time elapsed and the remaining unminted supply:

\[

\text{mint()}

= \text{seconds}_{\text{elapsed}}

\times \frac{\text{max}_{\text{supply}} - \text{circ}_{\text{supply}}}

{\text{vestingFactor}}

\]

The vesting factor serves as the protocol's primary "speed limit" for emissions. Effectively, for every week that passes, $1/\text{vestingFactor}$ of the remaining unminted supply becomes available for distribution.

Through governance action in February 2026, the community passed TIP-006, which significantly tightened this emission schedule. By increasing the vesting factor from 156 to 520, the protocol successfully reduced $TGLD emissions by approximately 70%. This shift ensures that while the circulating supply will continue to oscillate toward equilibrium, it now does so at a much more sustainable pace dictated by governance oversight.

When mint() is called, the newly minted $TGLD is allocated according to the following split: 70% to Gold Auction bidders, 15% to staking rewards for $TEMPLE holders, and 15% to a team Gnosis Safe reserved for contributor incentivisation and retention. These allocations are subject to modification by the DAO Multisig.

Obtaining $TGLD

$TGLD is non-transferable and can only be obtained through staking $TEMPLE or bidding $USDS in Gold Auctions.

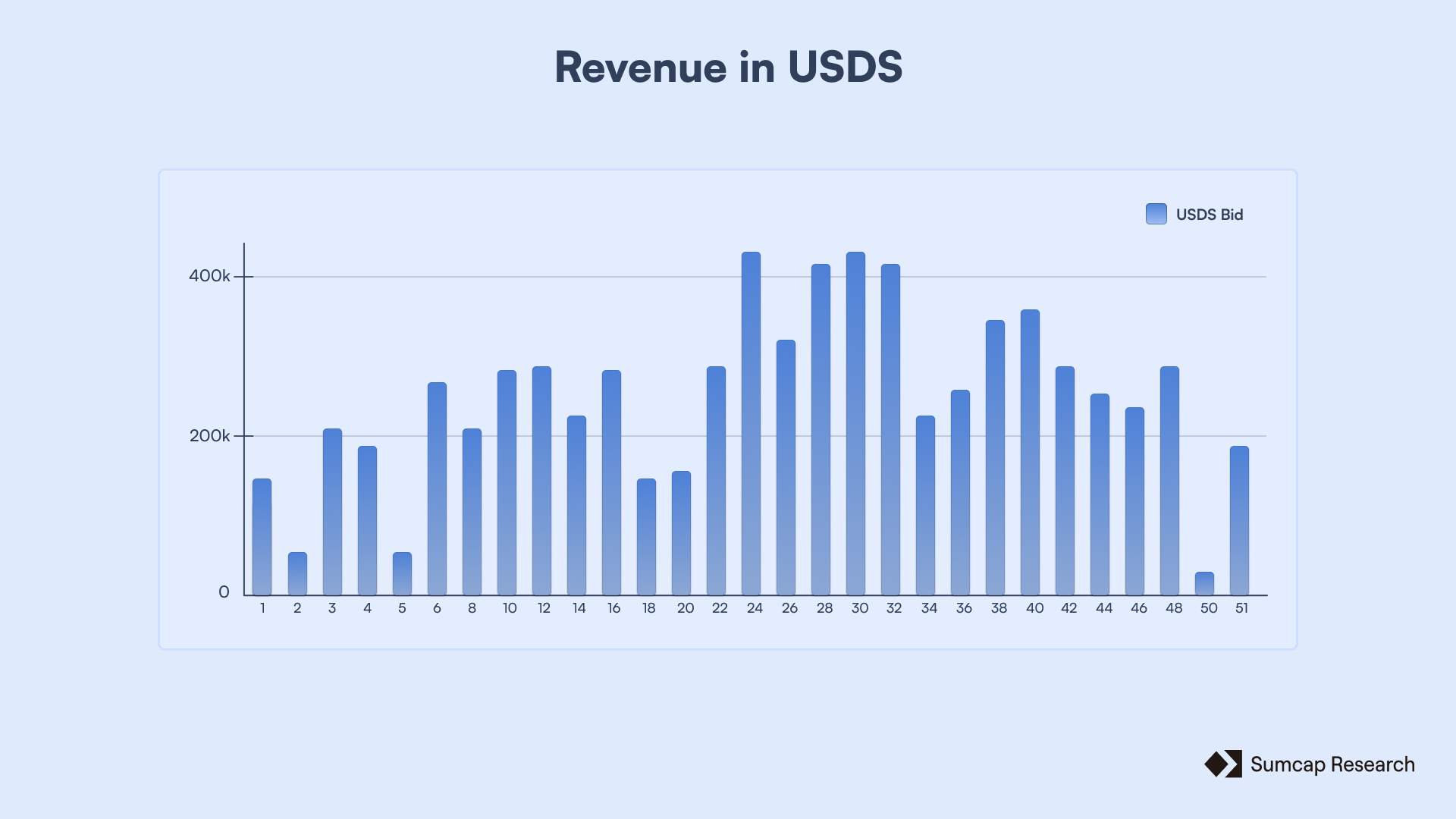

Gold Auctions

Gold Auctions run bi-weekly on Ethereum and operate without a reserve or starting price. The clearing price is determined entirely by the total $USDS submitted by all bidders before the auction closes, and it's the same for everyone.

\[

\text{TGLD}_{\text{price}}

= \frac{\text{Total}_{\text{stable bids}}}

{\text{TGLD}_{\text{sold}}}

\]

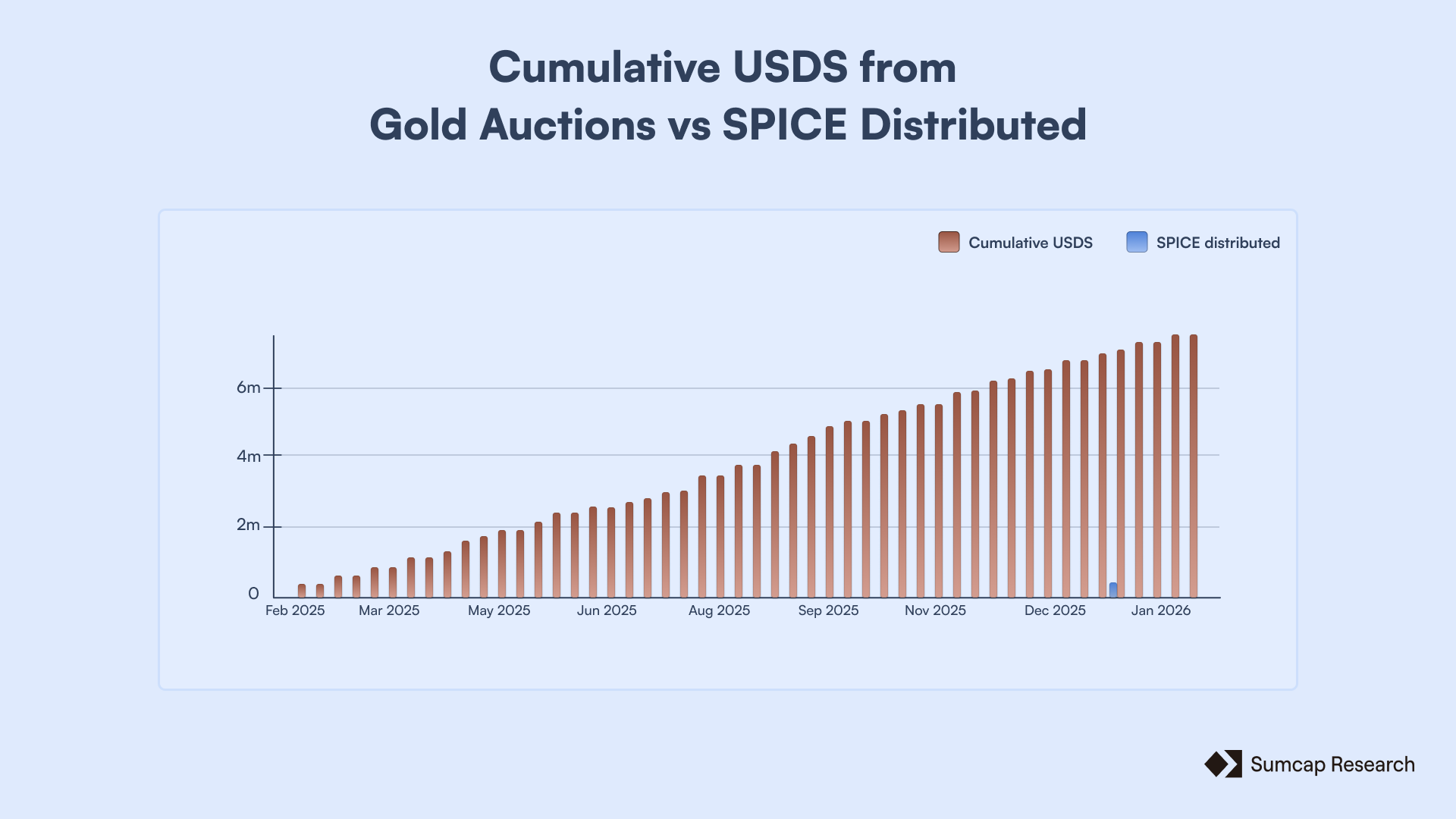

Gold Auctions represent one of the main revenue streams for the treasury. The $USDS collected constitutes direct protocol revenue, and these inflows have stabilised above $200,000 per bi-weekly epoch since mid-2025. This consistency suggests meaningful and persistent demand for Spice Bazaar access, which in turn validates the auction mechanism as a sustainable revenue model.

So far, Temple has generated +$7,500,000 and has only distributed 2,000,000 ENA tokens, worth around $450,000 at the time of distribution, a striking figure for a treasury with less than $50M .

Staking $TEMPLE

Unlike fixed-rate systems, the Staking APR for $TGLD is a floating rate that reacts to the protocol’s circulating supply and the density of $TEMPLE staking. Because $TGLD is emitted based on the remaining unminted supply, the APR naturally rises when the circulating supply is reduced - such as during large $TGLD redemptions in Spice Auctions. Conversely, the yield for individual stakers increases when a larger portion of $TEMPLE remains outside the staking contract, reducing the "pool" among which rewards are shared.

The annual percentage rate at any given epoch is determined by the following formula:

\[

\text{APR}

= \frac{

(\text{max}_{\text{supply}} - \text{circ}_{\text{supply}})

\times 0.15

\times 365

\times 86400

}{

\text{vestingFactor}

\times \text{TEMPLE}_{\text{staked}}

}

\]

This mechanism creates a distinct economic choice for users. While the cost of acquiring $TGLD through staking is typically higher than participating in a Gold Auction, staking allows users to retain their principal $TEMPLE position. In contrast, bidding with $USDS in an auction is a direct expenditure. This distinction became a central point of governance during the proposal to establish staked TEMPLE as the primary governance asset. At that peak in $TGLD$ acquisition costs, the value of the token was tied not just to its market price, but to the influence it represented within the protocol's decision-making framework.

This cost differential creates a natural segmentation between long-term holders (who stake) and active traders (who bid). Recently, the cost of acquisition of 1 $TGLD has risen due to the new governance framework.

SPICE Assets

SPICE is TempleDAO’s designation for volatile tokens that the treasury elects to distribute through Spice Auctions. The tokens typically originate from treasury activity, partner allocations, airdrop farming, vested positions, or pre-TGE deals.

Not every volatile holding is routed through this channel, as some may be allocated to support TPI growth or retained for strategic purposes.

The auction-based distribution offers several advantages over direct market selling, as auctions produce steadier and more predictable cash flows rather than one-off proceeds. Also, auctioning the tokens, they limit immediate price pressure on partner tokens, preserving relationships and alignment. Additionally, they avoid the reputational cost associated with visible market dumps, which can signal a lack of confidence in partner projects.

Spice Auction Mechanics

Spice Auctions accept only $TGLD as payment and depending on the total value of a given token lot, it may be split into multiple smaller epochs to promote broader participation and reduce bid-sniping risk. Each epoch typically lasts three to seven days and all $TGLD bidders receive the same pro-rata price at auction close, and bids are irrevocable once submitted to avoid gaming and strategic bid withdrawal.

For Q1 2026, the announced cadence involves auctioning up to 50% of Ethena $sENA Season 4 tokens across four to six auctions, with the first completed on January 10, 2026.

The Spice Bazaar: Auction-Based Volatility Monetizsation

The Spice Bazaar represents TempleDAO’s most distinctive protocol design. It addresses a challenge common across DeFi treasuries about how to monetise volatile token holdings (from airdrops, vesting schedules, VC investments, and partner allocations) without creating adverse market impact.

The Spice Bazaar creates a value loop across the protocol’s three tokens. External stablecoin inflows enter through Gold Auctions, where bidders exchange $USDS for $TGLD. These stablecoins flow directly into the treasury, strengthening reserves and supporting TPI growth. The $TGLD acquired is then spent in Spice Auctions to purchase volatile assets, and the $TGLD used in these purchases is burned, reducing circulating supply and increasing future staking APRs.

Deprecated Strategies

RAMOS (Automated Liquidity Manager)

RAMOS was TempleDAO’s automated market operations module, designed to keep $TEMPLE trading within a controlled band around TPI by actively managing the TEMPLE/DAI Balancer pool composition. When $TEMPLE traded below TPI, RAMOS withdrew TEMPLE single-sided from the LP and burned the tokens, reducing sell-side liquidity and supporting price recovery. When $TEMPLE traded above TPI, RAMOS added TEMPLE back into the LP to deepen liquidity and reduce volatility, while pulling DAI out of the LP to capture premium as reserve growth.

The rebalancing logic operated on a threshold basis: deviations of more than 1% below TPI triggered periodic rebalances with randomized timing, while deviations exceeding 3% forced immediate rebalances. Per event, RAMOS closed between 50–100% of the gap below TPI and 1–10% of the gap above TPI, reflecting an asymmetric defence posture that prioritised downside protection.

Base DSR

The predecessor to the current Sky Auto Farm base strategy, the Base DSR deposited idle TRV capital into the Dai Savings Rate (sDAI). It served the same benchmark function as the current base strategy, establishing the risk-free reference rate for all deployed capital.

Governance Framework

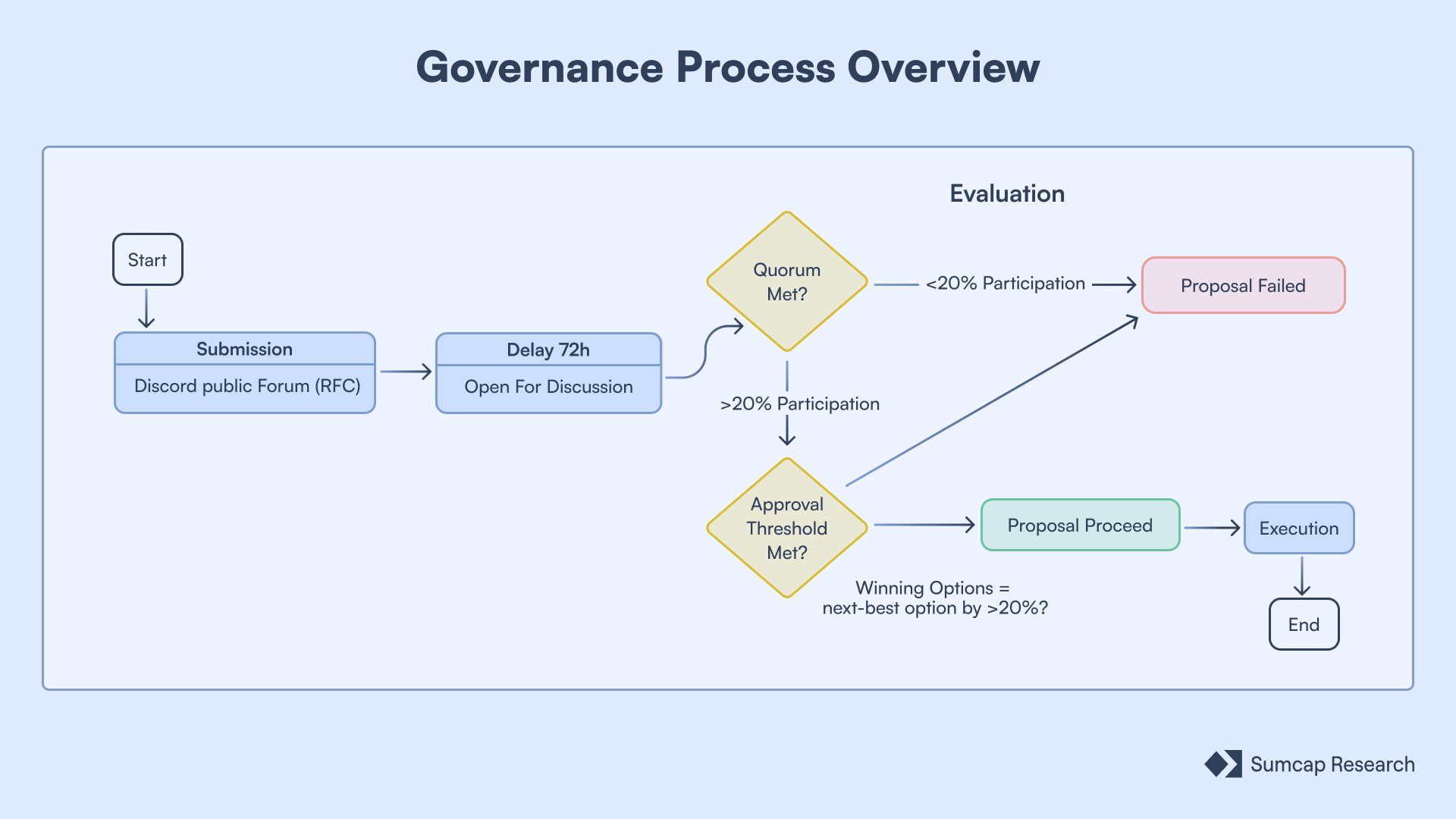

TempleDAO’s governance is undergoing a meaningful transition. Historically, the protocol operated through a Discord role-gated model where participation in governance conversations was mediated by Discord moderation and access roles. While functional, this approach limited participation with token-weighted governance.

Per TIP-001, TempleDAO is transitioning to a model where decision power is tied directly to staked $TEMPLE, making eligibility and influence more accessible. The proposed process requires that any Temple Improvement Proposal (TIP) be preceded by a Request for Comment posted in TempleDAO’s Discord forum, with a minimum 72-hour discussion period.

Voting power is measured at the Snapshot block and is based exclusively on staked $TEMPLE. For a TIP to pass, it must meet two conditions: a quorum of at least 20% of eligible staked TEMPLE participating, and the winning option beating the next-best option by at least 20%. Results can be challenged within a 48-hour window for manifest error or abuse, during which the Foundation may pause implementation.

Conclusions

TempleDAO's benchmark accounting model is, in practice, one of the most rigorous internal capital allocation frameworks operating in DeFi today. Most DeFi treasuries treat deployed capital as working because it generates yield, but TempleDAO treats it as underperforming unless it beats a defined opportunity cost.

Gold Auction revenue has sustained above $200K per bi-weekly epoch since mid-2025, and the dual-auction mechanism itself is one of the more intelligent distribution systems in DeFi treasury design. But the demand for $TGLD is a function of SPICE token quality, and that quality is entirely external. It depends on the treasury's ability to source attractive volatile assets through airdrop farming, partner allocations, and pre-TGE deals. These are fundamentally opportunistic revenue streams that correlate with bull market conditions. If the airdrop meta shifts, the consequences propagate through the entire system. $TGLD demand erodes, Gold Auction inflows contract, stablecoin reserves grow more slowly, and the loop weakens.

TempleDAO has weathered multiple market cycles, and the protocol's survival through successive bear markets speaks to the resilience of the treasury-first design philosophy. The TRV's benchmark accounting, the Spice Bazaar and the governance transition toward token-weighted voting all represent meaningful infrastructure upgrades over the past year. As the treasury scales, the governance surface area expands with it, and the concentration risks identified in this report become harder to manage through multisig discretion alone. The protocol's next phase will likely be defined by how effectively it can diversify strategy exposure, formalize the SPICE sourcing pipeline, and translate its accounting discipline into broader transparency for token holders who currently rely on dashboards that do not fully reflect realized performance.

Inside TempleDAO's Treasury

Most DeFi treasuries have no framework to deploy capital or measure performance. TempleDAO built an on-chain treasury that not only grows by generating yield that grows the price floor of its main asset. Here's the full breakdown.

Treasury Reserve Vault (TRV)

The TRV sits at the center of TempleDAO’s capital allocation architecture. It custody-holds core reserves and functions as an internal lender to approved strategy borrowers. The borrow-and-repay framing creates an accounting model that makes strategies directly comparable against a common benchmark.

TRV Architecture

The TRV is a DAI-based reserve where every loan must be authorised by governance. To protect the protocol, governance assigns each borrower a strict spending limit (debt ceiling). Furthermore, the system uses automated circuit breakers to stop unusually large or suspicious transfers, ensuring that even if a borrower is approved, they cannot accidentally or intentionally drain the treasury.

For a full reference of configurable protocol parameters, contract addresses and signers, see here.

Each treasury strategy is implemented as a whitelisted Strategy Borrower contract that draws capital from the TRV, deploys it into a defined opportunity set, and repays over time. The framework supports two operational models; automated strategies, which operate with deterministic, programmatic execution of borrows and repayments, and manually operated strategies that use a wrapper pattern where the borrower contract serves as the accounting shell while execution is delegated to an operator multisig for discretionary actions. In both cases, treasury capital usage is tracked as debt, and the strategy must eventually return capital through the repayment rail.

When a strategy draws funds, the system mints internal debt-share tokens ($dUSD for stable-denominated loans, $dTEMPLE for TEMPLE-denominated loans) representing principal owed to the TRV. The debt balance accrues at a continuously compounding Treasury Funding Rate:

\[r_{\text{funding}} = r_{\text{benchmark}} + r_{\text{risk premium}} \]

Currently \( r_{\text{risk premium}} = 0 \) for all strategies.

The benchmark rate represents the treasury’s baseline opportunity cost (referenced to the Origami sUSDS+ vault yield), while the risk premium encodes the additional required return for strategy-specific risks. This framework forces every strategy to clear a hurdle rate, meaning that if its producing nominal yield but failing to outperform the benchmark after premium then, in treasury accounting terms, underperforming.

Since all strategies carry a debt ceiling, a persistently underperforming strategy will see its accrued debt grow toward the ceiling. At that point, it must either repay the TRV or face governance action to close or restructure. To date, no strategy has triggered this scenario.

Active Strategies

As of March 2026, the TempleDAO treasury runs multiple strategies whose combined holdings are displayed at ~$130M. However, this figure is misleading as it represents the raw market value of all assets sitting in the strategy wallets without subtracting liabilities.

The net exposure, which strips out borrowed capital and accounts for outstanding debt, sits at roughly $47M. The gap between the two numbers is the clearest indicator of how aggressively the treasury uses leverage across its strategy set.

Templo Mayor (Omnibus Strategy)

Templo Mayor is TempleDAO’s largest and most complex strategy, structured as an Omnibus Strategy operated through a Gnosis Safe multisig. This format is used when full automation is not feasible due to technical or operational constraints. Unlike a single-position automated strategy, Templo Mayor groups multiple related exposures under the same umbrella while maintaining the same debt-tracking and approval framework.

The strategy's dashboard displays holdings of over $103M, but this figure also represents gross exposure:

After subtracting all liabilities, the net exposure is approximately $22M.

The strategy was initially funded with an initial credit line of $24.4M from the TRV and currently maintains roughly $22M in net assets, with an important negative benchmark equity, what suggests that the strategy is not performing as expected.

Temple Line of Credit (TLC)

TLC converts a portion of the treasury’s stablecoin reserves into a risk-managed lending book. The DAO allocates $DAI (notably, this strategy has not migrated to $USDS) as a borrowable asset against $TEMPLE. Collateral valuation is anchored to the Treasury Price Index (TPI) rather than spot market price, providing borrowers with more stable and predictable terms. More to follow on the TPI below. Since inception it, has generated $1.05M in excess returns over the benchmark rate, with $14.32M in total repayments and $185.29K in accrued interest. The strategy currently holds $16.94M with a benchmarked equity of $1.05M, confirming consistent performance above the hurdle rate.

Borrowers can draw up to 85% loan-to-value (LTV), with liquidation triggered at 90% LTV. The borrow rate is periodically recalibrated using the formula:

\[ \text{Borrow}_{\text{rate}} = \text{sDAI} _{\text{rate}} \times \max(1.1, 1 + \text{TEMPLE}_{\text{staked}}\%) \]

With the above expression, Temple ensures that this strategy will always outperform the DAI Savings Rate by at least 10%. Currently, this benchmark reflects a yield of 1.25% for sDAI, though it is important to note the wider yield environment: the Sky Savings Rate (SSR) for USDS is providing a higher baseline of 3.75%. This follows a recent 25bps reduction from its previous 4% target, which was implemented on March 9, 2026.

FOHMO

FOHMO maintains a maximally looped $OHM position based on Cooler loans, using Origami hOHM as the execution vehicle. This strategy has had a really good performance thanks to the good timing that TempleDAO had with the repayments to the TRV.

The total value of holdings ($8.86M) reflects only the gross value still sitting inside FOHMO today. It does not capture value that has already been realised and returned to the treasury through repayments ($8.19M total). Additionally, the strategy currently shows 0% debt ceiling utilisation, indicating no open debt position. The benchmarked equity stands at $13.97M, representing pure profit after accounting for all capital costs.

Base Sky Autofarm

Idle capital in the TRV is automatically directed to a Base Strategy to earn yield (i.e., $USDS received from Temple Gold Auctions). The current implementation of the Base Strategy deposits idle capital into the Sky Auto Farm through Origami sUSDS+ which deploys $SUSDS choosing the most optimal farm between vanilla $USDS staking and farming $SKY with auto-compounding based on which side has higher yield. Notably, TempleDAO seeded the $1.5M rise of Origami, but the terms of this round were not made public.

The return of the Base Strategy also serves as the performance benchmark for active strategies, establishing the risk-free reference rate against which all deployed capital is measured.

Cosecha Segunda Strategy (CSS)

The Cosecha Segunda Strategy (CSS) acts as the TRV’s strategic investment and incubation arm, focused on vetting and supporting new partners and projects. Because these early-stage investments typically involve vested tokens rather than instant cash, the CSS lacks the immediate liquidity found in other treasury strategies.

To bridge this liquidity gap, governance can approve the redirection of these vested tokens to Temple Gold Auctions within the Spice Bazaar. The CSS Repay Contract acts as the collection point for all $USDS bids generated by these auctions. Once a sufficient balance of $USDS has accumulated, the operator uses these liquid funds to systematically pay down the CSS’s debt to the TRV.

Token Architecture and Value Flows

TempleDAO's economy operates through three tokens, each serving a distinct function within the protocol. Understanding how these tokens interact is essential to evaluating the protocol's sustainability and the incentive alignment of its participants.

$TEMPLE is the protocol's central asset around which the DAO's economic mechanisms are designed. The treasury architecture and governance serve to accrue value for $TEMPLE.

The system architecture builds on this foundation through two core mechanisms. The Spice Bazaar introduces a dual-auction mechanism that converts external stablecoin inflows into internal claim tokens ($TGLD), which are subsequently used to distribute volatile treasury assets (SPICE).

$TEMPLE - The Base Asset

$TEMPLE serves as the foundational asset of the ecosystem with three primary utility vectors.

- As collateral: Temple Line of Credit (TLC), it enables users to borrow $DAI against their holdings at the TPI referenced value, generating interest revenue that flows back to the treasury.

- Staking: When staked, $TEMPLE earns $TGLD emissions, which serve as the internal auction currency for the Spice Bazaar.

- Governance: staked $TEMPLE carries governance weight, used to vote on Temple Improvement Proposals (TIPs).

Treasury Price Index (TPI)

The TPI tracks the stable backing per $TEMPLE and functions as the protocol's internal reference price. Rather than fluctuating with market sentiment, the TPI establishes a floor that appreciates over time as treasury activities generate returns.

The appreciation mechanism works through the "TPI Drip." The Temple Logicians propose a target TPI value and a target date, and the index increases linearly between the current value and the target over the specified timeframe (the same concept as how $OHM's backing price works). The underlying economic driver is the treasury revenue (yield + stablecoin inflows from Gold Auctions + volatile assets not sold through SPICE Auctions). As these revenues are liquidated into stablecoins, the per-token backing rises, which in turn justifies and sustains the TPI's upward trajectory.

The first target was set at $2.15 DAI per $TEMPLE by December 31, 2025. Having surpassed this ahead of schedule, the current target stands at $2.25 $DAI per $TEMPLE by June 30, 2026.

$TGLD - Temple Gold

$TGLD serves as the dedicated rewards and auction token within the ecosystem. It is non-transferable and can only be obtained through two channels: staking $TEMPLE or bidding $USDS in bi-weekly (every two weeks) Gold Auctions. This design ensures that all Spice Bazaar participants must either hold and stake $TEMPLE or contribute with stablecoins to the treasury.

Minting Mechanics

The issuance of $TGLD is managed by a public mint() function, allowing any user to trigger the protocol’s emission schedule. This schedule follows an exponential decay model designed to gradually approach a fixed maximum supply of 1 billion tokens. The amount issued per call is determined by the time elapsed and the remaining unminted supply:

\[

\text{mint()}

= \text{seconds}_{\text{elapsed}}

\times \frac{\text{max}_{\text{supply}} - \text{circ}_{\text{supply}}}

{\text{vestingFactor}}

\]

The vesting factor serves as the protocol's primary "speed limit" for emissions. Effectively, for every week that passes, $1/\text{vestingFactor}$ of the remaining unminted supply becomes available for distribution.

Through governance action in February 2026, the community passed TIP-006, which significantly tightened this emission schedule. By increasing the vesting factor from 156 to 520, the protocol successfully reduced $TGLD emissions by approximately 70%. This shift ensures that while the circulating supply will continue to oscillate toward equilibrium, it now does so at a much more sustainable pace dictated by governance oversight.

When mint() is called, the newly minted $TGLD is allocated according to the following split: 70% to Gold Auction bidders, 15% to staking rewards for $TEMPLE holders, and 15% to a team Gnosis Safe reserved for contributor incentivisation and retention. These allocations are subject to modification by the DAO Multisig.

Obtaining $TGLD

$TGLD is non-transferable and can only be obtained through staking $TEMPLE or bidding $USDS in Gold Auctions.

Gold Auctions

Gold Auctions run bi-weekly on Ethereum and operate without a reserve or starting price. The clearing price is determined entirely by the total $USDS submitted by all bidders before the auction closes, and it's the same for everyone.

\[

\text{TGLD}_{\text{price}}

= \frac{\text{Total}_{\text{stable bids}}}

{\text{TGLD}_{\text{sold}}}

\]

Gold Auctions represent one of the main revenue streams for the treasury. The $USDS collected constitutes direct protocol revenue, and these inflows have stabilised above $200,000 per bi-weekly epoch since mid-2025. This consistency suggests meaningful and persistent demand for Spice Bazaar access, which in turn validates the auction mechanism as a sustainable revenue model.

So far, Temple has generated +$7,500,000 and has only distributed 2,000,000 ENA tokens, worth around $450,000 at the time of distribution, a striking figure for a treasury with less than $50M .

Staking $TEMPLE

Unlike fixed-rate systems, the Staking APR for $TGLD is a floating rate that reacts to the protocol’s circulating supply and the density of $TEMPLE staking. Because $TGLD is emitted based on the remaining unminted supply, the APR naturally rises when the circulating supply is reduced - such as during large $TGLD redemptions in Spice Auctions. Conversely, the yield for individual stakers increases when a larger portion of $TEMPLE remains outside the staking contract, reducing the "pool" among which rewards are shared.

The annual percentage rate at any given epoch is determined by the following formula:

\[

\text{APR}

= \frac{

(\text{max}_{\text{supply}} - \text{circ}_{\text{supply}})

\times 0.15

\times 365

\times 86400

}{

\text{vestingFactor}

\times \text{TEMPLE}_{\text{staked}}

}

\]

This mechanism creates a distinct economic choice for users. While the cost of acquiring $TGLD through staking is typically higher than participating in a Gold Auction, staking allows users to retain their principal $TEMPLE position. In contrast, bidding with $USDS in an auction is a direct expenditure. This distinction became a central point of governance during the proposal to establish staked TEMPLE as the primary governance asset. At that peak in $TGLD$ acquisition costs, the value of the token was tied not just to its market price, but to the influence it represented within the protocol's decision-making framework.

This cost differential creates a natural segmentation between long-term holders (who stake) and active traders (who bid). Recently, the cost of acquisition of 1 $TGLD has risen due to the new governance framework.

SPICE Assets

SPICE is TempleDAO’s designation for volatile tokens that the treasury elects to distribute through Spice Auctions. The tokens typically originate from treasury activity, partner allocations, airdrop farming, vested positions, or pre-TGE deals.

Not every volatile holding is routed through this channel, as some may be allocated to support TPI growth or retained for strategic purposes.

The auction-based distribution offers several advantages over direct market selling, as auctions produce steadier and more predictable cash flows rather than one-off proceeds. Also, auctioning the tokens, they limit immediate price pressure on partner tokens, preserving relationships and alignment. Additionally, they avoid the reputational cost associated with visible market dumps, which can signal a lack of confidence in partner projects.

Spice Auction Mechanics

Spice Auctions accept only $TGLD as payment and depending on the total value of a given token lot, it may be split into multiple smaller epochs to promote broader participation and reduce bid-sniping risk. Each epoch typically lasts three to seven days and all $TGLD bidders receive the same pro-rata price at auction close, and bids are irrevocable once submitted to avoid gaming and strategic bid withdrawal.

For Q1 2026, the announced cadence involves auctioning up to 50% of Ethena $sENA Season 4 tokens across four to six auctions, with the first completed on January 10, 2026.

The Spice Bazaar: Auction-Based Volatility Monetizsation

The Spice Bazaar represents TempleDAO’s most distinctive protocol design. It addresses a challenge common across DeFi treasuries about how to monetise volatile token holdings (from airdrops, vesting schedules, VC investments, and partner allocations) without creating adverse market impact.

The Spice Bazaar creates a value loop across the protocol’s three tokens. External stablecoin inflows enter through Gold Auctions, where bidders exchange $USDS for $TGLD. These stablecoins flow directly into the treasury, strengthening reserves and supporting TPI growth. The $TGLD acquired is then spent in Spice Auctions to purchase volatile assets, and the $TGLD used in these purchases is burned, reducing circulating supply and increasing future staking APRs.

Deprecated Strategies

RAMOS (Automated Liquidity Manager)

RAMOS was TempleDAO’s automated market operations module, designed to keep $TEMPLE trading within a controlled band around TPI by actively managing the TEMPLE/DAI Balancer pool composition. When $TEMPLE traded below TPI, RAMOS withdrew TEMPLE single-sided from the LP and burned the tokens, reducing sell-side liquidity and supporting price recovery. When $TEMPLE traded above TPI, RAMOS added TEMPLE back into the LP to deepen liquidity and reduce volatility, while pulling DAI out of the LP to capture premium as reserve growth.

The rebalancing logic operated on a threshold basis: deviations of more than 1% below TPI triggered periodic rebalances with randomized timing, while deviations exceeding 3% forced immediate rebalances. Per event, RAMOS closed between 50–100% of the gap below TPI and 1–10% of the gap above TPI, reflecting an asymmetric defence posture that prioritised downside protection.

Base DSR

The predecessor to the current Sky Auto Farm base strategy, the Base DSR deposited idle TRV capital into the Dai Savings Rate (sDAI). It served the same benchmark function as the current base strategy, establishing the risk-free reference rate for all deployed capital.

Governance Framework

TempleDAO’s governance is undergoing a meaningful transition. Historically, the protocol operated through a Discord role-gated model where participation in governance conversations was mediated by Discord moderation and access roles. While functional, this approach limited participation with token-weighted governance.

Per TIP-001, TempleDAO is transitioning to a model where decision power is tied directly to staked $TEMPLE, making eligibility and influence more accessible. The proposed process requires that any Temple Improvement Proposal (TIP) be preceded by a Request for Comment posted in TempleDAO’s Discord forum, with a minimum 72-hour discussion period.

Voting power is measured at the Snapshot block and is based exclusively on staked $TEMPLE. For a TIP to pass, it must meet two conditions: a quorum of at least 20% of eligible staked TEMPLE participating, and the winning option beating the next-best option by at least 20%. Results can be challenged within a 48-hour window for manifest error or abuse, during which the Foundation may pause implementation.

Conclusions

TempleDAO's benchmark accounting model is, in practice, one of the most rigorous internal capital allocation frameworks operating in DeFi today. Most DeFi treasuries treat deployed capital as working because it generates yield, but TempleDAO treats it as underperforming unless it beats a defined opportunity cost.

Gold Auction revenue has sustained above $200K per bi-weekly epoch since mid-2025, and the dual-auction mechanism itself is one of the more intelligent distribution systems in DeFi treasury design. But the demand for $TGLD is a function of SPICE token quality, and that quality is entirely external. It depends on the treasury's ability to source attractive volatile assets through airdrop farming, partner allocations, and pre-TGE deals. These are fundamentally opportunistic revenue streams that correlate with bull market conditions. If the airdrop meta shifts, the consequences propagate through the entire system. $TGLD demand erodes, Gold Auction inflows contract, stablecoin reserves grow more slowly, and the loop weakens.

TempleDAO has weathered multiple market cycles, and the protocol's survival through successive bear markets speaks to the resilience of the treasury-first design philosophy. The TRV's benchmark accounting, the Spice Bazaar and the governance transition toward token-weighted voting all represent meaningful infrastructure upgrades over the past year. As the treasury scales, the governance surface area expands with it, and the concentration risks identified in this report become harder to manage through multisig discretion alone. The protocol's next phase will likely be defined by how effectively it can diversify strategy exposure, formalize the SPICE sourcing pipeline, and translate its accounting discipline into broader transparency for token holders who currently rely on dashboards that do not fully reflect realized performance.

.svg)