Tranching in DeFi

DeFi tranching separates one yield stream into senior and junior risk-return profiles. This article compares product-native and service-based models, covering yield sources, waterfalls, redemption gates, reserve funds, collateral use and how tranche tokens reshape risk across DeFi ecosystems.

DeFi doesn't have a yield problem, it has a risk problem. All the yield sources exist, but they force everyone into the same position without risk segregation. Tranching fixes this by letting protocols separate who gets paid first from who gets paid most, so that both sides get a product that matches their risk appetite.

1. Introduction

1.1 What is tranching in DeFi

Tranching is the segmentation of a single yield stream into instruments with distinct risk-return profiles. A senior tranche receives priority on cash flows with loss protection in exchange for capped upside, while a junior tranche absorbs first losses and captures the residuals, the excess yield that remains after the senior obligations are met.

The concept is borrowed directly from structured credit in traditional finance, where CLOs and CDOs slice loan portfolios into rated tranches with sequential payment waterfalls. In DeFi, the same logic applies but the yield sources, mechanisms, and liquidity dynamics are different.

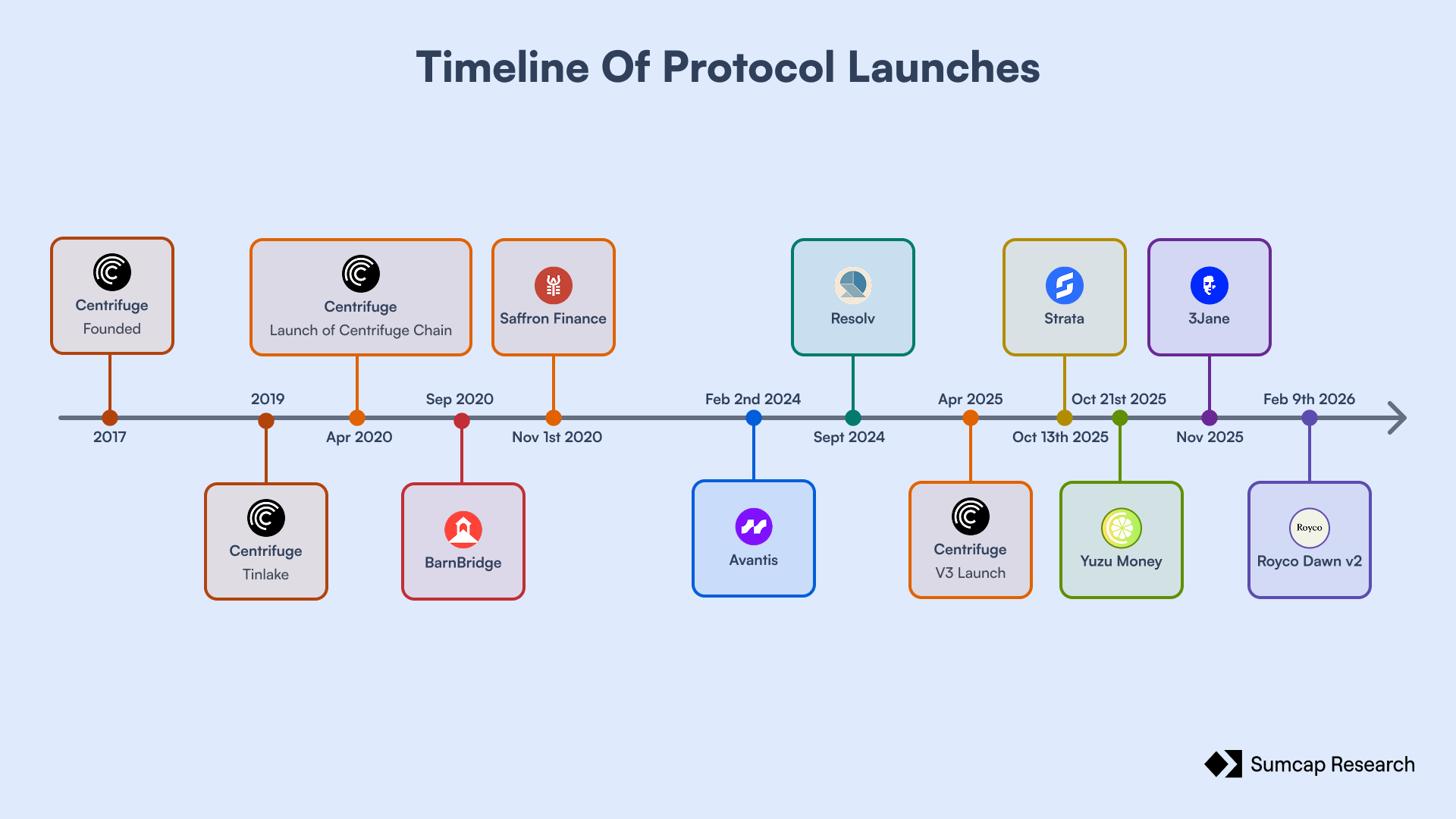

BarnBridge and Saffron Finance were the first to bring tranches on-chain in 2020, wrapping Compound and Aave lending rates into fixed-rate senior bonds and leveraged-yield junior positions. Both protocols proved the concept but struggled with sustainability as yield depended on token emissions, and demand imbalances between tranches made the economics fragile. They demonstrated that tranching had demand on-chain attracting hundreds of millions in TVL in a short period, but left open the question of whether it could economically work without subsidies.

Today, protocols like Resolv, Yuzu, Strata, Royco and 3Jane (among others), have revisited the problem with more diverse yield sources, more sophisticated loss absorption mechanisms, and different design philosophies.

1.2 Two paradigms

These newer protocols split into two distinct approaches.

The first is tranching as a product: this category includes protocols like Resolv, Avant, Yuzu, and 3Jane that generate their own yield through basis & carry trades, multi-strategies, or unsecured credit to build senior/junior tranches natively around that yield engine. This means the protocol controls how yield is generated, how it flows between tranches, how losses are absorbed, and under what conditions users can exit.

The second is tranching as a service: where platforms such as Strata, Royco Dawn, and Centrifuge don't generate yield themselves. Instead, they use the underlyings’ yield source such as an ERC-4626 vault or a tokenized credit pool, and split it into tranches. They present the infrastructure, the risk of the underlying strategy belongs entirely to whoever deployed it, not at the tranche layer. The platform defines the rules for splitting yield and absorbing losses, but it has no control over whether the underlying vault suffers a drawdown, a depeg, or a liquidity crisis.

This distinction shapes how yield is distributed, where losses land and what happens when tranche tokens start circulating as collateral in other protocols.

Part I: Tranching as a Product

In this first part we examine protocols that generate their own yield and build tranches natively around it. These protocols own the full vertical, from strategy execution to loss absorption, and their tranche design is inseparable from the yield engine underneath.

2. Yield Sources

The yield source is what defines the risk segregation. In protocols that build tranches in-house, the yield engine is proprietary and the protocol is directly responsible for its performance. This section covers the yield sources behind product-native tranching protocols, from the earliest lending market wrappers to the market-neutral strategies operating today.

2.1 Lending market wrappers

The first generation of DeFi tranching protocols did not generate yield on their own. BarnBridge and Saffron Finance both captured the variable interest flowing from lending markets (Compound and Aave), and redistributed it according to their own tranche rules.

User deposits were routed into lending protocols, and the resulting variable rate was split between a senior position that received a fixed or priority return and a junior position that absorbed the volatility.

In BarnBridge, the senior received a fixed rate derived from a 3d MA of the underlying protocol's APY. In Saffron, the junior received a leveraged multiplier (default 10x) on their share of pool interest, funded by the yield that senior depositors gave up and the seniors received practically only $SFI incentives.

Both protocols relied heavily on governance token rewards ($COMP, $AAVE) as yield source. These rewards were harvested, sold for the base asset, and reinjected into the pool as an additional yield source. This dependency meant that the economics of the tranches were completely tied to the price of tokens that the protocol did not control, making the yield profile fragile when emissions declined or token prices dropped.

2.2 Delta-neutral and market-neutral strategies

The current generation moved away from wrapping lending rates and relaying token emissions to build yield engines around market-neutral positioning.

Resolv generates yield through a delta-neutral basis trade. The protocol holds spot positions in ETH and BTC alongside short perpetual futures, capturing the funding rate differential while remaining neutral. This strategy is complemented by DeFi deployments of stablecoin reserves and a smaller allocation to tokenized RWA assets (AAA-rated CLOs via Centrifuge). The portfolio is designed to produce consistent yield without taking directional market exposure.

Avant operates through an actively managed multi-strategy framework organized around three independent markets which are USD, BTC, and ETH. Each market has its own strategy and deploys capital into a distinct basket of strategies that include basis trades, money market carry trades, and yield trading. This means the yield profile, risk exposure, and performance of each market are independent from one another.

Yuzu generates yield by running leveraged stablecoin loops, stablecoin arbitrages, CLOs and other strategies. These strategies have no directional exposure (Δ = 0), but they carry meaningful leverage mitigated by the use of fundamental oracles on money markets.

What connects these three is that none of them rely on token emissions or governance rewards as a primary yield source. The yield is structural, coming from native DeFi strategies and organic market conditions. This makes them more self-sustaining than their first-generation predecessors.

2.3 Unsecured credit

Instead of capturing on-chain lending rates or running market-neutral trades, 3Jane generate yield from unsecured USDC credit lines issued to borrowers who do not post on-chain collateral at the time of borrowing.

To open a credit line, a borrower connects their wallet, links a bank account, and submits zkTLS proofs of creditworthiness from sources including DeFi positions, centralized exchange balances, bank cash flows, and traditional credit scores. Based on this data, the protocol's 3CA algorithm assigns a credit line size, a default risk premium, and a repayment schedule. The yield that depositors earn comes directly from the interest charged on these credit lines.

This makes 3Jane's yield source closer to what a traditional prime brokerage or consumer lending platform would generate than anything else in the DeFi tranching space. The return is a function of credit spreads. The quality of that return depends entirely on how well the underwriting model estimates default probability and loss severity, which is a very different risk profile from basis trades or leveraged loops.

3. Tranche Architecture

Once a protocol has a yield source, the next design decision is how to structure the tranches around it. How many tranches, what role each one plays, and which mechanisms absorb losses beyond the junior position.

3.1 Two-tranche and three-tranche models

The majority of protocols chooses to tranche the assets in a two-tranche model, a senior position with priority on cash flows and loss protection paired with a junior position that absorbs first losses and captures residual yield. Most protocols covered in this piece follow this structure, whether they implement it as two distinct vaults, two ERC-4626 tokens, or a base-staked design.

Some protocols have experimented with three tranches.

Saffron Finance introduced a super-senior (\(AA\)), junior (\(A\)), and balancing (\(S\)) tranche, where the \(S\) tranche dynamically absorbed the imbalance between senior and junior demand to keep the yield multiplier consistent. Since organic deposits rarely arrived in that perfect ratio (\(\frac{AA}{A}=10\)), the \(S\) tranche existed to absorb the imbalance. It split itself internally into "utilised" capital, which actively backed the multiplier and earned the residual yield, and "unutilized" capital, which sat idle and earned no interest at all (if \(S > 10 \times A\) then not all capital of \(S\) could be deployed to \(AA\) because it wouldn't satisfy the ratio \(\frac{AA}{A}=10\)).

.png)

Actually, the only way to get into (\(AA\)) tranche was through the (\(S\)) tranche, as direct deposits into it were not possible, this made S tranche to end up performing both as the senior and balancing roles simultaneously, which made the system harder to reason about without adding economic differentiation.

Mezzanine aims to take a different approach with three explicitly layered tranches, this protocol will have a senior ($smzUSD), a mezzanine liquidity tranche (MLT) designed for DeFi composability, and a junior (JLT) that takes first-loss exposure. The protocol has not yet launched, so the real-world dynamics of this three-layer structure remain to be tested.

In both cases, the added complexity of a third tranche introduces questions about whether the intermediate layer occupies a distinct risk-return niche or simply fragments liquidity without creating a meaningfully different product for users.

3.2 Base token + staked tranche designs

Several current protocols share a design that differs from the classic senior/junior split. Instead of offering two separate deposit entry points, they start with a base token that represents a 1:1 claim on the underlying asset and then layer tranched exposure through staking derivatives on top of it.

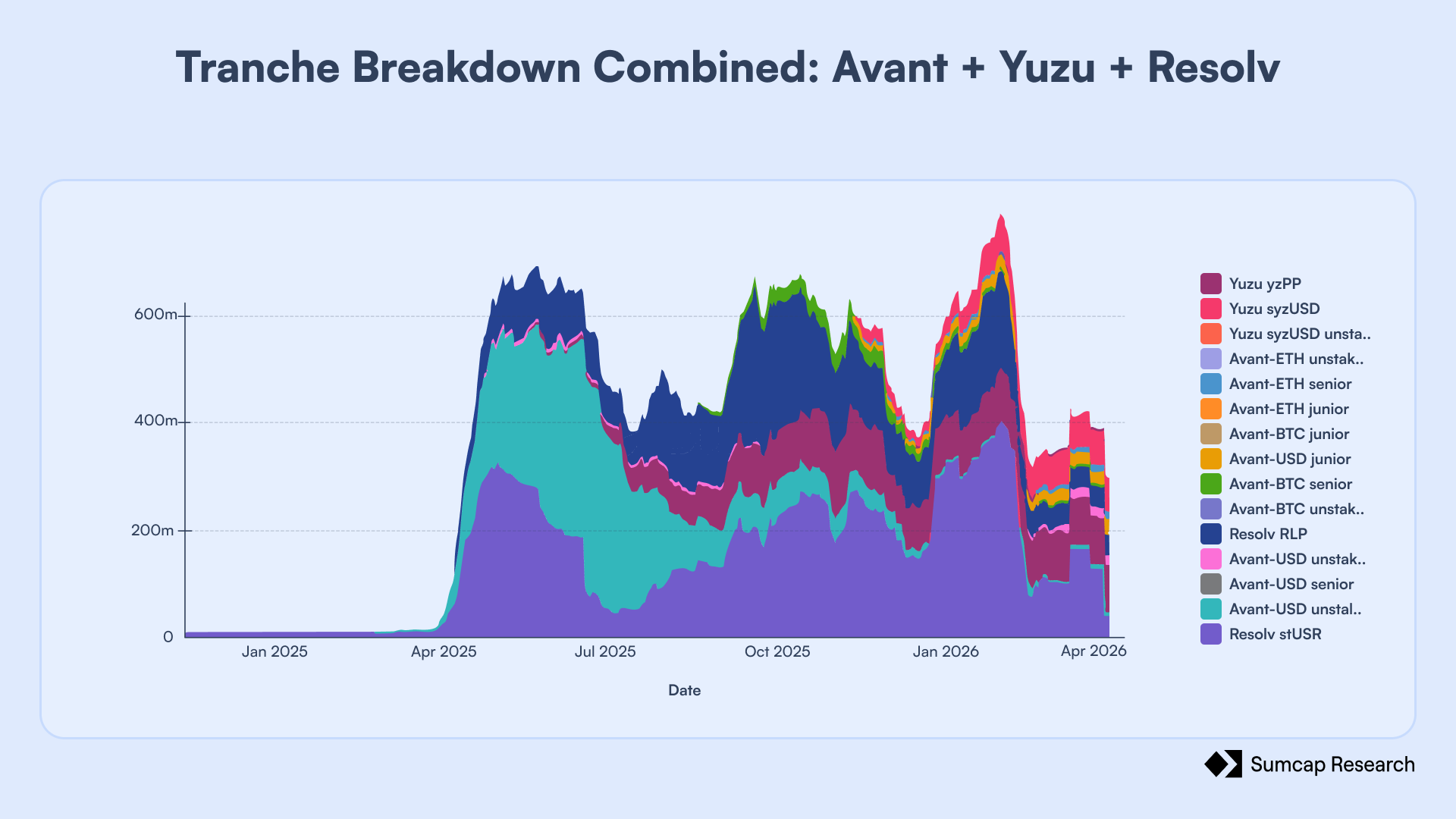

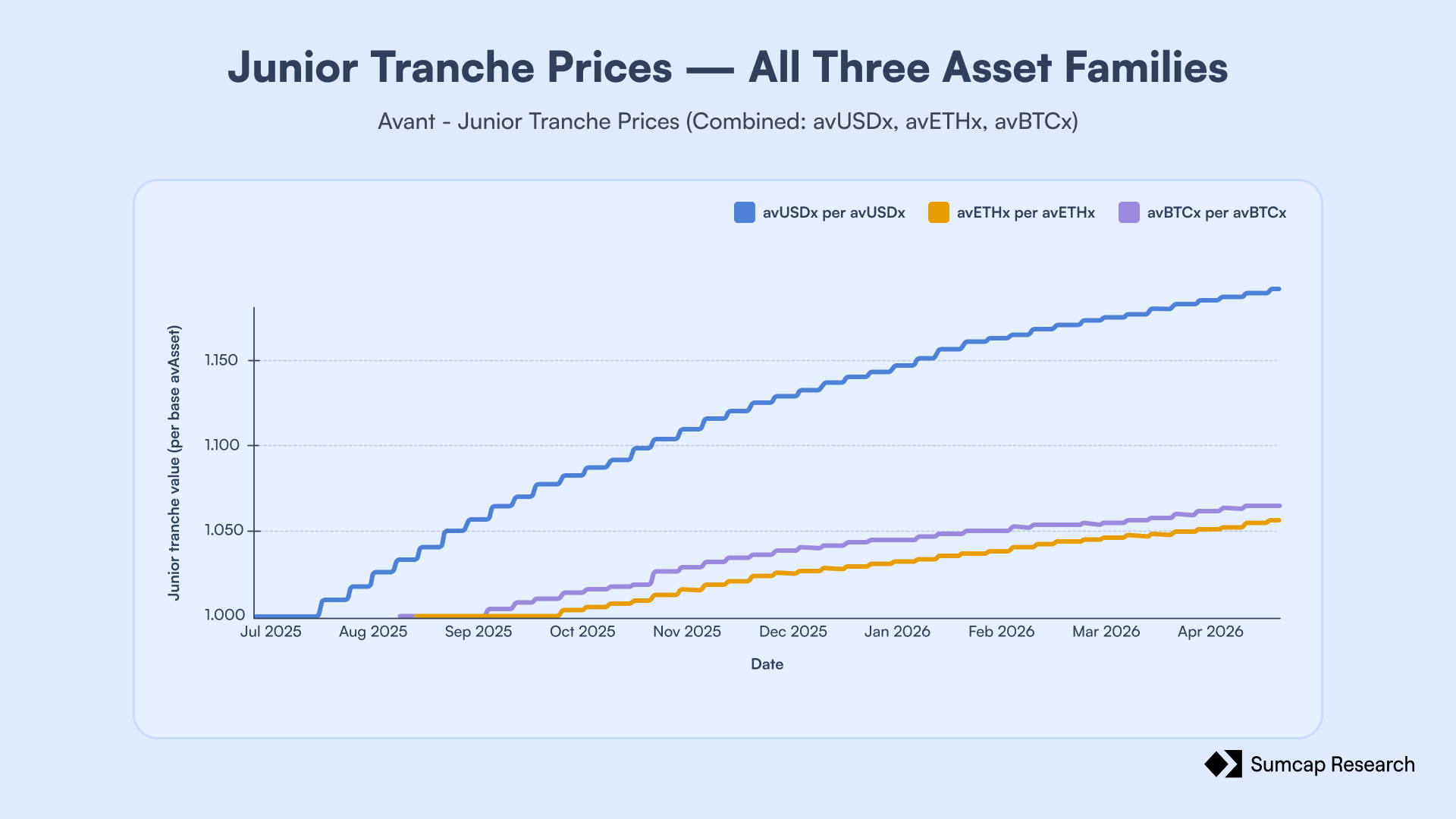

Resolv issues USR as its base stablecoin, which can then be staked into $stUSR (senior yield exposure) or users can separately mint $RLP (the junior first-loss token). Avant mints avAsset ($avUSD, $avBTC, $avETH) at a 1:1 ratio to the underlying and then offers savAsset as the senior tranche and avAssetX as the junior. Yuzu follows a similar logic with $yzUSD as the senior , $syzUSD as the staked variant for yield (an ERC-4626 wrapper), and $yzPP as the junior.

What makes this pattern distinct from a simple two-vault senior/junior is that it introduces the base token holder who has neither senior yield priority nor junior first-loss exposure, but whose capital is nonetheless part of the system.

3.3 Reserve funds and insurance layers

Every tranching protocol needs a mechanism for what happens when yield falls short or losses materialize. The junior tranche is usually the first layer of absorption, but some protocols incorporate a reserve fund or an insurance layer to protect even more their depositors.

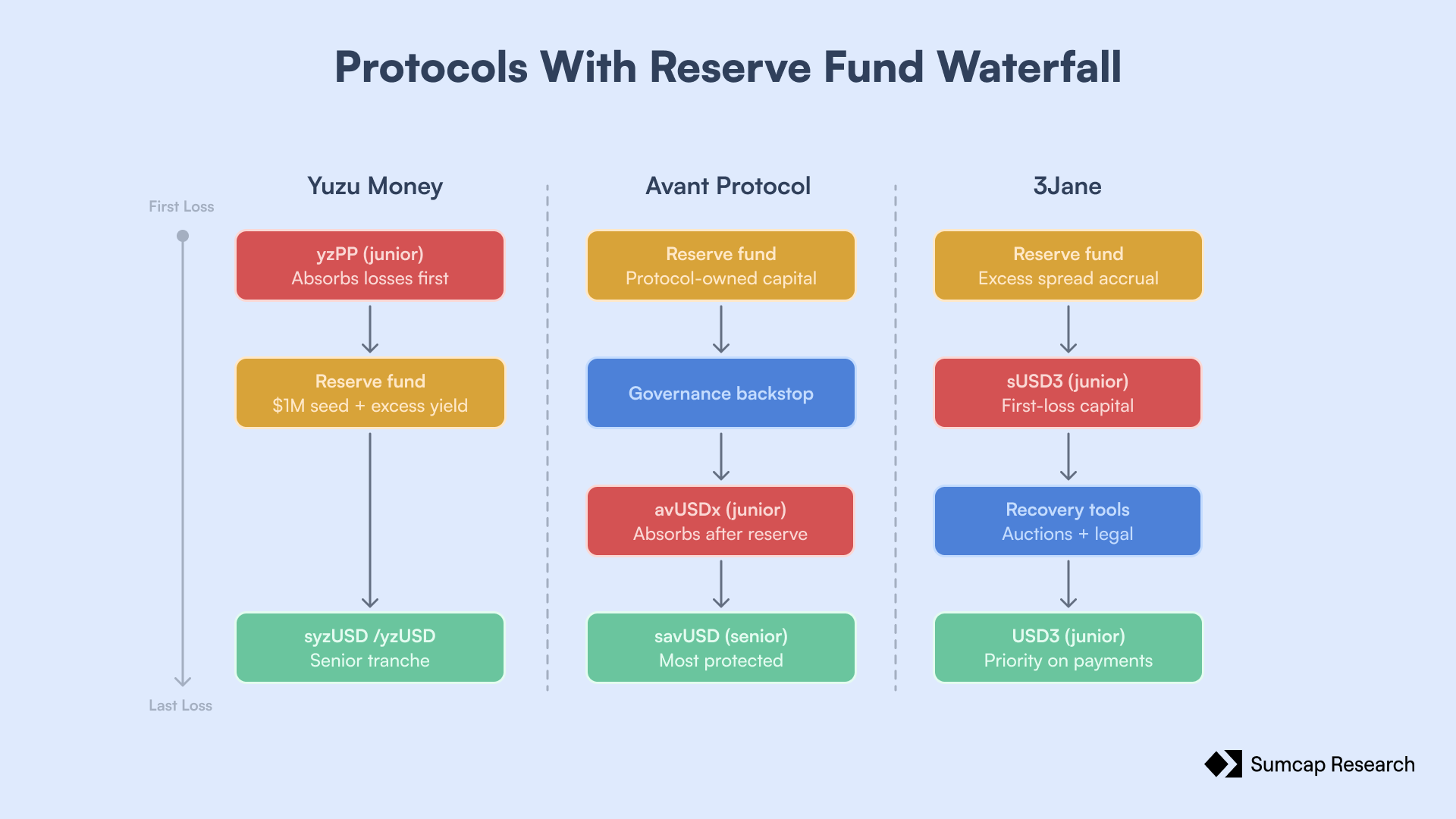

3Jane has the most layered loss architecture. The waterfall flows through an insurance fund, then through the junior tranche ($sUSD3), and only if both are exhausted does the senior ($USD3) take a hit. The reserve fund grows organically through a "Reserve Accrual" mechanism, whereby a portion of the excess spread between borrower interest payments and senior tranche distributions is captured before any residual yield flows down to $sUSD3 holders. The more distinctive aspect is what happens after a default, as their yield source is unsecured loans, there is no on-chain collateral to liquidate. Instead, 3Jane initiates off-chain recovery through a Dutch auction of non-performing credit lines, where licensed US collection agencies bid for the right to pursue the borrower. The protocol accounts for expected partial recoveries in its NAV through a progressive markdown system that gradually writes down delinquent loans rather than immediately marking them to zero. This introduces heavy dependency on the US legal system, recovery timelines that can take years, and the fundamental question of whether a "theoretical" recovery protects the immediate liquidity of the pool.

Avant maintains separate reserve funds for each of its three markets (USD, BTC, ETH), seeded with initial capital ($1M avUSD, 1.8 avBTC, 54.4 avETH) and grown through a 10% performance fee on strategy profits plus yield from unstaked avAsset backing. The design choice to isolate reserves per market prevents contagion across asset suites, which is a meaningful structural advantage. This reserve fund is designed to take the first loss, however, these funds are not held in the underlying asset but invested in the protocol's own productive assets (savUSD, savBTC, savETH), meaning the backstop is economically correlated with the system it is supposed to protect, which makes it redundant and does not offer protection. If a serious problem emerged in the underlying strategies, the reserve fund could deteriorate alongside the tranches it is meant to defend.

Yuzu also maintains a reserve fund as its second line of defense after the junior tranche $yzPP. The reserve fund grows during weeks of surplus and underwrite the yield during weeks of deficit, to smooth out yield distribution. Since inception, Yuzu reserve fund has paid out more than earned and currently sits at +430,000$.

4. Yield Distribution Mechanics

Once a protocol has defined its yield source and tranche structure, the next design decision is how the generated yield gets distributed between participants. The distribution mechanism is what defines who receives what share of the upside and who absorbs the downside when yield falls short of expectations.

4.1 Fixed-rate guarantees and multiplier models

The first generation used deterministic distribution rules where the senior's return yield was fixed at deposit time and the junior absorbed whatever remained.

In BarnBridge, the senior depositor received a fixed rate encoded in an NFT bond (sBOND) at the moment of entry, derived from a 3-day moving average of the underlying lending protocol's APY. From that point, the senior's return was guaranteed regardless of what rates did during the bond's life. If the pool earned more than the senior obligation, the surplus flowed entirely to juniors, if the pool earned less, juniors subsidized the shortfall from their own principal. The guarantee was absolute from the senior's perspective, but only as long as there was enough junior capital to back it.

Saffron used a multiplier model instead where the \(A\) tranche (junior) earned \(10\times\) its proportional share of the pool's total interest. This meant that in a \(\$100\text{k}\) pool where \(A\) tranche represented \(\$10\text{k}\), the \(A\) depositor captured \(\left(\frac{\$10\text{k}}{\$100\text{k}}\right) \times 10 \times \text{total interest}\), which meant they received almost \(100\%\) of the pool's interest. The \(S\) tranche (acting as senior) received whatever residual remained and Saffron tokens. When the junior grew too large or total interest was thin, the \(S\) tranche could end up earning nothing from interest, receiving only SFI token rewards, making \(S\) tranche unattractive as emissions declined.

Both models shared that the senior's economics were fully defined at entry and did not adjust to changing conditions mid-epoch. The junior was the residual claimant who bore all the variability, both upside and downside.

4.2 Non-fixed rate models

The current generation of product-native tranching protocols moved away from fixed guarantees toward models where yield distribution is dynamic, but the degree of transparency and predictability varies significantly across protocols.

Formula-driven distribution

Resolv has the most explicitly defined split. The protocol calculates PnL for 24-hour reward epochs, then, when the collateral pool generates a profit, that profit is divided into three parts:

- 76.5% as a base reward distributed pro rata between stUSR and RLP by TVL

- 13.5% as a risk premium allocated exclusively to RLP,

- 10% as a protocol fee directed to the treasury.

When the pool incurs a loss in a given epoch, 100% of the loss is allocated to RLP* and stUSR receives no distribution. A senior depositor knows exactly what percentage of profits he will receive and that they will only absorb a loss if RLP is completely wiped out.

*Resolv ToS states that “RLP is designed to protect USR from market and counterparty risks”, but the resolution and impact of the March 22nd exploit remains unknown.

Avant distributes yield on a weekly basis, finalized every Thursday. The senior tranche (savAsset) receives yield generated from the main strategy of its corresponding market and the yield is distributed in daily portions after the weekly calculation. The junior tranche (avAssetX) receives the same base yield plus an additional 10% of the total yield generated by all capital committed to the main strategy, and can also be deployed into separate DeFi strategies for additional returns. The distribution follows defined rules, but the underlying yield depends on the team's active management decisions. This means the split itself is structured, but the inputs feeding it are not formulaic.

Portfolio driven

3Jane's yield distribution is a function of the credit portfolio's performance. Each borrower pays a rate composed of a base rate plus an individual default risk premium, with an additional late repayment penalty if the borrower becomes delinquent. The yield that flows to depositors is the aggregate interest collected from all active credit lines. The tranche split follows the standard waterfall where sUSD3 (junior) absorbs losses first and captures the higher residual yield, while USD3 (senior) has priority and stability. What makes 3Jane's distribution distinct is that yield is not a function of market conditions or strategy execution but of borrower behavior and repayment discipline.

Discretionary allocation

Yuzu sits at the other end of the spectrum. The yield allocation for syzUSD (senior) is decided by the team every Wednesday, based on Accountable’s assessment of the portfolio's actual performance and their estimate of the next week's APY. There is no published formula and no on-chain mechanism enforcing the split. The junior tranche yzPP receives a base yield equivalent to syzUSD plus a daily risk premium following the formula:

\[ \text{yzPP}_\text{yield} = \text{syzUSD}_\text{APY} + \frac{0.15 \times \text{P&L}}{\text{yzPP}_\text{TVL}} \]

As Yuzu’s yield has been smoothened out thanks to the reserve fund, the yield distribution is not purely a reflection of portfolio performance, which introduces a layer of discretionary risk that is absent in other protocols.

5. Liquidity and Redemption Design

Different protocols impose different restrictions on exits, and in most cases the junior tranche faces longer lockups or restrictions than the senior, those exit conditions change depending on the health of the protocol.

5.1 Epoch-based lockups

Both BarnBridge and Saffron locked all capital into fixed 14-day epochs where deposits were frozen until settlement. Saffron offered no early exit at all, while BarnBridge allowed juniors to leave before the senior bond matured at the cost of surrendering their proportional share of the outstanding senior obligation.

This protected seniors from any shortfall caused by the early exit, but leaving during a period of high senior obligations could consume a significant portion of the junior's principal.

5.2 Timelocks

Current protocols moved away from rigid epochs toward cooldown-based models with varying durations and conditions.

Avant imposes a 24-hour cooldown for senior redemptions (savAsset) and 7 days for juniors (avAssetX). The junior cooldown faces another constraint, as during the waiting period, the tokens being withdrawn do not accrue yield, and the final redemption price is the lower of the price at request time or the price at the end of the cooldown. This means the junior redeemer bears full downside exposure during the wait but captures none of the upside, discouraging speculative exits and protecting remaining junior holders from dilution.

3Jane enforces a 1-month lockup on sUSD3 (junior), but even after the lockup expires, redemption is not guaranteed. Since the pool's capital is deployed in active unsecured credit lines, idle capital is parked in Aave and redemptions are capped by the USDC liquidity available there. If a large portion of the pool is in outstanding loans, the NAV may reflect the value of those credit lines but the actual liquid capital for redemptions could be significantly less. This creates a gap between what a position is theoretically worth and what a holder can actually extract at any given moment.

Yuzu's junior (yzPP) now operates on a 30-day cooldown with a last-order-wins rule, where submitting a new redemption request replaces any pending one. syzUSD has no lockup and the senior yzUSD is only redeemable for USDT0 (on Plasma) by eligible investors and can take up to 3-days with an instant redemption facility available for a 0.3% redemption fee. This cooldown model was introduced after the protocol moved away from a CR-based gate that had effectively trapped junior holders indefinitely, as described in 5.3.

5.3 Coverage-aware redemption

Some protocols tie redemption availability not to time but to the health of the system.

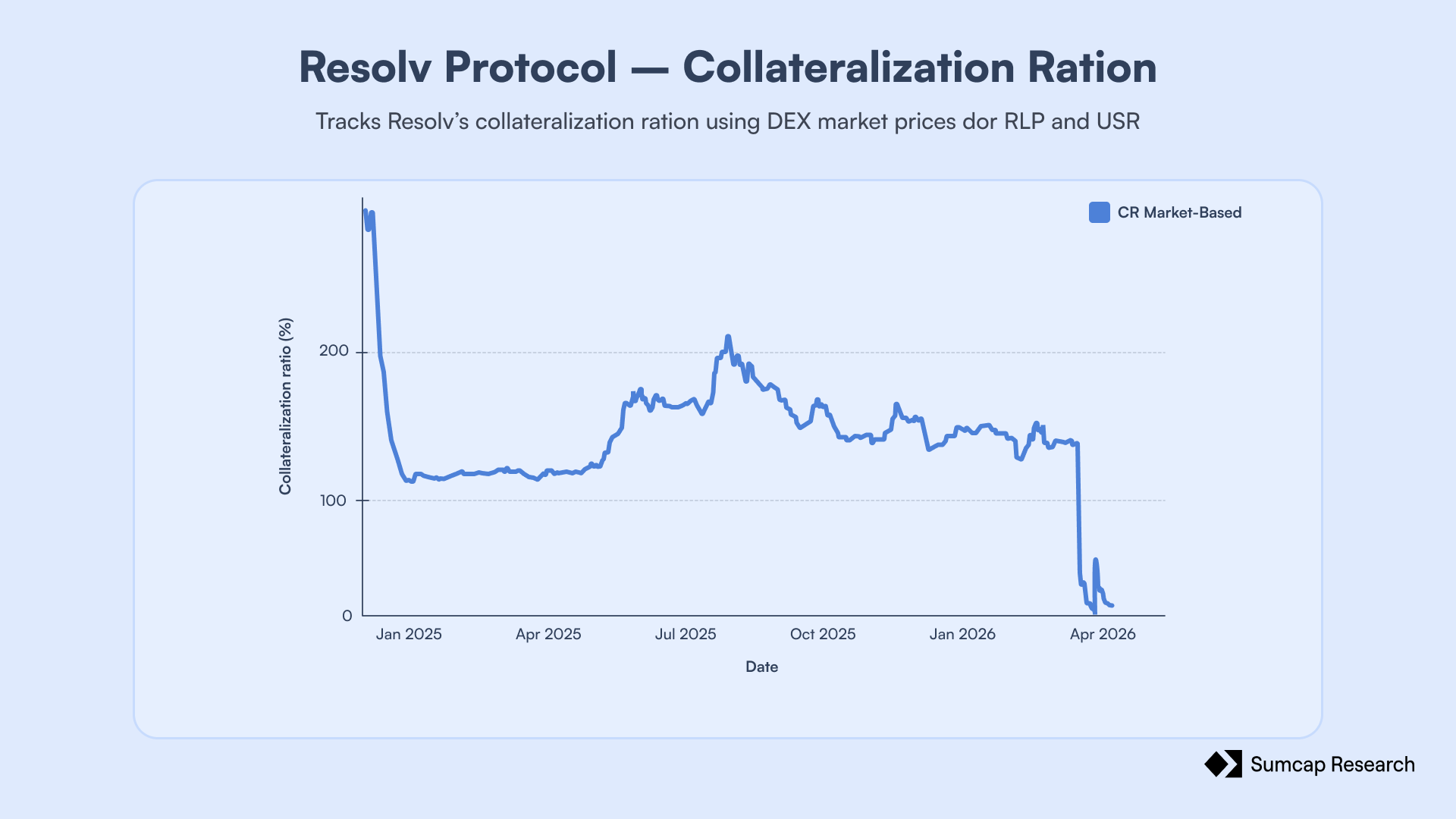

Resolv suspends RLP (junior) redemptions when the USR collateralisation ratio falls below 110%. There is no time-based lockup, but the junior cannot exit when the system is under the most stress. This protects the senior's coverage at the cost of trapping junior capital in a deteriorating position.

The drop on the CR in the image above is due to the March 2026 exploit where an unauthorized actor minted $80M of uncollateralised USR, thus causing the collateralisation ratio to drop from 137% to a minimum of 27%, freezing RLP redemptions.

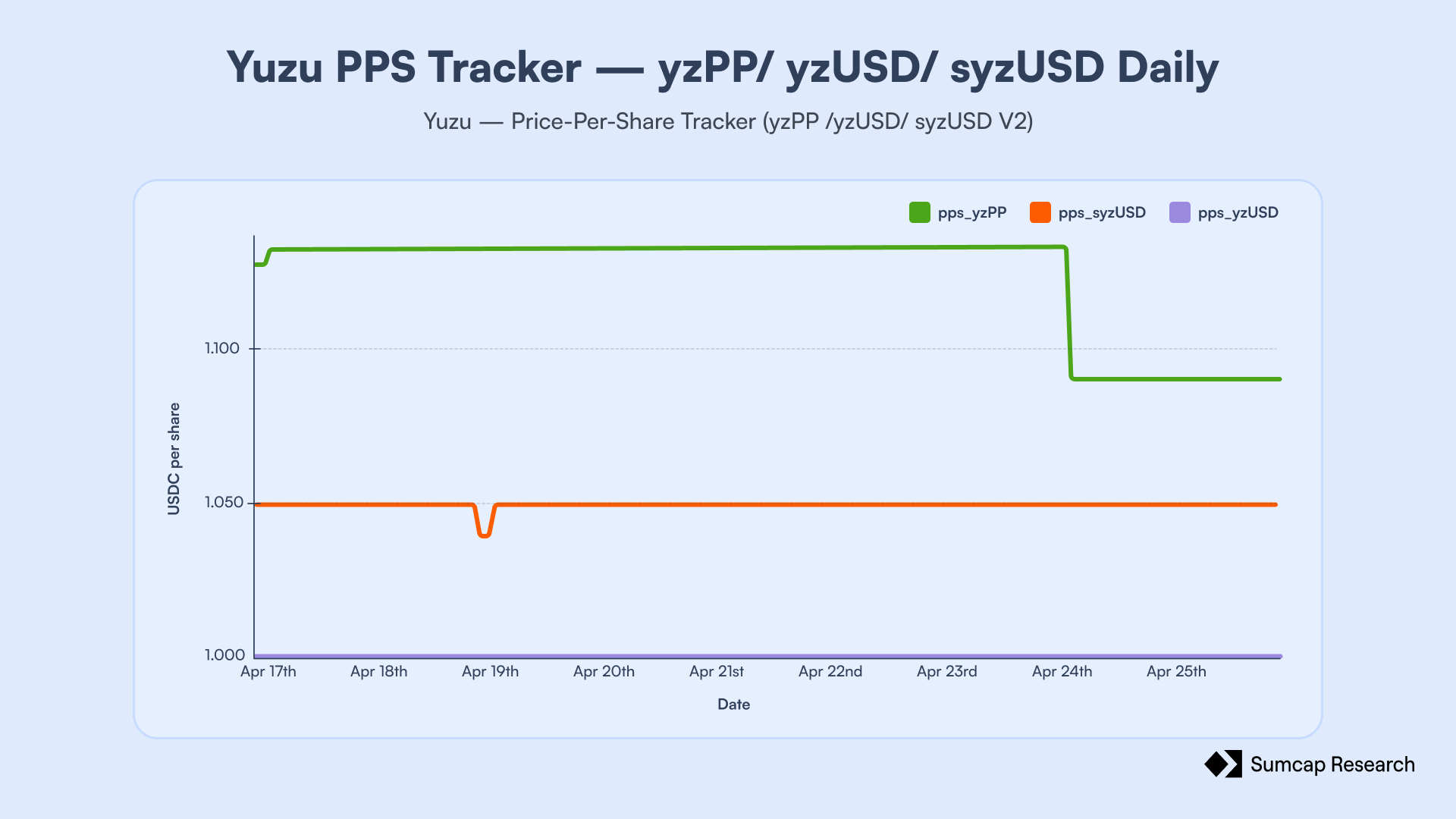

Yuzu operated under a similar model until recently where yzPP redemptions were only available when the CR exceeded 110%, but because the CR never reached that threshold, junior holders were effectively locked with no exit at redemption value (there's a secondary Curve market). The protocol has since replaced this with the 30-day cooldown described above, but its history shows the tension in coverage-based gates where seniors are protected at the cost of junior liquidity, and if the gate condition is never met, the junior position becomes illiquid.

The dynamics and trade-offs of coverage-aware gating become even more relevant when comparing product-native protocols with tranching-as-a-service platforms, which is explored further in Part III.

6. Incident Response

After the KelpDAO exploit, AAVE incurred close to 200M$ in bad debt due to contagion. This triggered widespread capital withdrawals, driving utilisation ratios to 100% in several markets. The resulting spike in borrowing costs rendered many carry strategies unprofitable. Yuzu and Avant were indirectly affected by these shifts in distinct ways, leading each to employ unique strategies for managing the incident.

Yuzu’s looped position in AAVE triggered an initial $169,693 drawdown for yzPP. While this represented a ~4.22% hit to the junior tranche or 0.25% of the protocol TVL, the team successfully resolved the incident in around 72 hours (of which ~36hours was due to widespread OFT/bridge pausing by several counterparts such as Tether’s USDT0) through OTC deals and capital rotations, passing from a -50% carry position to a +7%, allowing them to generate post-slashing yield, narrowing the final loss to $148,000 by the conclusion of the epoch.

On the other hand the syzUSD yield distribution (101,000$) was supported by the Reserve Fund, meaning that the senior tranche kept earning yield despite the junior slashing.

Avant, meanwhile, incurred $600,000 in total losses, representing approximately 0.4% of the protocol’s TVL. The savUSD pool was the most impacted, requiring a $553,000 draw from the reserve fund. This was followed by the ETH strategy, which utilised roughly 15 ETH from reserves, while the BTC strategy remained unaffected.

Avant covered 100% of the losses using the reserve funds and the senior yield was funded by the protocol treasury, ensuring no junior holder lost money.

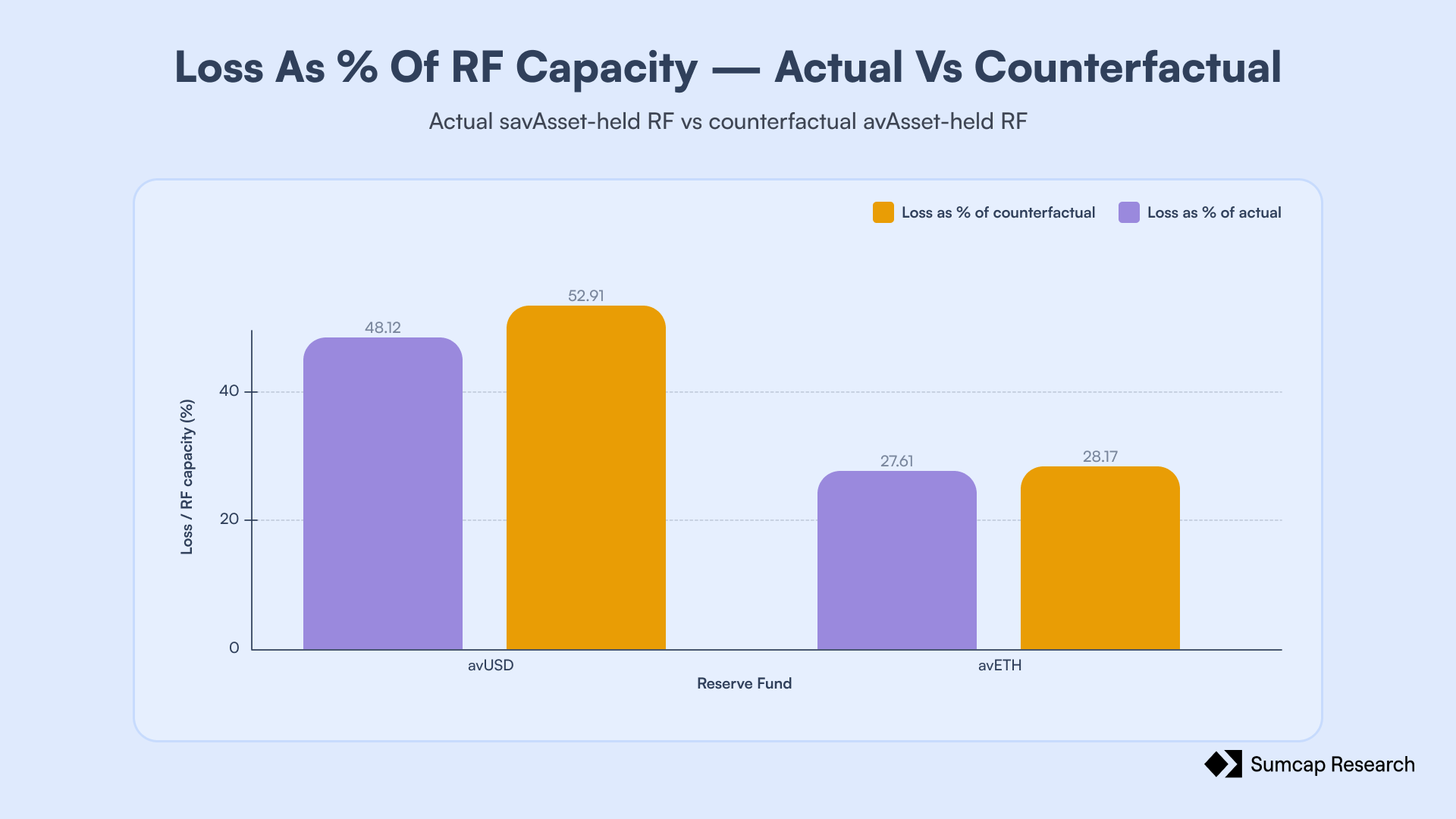

Notably, if Avant had held the Reserve Funds in plain avAssets (as the docs literally describe) instead of savAssets, the buffers going into the AAVE event would have been meaningfully smaller. The avUSD Reserve Fund would have had roughly \( \$103\text{k} \) less capacity (yield accrued since the initial deployment), meaning that the \( \$553\text{k} \) coverage payment would have consumed \( 52.9\% \) of the buffer instead of the actual \( 48.1\% \). On the ETH side, the avETH Reserve Fund would have entered the event with approximately \( 1.1\text{ avETH} \) less headroom, pushing the \( 15.28\text{ avETH} \) loss from \( 27.6\% \) of capacity up to \( 28.2\% \). By holding yield-bearing savAssets, the team earned additional buffer capacity across the two affected strategies.

However, the improved outcome came from a structure that made the backstop less clean. The Reserve Funds were deployed into Avant strategies, which meant they also participated in the same loss environment they were meant to protect against.

In the USD Suite, the Reserve Fund’s was \( 1,149,265.18\text{ avUSD} \) worth against a collateral pool of roughly \( \$122.5\text{m} \), making it approximately \( 0.94\% \) of the pool. As negative carry was generated across the deployed base, adding the Reserve Fund to that base marginally increases the losses that need to be absorbed. The \( \$553\text{k} \) coverage payment should therefore be read as the total loss absorbed by the avUSD Reserve Fund, not as a user-collateral loss to which the Reserve Fund’s own loss must be added on top. Because the Reserve Fund was deployed alongside the rest of the USD pool, a fraction of that \( \$553\text{k} \) loss was generated by the Reserve Fund’s own exposure. With \( 1.15\text{m avUSD} \) of Reserve Fund capacity against a USD collateral pool of roughly \( \$122.5\text{m} \), the Reserve Fund represented around \( 0.94\% \) of the deployed base. That implies that approximately \( \$5.2\text{k} \) of the \( \$553\text{k} \) coverage payment came from the Reserve Fund’s own participation in the same loss. The relevant point is that the buffer slightly increased the loss base it was meant to protect, so the realized payment was about \( 100.94\% \) of the loss that would have existed if the Reserve Fund had remained outside the strategy.

The ETH pool follows the same logic. The \( 15.28\text{ avETH} \) coverage payment already includes the loss attributable to the Reserve Fund’s. With \( 55.36\text{ avETH} \) of Reserve Fund capacity against \( 7.2\text{k ETH} \) pool, the Reserve Fund represented around \( 0.77\% \) of the deployed capital. That means that roughly \( 0.12\text{ avETH} \) of the \( 15.28\text{ avETH} \) loss came from the Reserve Fund’s exposure.

In this instance, the trade-off was economically positive as the avUSD Reserve Fund earned \( 103\text{k avUSD} \) of extra capacity and the avETH Reserve Fund earned \( 1.10\text{ avETH} \), while the incremental losses caused by deploying the Reserve Funds were much smaller. But as a risk-management design, the practice still increases the system’s loss surface and reduces the fallback protection.

Part II: Tranching as a Service

In this second part we examine protocols that do not generate yield themselves but instead provide the infrastructure to tranche any external yield source. These platforms define the rules for splitting risk and reward between senior and junior, but the underlying strategy and its performance belong to whoever deployed it.

6. The Platform Model

Tranching as a service emerged as a response to the coupling between yield engine and tranche structure that defines product-native protocols. The idea is to separate the tranching logic from the yield source entirely, creating a layer that can take any yield-bearing position and split it into senior and junior exposure using configurable parameters. This means a single tranching platform can serve dozens of different yield sources without having to build or manage any of them.

6.1 What tranching as a service means

In a Tranching-as-a-Service (Taas) model, the platform provides the contracts, the yield split logic, the accounting, and the redemption rules. The underlying yield source is an external input, typically an ERC-4626 vault or a tokenised asset pool, that plugs into the tranching layer. The platform does not control the strategy, does not manage the capital, and does not determine the raw yield; it only determines how that yield gets divided and under what conditions each tranche can enter or exit.

7. Yield Distribution Mechanics in TaaS

The core design question for any TaaS platform is how to price the protection that junior provides to seniors. Strata and Royco address this through different models.

7.1 Strata: benchmark-floored yield

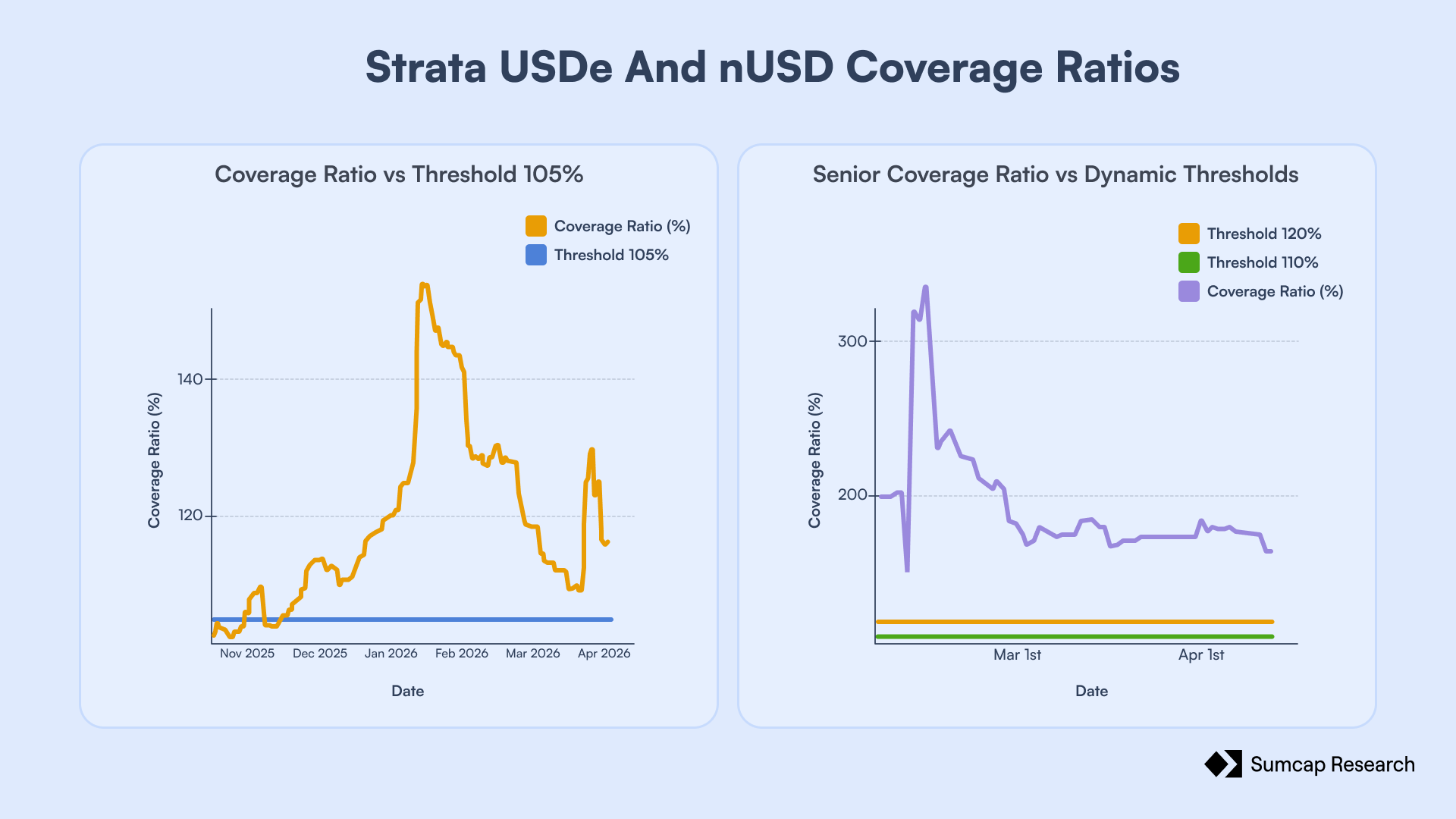

Strata splits any supported yield source into two ERC-4626 vaults, one senior and one junior, operating on the same base asset. The senior tranche receives a yield anchored to an external benchmark rate plus part of the underlying asset native yield. The benchmark rate is guaranteed. For the USDe market, this benchmark is the supply-weighted average of USDC and USDT lending rates on Aave v3 and for Neutrl's market, it is tied to the sUSDe APY.

Then, the risk premium, which represents the yield transferred from senior to junior as compensation for subordination, is calculated using an exponential function of the senior-to-junior TVL ratio and the underlying asset APY.

As more capital sits in senior relative to junior, the premium increases, redirecting more yield to junior. This creates a self-balancing incentive where junior becomes more attractive as senior grows, encouraging deposits that restore the coverage ratio.

In case the underlying yield falls short to cover the benchmark rate (which is guaranteed), junior subsidizes the senior from its own capital.

7.2 Royco Dawn: utilization-driven yield split

Royco takes a different approach. Instead of anchoring to an external benchmark, Royco derives pricing entirely from the internal supply-demand balance between tranches through its Yield Distribution Model (YDM).

The YDM measures how stretched junior capital is relative to the minimum coverage that the market requires at all times. That minimum coverage is calibrated at 100% utilisation, while lower utilisation leaves room for liquid deposits and withdrawals. This dynamic is governed by a yield curve defined at market creation, which behaves similarly to a Euler V1 utilisation rate model, with a target utilisation level that can gradually shift upward over days or weeks when utilisation remains persistently above target.

Royco also adds a product layer on top of the raw tranching infrastructure. The Dawn Senior Vault (DSV) is a separate ERC-4626 vault that allocates USDC across a curated and diversified basket of senior tranche positions from multiple Dawn markets.

7.3 Centrifuge: total personalization of tranches

Centrifuge operates at a lower level of abstraction. Rather than providing a specific yield split or rules, Centrifuge offers pool infrastructure where issuers configure their own capital structures, define how many share classes exist, assign custom valuation contracts to each asset, and control access through permissioning. This makes it less of a tranching protocol and more of a tokenization toolkit that can be used to build tranched products, particularly for real-world assets where standardized yield splits would not accommodate the diversity of underlying credit exposures. However, there are currently no tranches deployed by Centrifuge architecture.

8. Liquidity and Redemption Design in TaaS

A senior tranche without sufficient junior backing is a senior tranche without real protection Strata and Royco implement similar mechanisms based on the coverage ratio to prevent this.

If Strata senior coverage ratio falls below predefined thresholds, they may temporarily halt senior minting and junior redemptions, or allow junior redemptions only after a lockup period, to avoid depletion of the junior tranche and to maintain adequate coverage for the senior tranche. In the Ethena market, junior redemptions are blocked when the senior coverage ratio falls below 105%. In the Neutrl market, the restrictions are more granular, with junior redemptions facing progressively higher fees and longer cooldowns as coverage drops, ranging from instant exit with a 0.20% fee above when CR is 120% to a 35-day cooldown below 110%. Senior redemption fees adjust in the opposite direction, becoming cheaper as coverage tightens to encourage senior exits that naturally restore the ratio. Those parameters are defined by the protocol and calibrated using the results of in-house backtests.

Royco also handles redemption by restricting user actions that would result in less than minimum coverage that a market requires. This means that when utilisation hits the ceiling, new senior deposits are blocked, and existing juniors cannot withdraw. This gives senior depositors more stable coverage, but it also makes growth dependent on the available junior supply. If the yield share is imbalanced (YDM), deposits stall until the adaptive curve shifts enough.

The mechanism that Strata and Royco uses, mirrors the same dynamic we observed in Resolv and the prior version of Yuzu in Part I, but with the difference that their models are more market-driven (each on its own way) in the sense that deposits almost always flow freely and the system may adjust different parameters (YDM for Royco and fees or timing in Strata) in response to coverage conditions, which means that protocol growth is never directly throttled by the mechanism itself.

9. Incident Response

Strata had a slightly different problem. During the stress event, Aave utilisation for USDC and USDT reached 100%, which pushed the baseline borrowing/supply rate sharply higher, roughly into the 14–15% range. Since Strata’s senior USDe rate was benchmarked against that external USDC/USDT rate, the senior guaranteed return also increased. The issue was that USDe’s underlying yield was far below that benchmark, so the gap had to be subsidised by the junior tranche.

Strata’s response was to change the benchmark APY for senior USDe to the “pre-stress supply-weighted average of USDC/USDT”. This protected junior holders from being drained by a benchmark rate that had temporarily detached from the actual yield of the underlying collateral. But the adjustment shifted the adverse effect onto PT-srUSDe loopers, the backbone of Strata’s TVL.

A typical PT loop starts with USDC or USDT, swaps into srUSDe, mints PT-srUSDe and YT-srUSDe, posts the PT-srUSDe as collateral to borrow more USDC/USDT and then repeat the process. This strategy was meant to hedge rate volatility on the underlying because the user kept the YT side, which should benefit when the underlying yield rises, but once the benchmark was reset, that relationship broke. PT loopers still faced the higher borrowing costs, but their srUSDe exposure no longer captured the same upside through the senior benchmark, which led into a leveraged negative carry trade.

.png)

Part III: Product vs. Service

This final part brings them together, comparing the trade-offs each model makes, where risk actually sits in each design, and what happens when tranche tokens leave their native context and enter the broader DeFi.

9. Comparative Analysis

9.1 TaaP vs. TaaS

In Tranche-as-a-Product (Taap), the protocol is responsible for both the strategy and the structure, meaning that if the yield engine fails, the protocol fails. In TaaS, the platform is accountable for the structure but not for the strategy, if the underlying vault suffers a drawdown, the tranching layer functioned correctly as long as the loss waterfall operated as designed and junior absorbed what it was supposed to absorb.

This means that a TaaP protocol can only grow by scaling its own strategy, which means every dollar of new TVL adds exposure to the same yield engine. If a protocol grows from $100M to $1B, it needs ten times the return capacity, ten times the counterparty exposure, and become ten times more dependent on the funding rates. A TaaS platform grows by onboarding new yield sources, which means growth diversifies the platform.

Both work, but have different ceilings and different ways of breaking.

10. Composability and Risk Propagation

As tranche tokens gain adoption, they will find their way into the broader DeFi as collateral on money markets or to mint CDPs. This creates a new layer of risk on top of the tranching structure itself, and raises questions about the risk that carries this integration.

10.1 Tranche tokens as collateral

The simplest case for collateral listing is the Dawn Senior Vault (DSV). Because the DSV allocates across a curated and diversified basket of senior tranche positions from multiple Dawn markets with concentration limits per market, a money market accepting DSV as collateral is not exposed to any single underlying strategy. The diversification means that a problem in any single underlying vault does not compromise the entire position, and the senior priority within each market provides an additional layer of protection. But the DSV also stacks additional smart contract layers on top of the base asset: the underlying vault's contracts, the Dawn tranching contracts, and the DSV aggregation contracts, something that must be priced in. Risk teams listing DSV need to determine whether the diversification benefit outweighs the additional smart contract surface, and whether DSV should carry a higher or lower LTV than an individual senior tranche position that has less abstraction but more concentration. Neither answer is self-evident, and defaulting to a conservative LTV without modelling both dimensions means leaving capital efficiency on the table or underpricing tail risk.

Listing an individual senior tranche also exposes the same problem. Consider a Strata senior vault on USDe listed as collateral alongside base USDe on the same money market. The senior has junior protection underneath it, meaning it is structurally more resilient to a drawdown in the underlying yield source than naked USDe, but it also carries additional smart contract risk from the tranching layer and less liquidity. The instinct to assign it a lower LTV than base USDe because of the added complexity would ignore the subordination protection. The instinct to assign it a higher LTV because of the protection would ignore the liquidity and smart contract risks. Any LTV that doesn't account for both dimensions is mispricing the asset.

The senior-versus-junior LTV question is more straightforward directionally but dangerous in its details. A senior tranche should clearly receive a higher LTV than a junior tranche from the same market. But the magnitude of that differential depends on the current junior coverage ratio, which is not static. A senior tranche backed by 30% junior coverage is a different asset than the same senior tranche backed by 5% junior coverage. If the LTV is fixed at listing time, it becomes stale the moment coverage changes, and the money market is extending credit based on protection that may no longer exist. If the LTV is dynamic, borrowers face the risk of their positions becoming liquidatable not because the collateral price dropped but because junior holders exited. Either approach has failure modes, and money markets that list tranche tokens without modeling the coverage dependency are building on assumptions they cannot enforce.

10.2 How risk propagates through the stack

When a senior tranche token sits as collateral on a money market, a loss event in the underlying strategy propagates through multiple layers. A drawdown first hits the junior tranche. If the junior buffer holds, the senior is unaffected and the collateral value remains stable. If the junior is wiped out, the senior begins absorbing losses, the collateral value drops, and the borrower's money market position moves toward liquidation.

But liquidation assumes the collateral can actually be sold or redeemed. A senior tranche with a 24-hour cooldown, a junior tranche with a 7-day cooldown, or a position gated behind a coverage ratio threshold cannot be liquidated instantly. The money market's solvency depends on converting collateral to the base asset within a timeframe that covers the outstanding debt. If the tranche token's redemption is delayed or blocked precisely during the conditions that triggered the liquidation, the money market can incur in bad debt.

The problem is even bigger if the money market has adopted a dynamic LTV model tied to the junior coverage ratio. When the junior takes a loss, the coverage ratio drops, which should trigger an LTV reduction on the senior collateral (that may trigger more liquidations). But this adjustment needs to propagate fast enough to reflect the new reality before borrowers extract value at the old, now-stale LTV. If the coverage ratio drops sharply in a single event and the LTV oracle updates on a slower cadence, there is a window where the money market is lending against protection that has already been partially consumed. The speed of LTV adjustment and the Oracle cadence become critical design parameters, and any lag between a junior loss and the corresponding LTV change creates an arbitrage window at the expense of the money market's lenders.

The problem is that tranche tokens are designed with internal mechanisms (coverage gates, cooldowns, loss waterfalls) that assume a certain pace of adjustment while money markets are designed with liquidation mechanisms that need speed to maintain the protocol solvent. When a tranche token becomes collateral, these two things collide. Both cannot be right simultaneously during a stress event, and neither system was designed with the other's constraints in mind. This is not a problem unique to tranche tokens, as RWA collateral faces an analogous version of the same tension, where the on-chain token represents a claim on an asset whose liquidation happens off-chain, on legal timelines that are measured in days or weeks.

11. Conclusion

DeFi tranching has moved well beyond its first-generation origins of wrapping lending rates into fixed and variable positions. The landscape now spans proprietary basis trades, unsecured credit lines, leveraged stablecoin loops, and strategy-agnostic platforms that can tranche any yield-bearing vault. The article framed this evolution around protocols that tranche their own yield versus protocols that tranche anyone's yield. That distinction, as this analysis has shown, shapes everything downstream, from how yield is distributed and how losses are absorbed to how redemptions are gated and how collateral is priced when tranche tokens enter the broader DeFi stack.

From a protocol perspective, the scalability dynamics of each model are fundamentally different. TaaP grows by scaling its own strategy, which means every new dollar of TVL deepens the protocol's exposure to the same yield engine which creates natural ceilings as basis trade capacity is finite and bigger portfolios require more underwriting infrastructure as they grow. TaaS grows by onboarding new yield sources, which means the platform can expand without concentrating risk in a single strategy. But this horizontal scalability comes at the cost of depending on external teams to build and maintain the yield sources and its growth is ultimately bounded by the quality and diversity of vaults available to plug in.

Recent events have also made clear that tranching is not only a yield-packaging mechanism, but a risk-management primitive. By separating senior and junior claims, protocols can contain losses, define who absorbs volatility first, and avoid forcing every depositor into the same risk bucket. That said, the adoption of tranche tokens across the broader DeFi ecosystem, whether as collateral or inputs to further structured products, will be the key driver of growth for the entire space, but the questions around collateral pricing, liquidation feasibility, and risk propagation across protocols remain unanswered.

Tranching in DeFi

DeFi tranching separates one yield stream into senior and junior risk-return profiles. This article compares product-native and service-based models, covering yield sources, waterfalls, redemption gates, reserve funds, collateral use and how tranche tokens reshape risk across DeFi ecosystems.

DeFi doesn't have a yield problem, it has a risk problem. All the yield sources exist, but they force everyone into the same position without risk segregation. Tranching fixes this by letting protocols separate who gets paid first from who gets paid most, so that both sides get a product that matches their risk appetite.

1. Introduction

1.1 What is tranching in DeFi

Tranching is the segmentation of a single yield stream into instruments with distinct risk-return profiles. A senior tranche receives priority on cash flows with loss protection in exchange for capped upside, while a junior tranche absorbs first losses and captures the residuals, the excess yield that remains after the senior obligations are met.

The concept is borrowed directly from structured credit in traditional finance, where CLOs and CDOs slice loan portfolios into rated tranches with sequential payment waterfalls. In DeFi, the same logic applies but the yield sources, mechanisms, and liquidity dynamics are different.

BarnBridge and Saffron Finance were the first to bring tranches on-chain in 2020, wrapping Compound and Aave lending rates into fixed-rate senior bonds and leveraged-yield junior positions. Both protocols proved the concept but struggled with sustainability as yield depended on token emissions, and demand imbalances between tranches made the economics fragile. They demonstrated that tranching had demand on-chain attracting hundreds of millions in TVL in a short period, but left open the question of whether it could economically work without subsidies.

Today, protocols like Resolv, Yuzu, Strata, Royco and 3Jane (among others), have revisited the problem with more diverse yield sources, more sophisticated loss absorption mechanisms, and different design philosophies.

1.2 Two paradigms

These newer protocols split into two distinct approaches.

The first is tranching as a product: this category includes protocols like Resolv, Avant, Yuzu, and 3Jane that generate their own yield through basis & carry trades, multi-strategies, or unsecured credit to build senior/junior tranches natively around that yield engine. This means the protocol controls how yield is generated, how it flows between tranches, how losses are absorbed, and under what conditions users can exit.

The second is tranching as a service: where platforms such as Strata, Royco Dawn, and Centrifuge don't generate yield themselves. Instead, they use the underlyings’ yield source such as an ERC-4626 vault or a tokenized credit pool, and split it into tranches. They present the infrastructure, the risk of the underlying strategy belongs entirely to whoever deployed it, not at the tranche layer. The platform defines the rules for splitting yield and absorbing losses, but it has no control over whether the underlying vault suffers a drawdown, a depeg, or a liquidity crisis.

This distinction shapes how yield is distributed, where losses land and what happens when tranche tokens start circulating as collateral in other protocols.

Part I: Tranching as a Product

In this first part we examine protocols that generate their own yield and build tranches natively around it. These protocols own the full vertical, from strategy execution to loss absorption, and their tranche design is inseparable from the yield engine underneath.

2. Yield Sources

The yield source is what defines the risk segregation. In protocols that build tranches in-house, the yield engine is proprietary and the protocol is directly responsible for its performance. This section covers the yield sources behind product-native tranching protocols, from the earliest lending market wrappers to the market-neutral strategies operating today.

2.1 Lending market wrappers

The first generation of DeFi tranching protocols did not generate yield on their own. BarnBridge and Saffron Finance both captured the variable interest flowing from lending markets (Compound and Aave), and redistributed it according to their own tranche rules.

User deposits were routed into lending protocols, and the resulting variable rate was split between a senior position that received a fixed or priority return and a junior position that absorbed the volatility.

In BarnBridge, the senior received a fixed rate derived from a 3d MA of the underlying protocol's APY. In Saffron, the junior received a leveraged multiplier (default 10x) on their share of pool interest, funded by the yield that senior depositors gave up and the seniors received practically only $SFI incentives.

Both protocols relied heavily on governance token rewards ($COMP, $AAVE) as yield source. These rewards were harvested, sold for the base asset, and reinjected into the pool as an additional yield source. This dependency meant that the economics of the tranches were completely tied to the price of tokens that the protocol did not control, making the yield profile fragile when emissions declined or token prices dropped.

2.2 Delta-neutral and market-neutral strategies

The current generation moved away from wrapping lending rates and relaying token emissions to build yield engines around market-neutral positioning.

Resolv generates yield through a delta-neutral basis trade. The protocol holds spot positions in ETH and BTC alongside short perpetual futures, capturing the funding rate differential while remaining neutral. This strategy is complemented by DeFi deployments of stablecoin reserves and a smaller allocation to tokenized RWA assets (AAA-rated CLOs via Centrifuge). The portfolio is designed to produce consistent yield without taking directional market exposure.

Avant operates through an actively managed multi-strategy framework organized around three independent markets which are USD, BTC, and ETH. Each market has its own strategy and deploys capital into a distinct basket of strategies that include basis trades, money market carry trades, and yield trading. This means the yield profile, risk exposure, and performance of each market are independent from one another.

Yuzu generates yield by running leveraged stablecoin loops, stablecoin arbitrages, CLOs and other strategies. These strategies have no directional exposure (Δ = 0), but they carry meaningful leverage mitigated by the use of fundamental oracles on money markets.

What connects these three is that none of them rely on token emissions or governance rewards as a primary yield source. The yield is structural, coming from native DeFi strategies and organic market conditions. This makes them more self-sustaining than their first-generation predecessors.

2.3 Unsecured credit

Instead of capturing on-chain lending rates or running market-neutral trades, 3Jane generate yield from unsecured USDC credit lines issued to borrowers who do not post on-chain collateral at the time of borrowing.

To open a credit line, a borrower connects their wallet, links a bank account, and submits zkTLS proofs of creditworthiness from sources including DeFi positions, centralized exchange balances, bank cash flows, and traditional credit scores. Based on this data, the protocol's 3CA algorithm assigns a credit line size, a default risk premium, and a repayment schedule. The yield that depositors earn comes directly from the interest charged on these credit lines.

This makes 3Jane's yield source closer to what a traditional prime brokerage or consumer lending platform would generate than anything else in the DeFi tranching space. The return is a function of credit spreads. The quality of that return depends entirely on how well the underwriting model estimates default probability and loss severity, which is a very different risk profile from basis trades or leveraged loops.

3. Tranche Architecture

Once a protocol has a yield source, the next design decision is how to structure the tranches around it. How many tranches, what role each one plays, and which mechanisms absorb losses beyond the junior position.

3.1 Two-tranche and three-tranche models

The majority of protocols chooses to tranche the assets in a two-tranche model, a senior position with priority on cash flows and loss protection paired with a junior position that absorbs first losses and captures residual yield. Most protocols covered in this piece follow this structure, whether they implement it as two distinct vaults, two ERC-4626 tokens, or a base-staked design.

Some protocols have experimented with three tranches.

Saffron Finance introduced a super-senior (\(AA\)), junior (\(A\)), and balancing (\(S\)) tranche, where the \(S\) tranche dynamically absorbed the imbalance between senior and junior demand to keep the yield multiplier consistent. Since organic deposits rarely arrived in that perfect ratio (\(\frac{AA}{A}=10\)), the \(S\) tranche existed to absorb the imbalance. It split itself internally into "utilised" capital, which actively backed the multiplier and earned the residual yield, and "unutilized" capital, which sat idle and earned no interest at all (if \(S > 10 \times A\) then not all capital of \(S\) could be deployed to \(AA\) because it wouldn't satisfy the ratio \(\frac{AA}{A}=10\)).

Actually, the only way to get into (\(AA\)) tranche was through the (\(S\)) tranche, as direct deposits into it were not possible, this made S tranche to end up performing both as the senior and balancing roles simultaneously, which made the system harder to reason about without adding economic differentiation.

Mezzanine aims to take a different approach with three explicitly layered tranches, this protocol will have a senior ($smzUSD), a mezzanine liquidity tranche (MLT) designed for DeFi composability, and a junior (JLT) that takes first-loss exposure. The protocol has not yet launched, so the real-world dynamics of this three-layer structure remain to be tested.

In both cases, the added complexity of a third tranche introduces questions about whether the intermediate layer occupies a distinct risk-return niche or simply fragments liquidity without creating a meaningfully different product for users.

3.2 Base token + staked tranche designs

Several current protocols share a design that differs from the classic senior/junior split. Instead of offering two separate deposit entry points, they start with a base token that represents a 1:1 claim on the underlying asset and then layer tranched exposure through staking derivatives on top of it.

Resolv issues USR as its base stablecoin, which can then be staked into $stUSR (senior yield exposure) or users can separately mint $RLP (the junior first-loss token). Avant mints avAsset ($avUSD, $avBTC, $avETH) at a 1:1 ratio to the underlying and then offers savAsset as the senior tranche and avAssetX as the junior. Yuzu follows a similar logic with $yzUSD as the senior , $syzUSD as the staked variant for yield (an ERC-4626 wrapper), and $yzPP as the junior.

What makes this pattern distinct from a simple two-vault senior/junior is that it introduces the base token holder who has neither senior yield priority nor junior first-loss exposure, but whose capital is nonetheless part of the system.

3.3 Reserve funds and insurance layers

Every tranching protocol needs a mechanism for what happens when yield falls short or losses materialize. The junior tranche is usually the first layer of absorption, but some protocols incorporate a reserve fund or an insurance layer to protect even more their depositors.

3Jane has the most layered loss architecture. The waterfall flows through an insurance fund, then through the junior tranche ($sUSD3), and only if both are exhausted does the senior ($USD3) take a hit. The reserve fund grows organically through a "Reserve Accrual" mechanism, whereby a portion of the excess spread between borrower interest payments and senior tranche distributions is captured before any residual yield flows down to $sUSD3 holders. The more distinctive aspect is what happens after a default, as their yield source is unsecured loans, there is no on-chain collateral to liquidate. Instead, 3Jane initiates off-chain recovery through a Dutch auction of non-performing credit lines, where licensed US collection agencies bid for the right to pursue the borrower. The protocol accounts for expected partial recoveries in its NAV through a progressive markdown system that gradually writes down delinquent loans rather than immediately marking them to zero. This introduces heavy dependency on the US legal system, recovery timelines that can take years, and the fundamental question of whether a "theoretical" recovery protects the immediate liquidity of the pool.

Avant maintains separate reserve funds for each of its three markets (USD, BTC, ETH), seeded with initial capital ($1M avUSD, 1.8 avBTC, 54.4 avETH) and grown through a 10% performance fee on strategy profits plus yield from unstaked avAsset backing. The design choice to isolate reserves per market prevents contagion across asset suites, which is a meaningful structural advantage. This reserve fund is designed to take the first loss, however, these funds are not held in the underlying asset but invested in the protocol's own productive assets (savUSD, savBTC, savETH), meaning the backstop is economically correlated with the system it is supposed to protect, which makes it redundant and does not offer protection. If a serious problem emerged in the underlying strategies, the reserve fund could deteriorate alongside the tranches it is meant to defend.

Yuzu also maintains a reserve fund as its second line of defense after the junior tranche $yzPP. The reserve fund grows during weeks of surplus and underwrite the yield during weeks of deficit, to smooth out yield distribution. Since inception, Yuzu reserve fund has paid out more than earned and currently sits at +430,000$.

4. Yield Distribution Mechanics

Once a protocol has defined its yield source and tranche structure, the next design decision is how the generated yield gets distributed between participants. The distribution mechanism is what defines who receives what share of the upside and who absorbs the downside when yield falls short of expectations.

4.1 Fixed-rate guarantees and multiplier models

The first generation used deterministic distribution rules where the senior's return yield was fixed at deposit time and the junior absorbed whatever remained.

In BarnBridge, the senior depositor received a fixed rate encoded in an NFT bond (sBOND) at the moment of entry, derived from a 3-day moving average of the underlying lending protocol's APY. From that point, the senior's return was guaranteed regardless of what rates did during the bond's life. If the pool earned more than the senior obligation, the surplus flowed entirely to juniors, if the pool earned less, juniors subsidized the shortfall from their own principal. The guarantee was absolute from the senior's perspective, but only as long as there was enough junior capital to back it.

Saffron used a multiplier model instead where the \(A\) tranche (junior) earned \(10\times\) its proportional share of the pool's total interest. This meant that in a \(\$100\text{k}\) pool where \(A\) tranche represented \(\$10\text{k}\), the \(A\) depositor captured \(\left(\frac{\$10\text{k}}{\$100\text{k}}\right) \times 10 \times \text{total interest}\), which meant they received almost \(100\%\) of the pool's interest. The \(S\) tranche (acting as senior) received whatever residual remained and Saffron tokens. When the junior grew too large or total interest was thin, the \(S\) tranche could end up earning nothing from interest, receiving only SFI token rewards, making \(S\) tranche unattractive as emissions declined.

Both models shared that the senior's economics were fully defined at entry and did not adjust to changing conditions mid-epoch. The junior was the residual claimant who bore all the variability, both upside and downside.

4.2 Non-fixed rate models

The current generation of product-native tranching protocols moved away from fixed guarantees toward models where yield distribution is dynamic, but the degree of transparency and predictability varies significantly across protocols.

Formula-driven distribution

Resolv has the most explicitly defined split. The protocol calculates PnL for 24-hour reward epochs, then, when the collateral pool generates a profit, that profit is divided into three parts:

- 76.5% as a base reward distributed pro rata between stUSR and RLP by TVL

- 13.5% as a risk premium allocated exclusively to RLP,

- 10% as a protocol fee directed to the treasury.

When the pool incurs a loss in a given epoch, 100% of the loss is allocated to RLP* and stUSR receives no distribution. A senior depositor knows exactly what percentage of profits he will receive and that they will only absorb a loss if RLP is completely wiped out.

*Resolv ToS states that “RLP is designed to protect USR from market and counterparty risks”, but the resolution and impact of the March 22nd exploit remains unknown.

Avant distributes yield on a weekly basis, finalized every Thursday. The senior tranche (savAsset) receives yield generated from the main strategy of its corresponding market and the yield is distributed in daily portions after the weekly calculation. The junior tranche (avAssetX) receives the same base yield plus an additional 10% of the total yield generated by all capital committed to the main strategy, and can also be deployed into separate DeFi strategies for additional returns. The distribution follows defined rules, but the underlying yield depends on the team's active management decisions. This means the split itself is structured, but the inputs feeding it are not formulaic.

Portfolio driven

3Jane's yield distribution is a function of the credit portfolio's performance. Each borrower pays a rate composed of a base rate plus an individual default risk premium, with an additional late repayment penalty if the borrower becomes delinquent. The yield that flows to depositors is the aggregate interest collected from all active credit lines. The tranche split follows the standard waterfall where sUSD3 (junior) absorbs losses first and captures the higher residual yield, while USD3 (senior) has priority and stability. What makes 3Jane's distribution distinct is that yield is not a function of market conditions or strategy execution but of borrower behavior and repayment discipline.

Discretionary allocation

Yuzu sits at the other end of the spectrum. The yield allocation for syzUSD (senior) is decided by the team every Wednesday, based on Accountable’s assessment of the portfolio's actual performance and their estimate of the next week's APY. There is no published formula and no on-chain mechanism enforcing the split. The junior tranche yzPP receives a base yield equivalent to syzUSD plus a daily risk premium following the formula:

\[ \text{yzPP}_\text{yield} = \text{syzUSD}_\text{APY} + \frac{0.15 \times \text{P&L}}{\text{yzPP}_\text{TVL}} \]

As Yuzu’s yield has been smoothened out thanks to the reserve fund, the yield distribution is not purely a reflection of portfolio performance, which introduces a layer of discretionary risk that is absent in other protocols.

5. Liquidity and Redemption Design

Different protocols impose different restrictions on exits, and in most cases the junior tranche faces longer lockups or restrictions than the senior, those exit conditions change depending on the health of the protocol.

5.1 Epoch-based lockups

Both BarnBridge and Saffron locked all capital into fixed 14-day epochs where deposits were frozen until settlement. Saffron offered no early exit at all, while BarnBridge allowed juniors to leave before the senior bond matured at the cost of surrendering their proportional share of the outstanding senior obligation.

This protected seniors from any shortfall caused by the early exit, but leaving during a period of high senior obligations could consume a significant portion of the junior's principal.

5.2 Timelocks

Current protocols moved away from rigid epochs toward cooldown-based models with varying durations and conditions.

Avant imposes a 24-hour cooldown for senior redemptions (savAsset) and 7 days for juniors (avAssetX). The junior cooldown faces another constraint, as during the waiting period, the tokens being withdrawn do not accrue yield, and the final redemption price is the lower of the price at request time or the price at the end of the cooldown. This means the junior redeemer bears full downside exposure during the wait but captures none of the upside, discouraging speculative exits and protecting remaining junior holders from dilution.

3Jane enforces a 1-month lockup on sUSD3 (junior), but even after the lockup expires, redemption is not guaranteed. Since the pool's capital is deployed in active unsecured credit lines, idle capital is parked in Aave and redemptions are capped by the USDC liquidity available there. If a large portion of the pool is in outstanding loans, the NAV may reflect the value of those credit lines but the actual liquid capital for redemptions could be significantly less. This creates a gap between what a position is theoretically worth and what a holder can actually extract at any given moment.

Yuzu's junior (yzPP) now operates on a 30-day cooldown with a last-order-wins rule, where submitting a new redemption request replaces any pending one. syzUSD has no lockup and the senior yzUSD is only redeemable for USDT0 (on Plasma) by eligible investors and can take up to 3-days with an instant redemption facility available for a 0.3% redemption fee. This cooldown model was introduced after the protocol moved away from a CR-based gate that had effectively trapped junior holders indefinitely, as described in 5.3.

5.3 Coverage-aware redemption

Some protocols tie redemption availability not to time but to the health of the system.

Resolv suspends RLP (junior) redemptions when the USR collateralisation ratio falls below 110%. There is no time-based lockup, but the junior cannot exit when the system is under the most stress. This protects the senior's coverage at the cost of trapping junior capital in a deteriorating position.

The drop on the CR in the image above is due to the March 2026 exploit where an unauthorized actor minted $80M of uncollateralised USR, thus causing the collateralisation ratio to drop from 137% to a minimum of 27%, freezing RLP redemptions.

Yuzu operated under a similar model until recently where yzPP redemptions were only available when the CR exceeded 110%, but because the CR never reached that threshold, junior holders were effectively locked with no exit at redemption value (there's a secondary Curve market). The protocol has since replaced this with the 30-day cooldown described above, but its history shows the tension in coverage-based gates where seniors are protected at the cost of junior liquidity, and if the gate condition is never met, the junior position becomes illiquid.

The dynamics and trade-offs of coverage-aware gating become even more relevant when comparing product-native protocols with tranching-as-a-service platforms, which is explored further in Part III.

6. Incident Response

After the KelpDAO exploit, AAVE incurred close to 200M$ in bad debt due to contagion. This triggered widespread capital withdrawals, driving utilisation ratios to 100% in several markets. The resulting spike in borrowing costs rendered many carry strategies unprofitable. Yuzu and Avant were indirectly affected by these shifts in distinct ways, leading each to employ unique strategies for managing the incident.

Yuzu’s looped position in AAVE triggered an initial $169,693 drawdown for yzPP. While this represented a ~4.22% hit to the junior tranche or 0.25% of the protocol TVL, the team successfully resolved the incident in around 72 hours (of which ~36hours was due to widespread OFT/bridge pausing by several counterparts such as Tether’s USDT0) through OTC deals and capital rotations, passing from a -50% carry position to a +7%, allowing them to generate post-slashing yield, narrowing the final loss to $148,000 by the conclusion of the epoch.

On the other hand the syzUSD yield distribution (101,000$) was supported by the Reserve Fund, meaning that the senior tranche kept earning yield despite the junior slashing.

Avant, meanwhile, incurred $600,000 in total losses, representing approximately 0.4% of the protocol’s TVL. The savUSD pool was the most impacted, requiring a $553,000 draw from the reserve fund. This was followed by the ETH strategy, which utilised roughly 15 ETH from reserves, while the BTC strategy remained unaffected.

Avant covered 100% of the losses using the reserve funds and the senior yield was funded by the protocol treasury, ensuring no junior holder lost money.

Notably, if Avant had held the Reserve Funds in plain avAssets (as the docs literally describe) instead of savAssets, the buffers going into the AAVE event would have been meaningfully smaller. The avUSD Reserve Fund would have had roughly \( \$103\text{k} \) less capacity (yield accrued since the initial deployment), meaning that the \( \$553\text{k} \) coverage payment would have consumed \( 52.9\% \) of the buffer instead of the actual \( 48.1\% \). On the ETH side, the avETH Reserve Fund would have entered the event with approximately \( 1.1\text{ avETH} \) less headroom, pushing the \( 15.28\text{ avETH} \) loss from \( 27.6\% \) of capacity up to \( 28.2\% \). By holding yield-bearing savAssets, the team earned additional buffer capacity across the two affected strategies.

However, the improved outcome came from a structure that made the backstop less clean. The Reserve Funds were deployed into Avant strategies, which meant they also participated in the same loss environment they were meant to protect against.

In the USD Suite, the Reserve Fund’s was \( 1,149,265.18\text{ avUSD} \) worth against a collateral pool of roughly \( \$122.5\text{m} \), making it approximately \( 0.94\% \) of the pool. As negative carry was generated across the deployed base, adding the Reserve Fund to that base marginally increases the losses that need to be absorbed. The \( \$553\text{k} \) coverage payment should therefore be read as the total loss absorbed by the avUSD Reserve Fund, not as a user-collateral loss to which the Reserve Fund’s own loss must be added on top. Because the Reserve Fund was deployed alongside the rest of the USD pool, a fraction of that \( \$553\text{k} \) loss was generated by the Reserve Fund’s own exposure. With \( 1.15\text{m avUSD} \) of Reserve Fund capacity against a USD collateral pool of roughly \( \$122.5\text{m} \), the Reserve Fund represented around \( 0.94\% \) of the deployed base. That implies that approximately \( \$5.2\text{k} \) of the \( \$553\text{k} \) coverage payment came from the Reserve Fund’s own participation in the same loss. The relevant point is that the buffer slightly increased the loss base it was meant to protect, so the realized payment was about \( 100.94\% \) of the loss that would have existed if the Reserve Fund had remained outside the strategy.

The ETH pool follows the same logic. The \( 15.28\text{ avETH} \) coverage payment already includes the loss attributable to the Reserve Fund’s. With \( 55.36\text{ avETH} \) of Reserve Fund capacity against \( 7.2\text{k ETH} \) pool, the Reserve Fund represented around \( 0.77\% \) of the deployed capital. That means that roughly \( 0.12\text{ avETH} \) of the \( 15.28\text{ avETH} \) loss came from the Reserve Fund’s exposure.

In this instance, the trade-off was economically positive as the avUSD Reserve Fund earned \( 103\text{k avUSD} \) of extra capacity and the avETH Reserve Fund earned \( 1.10\text{ avETH} \), while the incremental losses caused by deploying the Reserve Funds were much smaller. But as a risk-management design, the practice still increases the system’s loss surface and reduces the fallback protection.

Part II: Tranching as a Service

In this second part we examine protocols that do not generate yield themselves but instead provide the infrastructure to tranche any external yield source. These platforms define the rules for splitting risk and reward between senior and junior, but the underlying strategy and its performance belong to whoever deployed it.

6. The Platform Model

Tranching as a service emerged as a response to the coupling between yield engine and tranche structure that defines product-native protocols. The idea is to separate the tranching logic from the yield source entirely, creating a layer that can take any yield-bearing position and split it into senior and junior exposure using configurable parameters. This means a single tranching platform can serve dozens of different yield sources without having to build or manage any of them.

6.1 What tranching as a service means

In a Tranching-as-a-Service (Taas) model, the platform provides the contracts, the yield split logic, the accounting, and the redemption rules. The underlying yield source is an external input, typically an ERC-4626 vault or a tokenised asset pool, that plugs into the tranching layer. The platform does not control the strategy, does not manage the capital, and does not determine the raw yield; it only determines how that yield gets divided and under what conditions each tranche can enter or exit.

7. Yield Distribution Mechanics in TaaS

The core design question for any TaaS platform is how to price the protection that junior provides to seniors. Strata and Royco address this through different models.

7.1 Strata: benchmark-floored yield

Strata splits any supported yield source into two ERC-4626 vaults, one senior and one junior, operating on the same base asset. The senior tranche receives a yield anchored to an external benchmark rate plus part of the underlying asset native yield. The benchmark rate is guaranteed. For the USDe market, this benchmark is the supply-weighted average of USDC and USDT lending rates on Aave v3 and for Neutrl's market, it is tied to the sUSDe APY.

Then, the risk premium, which represents the yield transferred from senior to junior as compensation for subordination, is calculated using an exponential function of the senior-to-junior TVL ratio and the underlying asset APY.

As more capital sits in senior relative to junior, the premium increases, redirecting more yield to junior. This creates a self-balancing incentive where junior becomes more attractive as senior grows, encouraging deposits that restore the coverage ratio.

In case the underlying yield falls short to cover the benchmark rate (which is guaranteed), junior subsidizes the senior from its own capital.

7.2 Royco Dawn: utilization-driven yield split

Royco takes a different approach. Instead of anchoring to an external benchmark, Royco derives pricing entirely from the internal supply-demand balance between tranches through its Yield Distribution Model (YDM).

The YDM measures how stretched junior capital is relative to the minimum coverage that the market requires at all times. That minimum coverage is calibrated at 100% utilisation, while lower utilisation leaves room for liquid deposits and withdrawals. This dynamic is governed by a yield curve defined at market creation, which behaves similarly to a Euler V1 utilisation rate model, with a target utilisation level that can gradually shift upward over days or weeks when utilisation remains persistently above target.

Royco also adds a product layer on top of the raw tranching infrastructure. The Dawn Senior Vault (DSV) is a separate ERC-4626 vault that allocates USDC across a curated and diversified basket of senior tranche positions from multiple Dawn markets.

7.3 Centrifuge: total personalization of tranches

Centrifuge operates at a lower level of abstraction. Rather than providing a specific yield split or rules, Centrifuge offers pool infrastructure where issuers configure their own capital structures, define how many share classes exist, assign custom valuation contracts to each asset, and control access through permissioning. This makes it less of a tranching protocol and more of a tokenization toolkit that can be used to build tranched products, particularly for real-world assets where standardized yield splits would not accommodate the diversity of underlying credit exposures. However, there are currently no tranches deployed by Centrifuge architecture.

8. Liquidity and Redemption Design in TaaS

A senior tranche without sufficient junior backing is a senior tranche without real protection Strata and Royco implement similar mechanisms based on the coverage ratio to prevent this.